Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFirst quarter update on our 2018 share portfolio

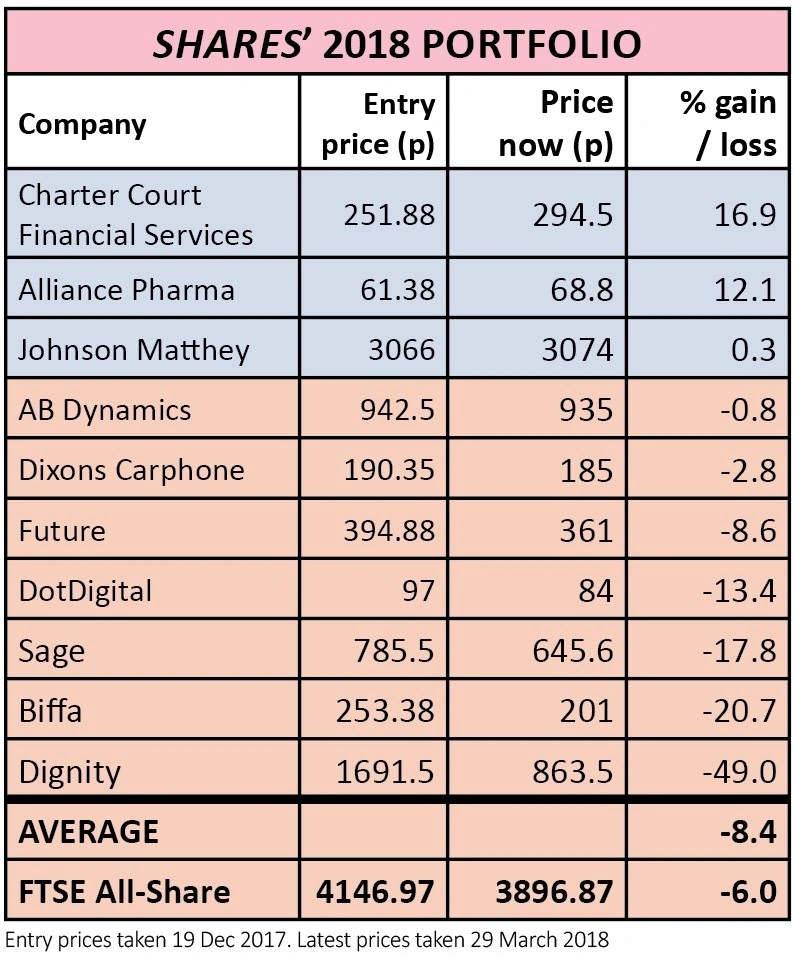

Our top picks for 2018 are lagging the broader market at the end of the first quarter. Our portfolio of 10 stocks has an average loss of 8.4% versus a 6% decline from the FTSE All-Share.

While this is a disappointing start, our selections were designed to be held for at least a year, so we remain hopeful that some of the laggards will pick up as the year progresses.

Before we look at the individual constituents, it is worth considering the state of the market as a whole.

Our selections were made on the eve of a stock market correction, so we’ve been battling negative investor sentiment almost from the start.

The market has also punished highly rated stocks with the slightest bit of bad news, which is relevant to several of our selections.

Investors in general currently seem to be nervous about buying stocks that have fallen in value, so we haven’t seen any widespread ‘bottom fishing’ since the market correction earlier this year.

STOCKS IN FOCUS

Half of our portfolio has outperformed the stock market, albeit only three of these stocks are in positive territory.

Charter Court Financial Services (CCFS) is up by 16.9% to 294.5p, helped by the strength of the buy-to-let mortgage lending market and more investors becoming aware of the stock.

Full year results published on 20 March showed a 128% increase in pre-tax profit to £111.7m; its loan book up 42% to £5.4bn; and 28.6% return on equity.

Investec analyst Ian Gordon believes niche banking companies like Charter Court offer ‘materially better value’ than the more ‘structurally challenged’ FTSE 100 banks.

ALLIANCE PHARMA LOOKING GOOD

Alliance Pharma (APH:AIM) is gaining traction as strong international sales growth drives its impressive performance. Underlying pre-tax profit increased by 8% to £24m in 2017.

Its shares are up by 12.1% to 61.38p since we said to buy last December and we expect them to end the year even higher.

The shares aren’t expensive at 14.9 times forecast earnings for 2018 given that analysts predict 12% compound annual growth in earnings per share for the next three years.

A FEW STOCKS SITTING QUIETLY

Johnson Matthey (JMAT) and AB Dynamics (ABDP:AIM) are sitting close to our entry level on each stock. The latter recently issued a decent trading update and said its new chief executive should start in the summer. It is bringing in someone new to drive corporate development.

Dixons Carphone (DC.) is down 2.8%, roughly half the decline in the broader market, which isn’t bad considering ongoing negative sentiment towards retail stocks. Its trading update in January was fairly decent and the share valuation is already discounting a tough market. A new chief executive and a new finance director bring some excitement to the investment case.

Media group Future (FUTR) is down 8.6% but we certainly don’t expect the stock to remain in the red. Research group Edison recently commented: ‘The share price has drifted back from recent highs and we consider that the current rating does not fully reflect the opportunity.’ The shares currently trade on 15.6 times forecast earnings for the year to September 2019.

THE DISAPPOINTING FOUR

The market reacted negatively to DotDigital’s (DOTD:AIM) half year results in February. A mere 1.5% pre-tax profit growth called into question the company’s share valuation. Prior to the figures the shares traded on 32 times forecast earnings for the current financial year. Such a rating would normally warrant faster earnings growth.

There were some delays to customers buying services from DotDigital ahead of new data regulations called GDPR which come into force in May. That’s something to watch closely in the near-term in case the regulations lead to a short-term drop in email marketing activity (and thus demand for DotDigital’s technology) as companies have to rebuild their marketing databases.

A weak first quarter update in January from Sage (SGE) served to pull down its share price. It suffered some revenue delay due to sales personnel receiving, in aggregate, around two weeks’ training time on the new ‘Sage Business Cloud’ product suite, as well as a poor show from its French operations. A stronger second quarter update could be the catalyst to revive the share price.

Biffa (BIFF) was trading on 11.9-times forecast earnings for the year to 31 March 2019 on the eve of its disappointing trading update last month. Ongoing restrictions for exporting paper recyclates to China prompted an 8% downgrade to the March 2019 financial year’s earnings per share (EPS) estimate.

The shares have fallen by more than twice the EPS downgrade, down 19% to 201p. They now trade on 10.4 times forecast earnings which seems unjustified given its core business is still trading well and earnings forecasts now assume zero financial contribution from exports to China for at least the next two years.

A planned bottle and can deposit return scheme in England could even create more recycling volumes, benefiting collection companies like Biffa.

And finally we have Dignity (DTY) which has halved in value since we said to buy. The business model has completely changed since our original article. A major overhaul of its pricing structure radically changes its potential earnings capability and thus the investment case.

We see better opportunities elsewhere in the market and believe now is the time to cut your losses on Dignity. The risk is another profit warning; the potential reward is a private equity takeover. We don’t think the risk/reward balance favours keeping the shares. (DC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.