Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine10 fantastic stocks for 2019

Every year the Shares team research the market to find investment ideas and create a portfolio of stocks to own for the year ahead.

We draw up a long list and then debate the pros and cons as a team over several meetings and then narrow the list down to the cream of the crop.

This year we’ve selected 10 stocks which look attractive for various reasons. We will regularly update readers on trading updates, financial results and other bits of relevant information as the year progresses.

Our goal is to hold these stocks for the following 12 months, although we will reassess their merits should something fundamentally change to alter the investment case. We hope you enjoy our analysis across this article.

COATS (COA)

In times of trouble a good strategy is to turn to companies which have a long history of generating solid returns. Coats very much fits the bill and its shares look great value trading on 12.2 times forecast earnings for 2019.

Coats is a global market leader in the manufacture of threads, boasting a 20% market share. It is expected to grow profit by 7% next year and there is also a 1.8% prospective dividend yield.

Its threads are used across a number of industries including clothing where it keeps jeans and trainers together for customers including Nike, Adidas and Next (NXT).

It plays very well into the popular and growing trends of athleisure and fast fashion, where retailers are turning round new products very quickly to satisfy ever-changing public needs. As well as threads and yarns it provides the apparel and footwear industries with zips, reflective tape and interlinings.

One in five garments sold globally is held together using its thread. It also makes threads for tea bags and bedding, among other areas.

Coats’ performance materials division is really exciting. This develops innovative threads and fire retardant yarns for customers including Proctor & Gamble, Michelin and Ikea. Its products end up in a variety of places from airbags and car tyres to fibre optic cables and protective clothing.

Berenberg analyst Anthony Plom says the growth opportunity for the performance materials division is significant, now representing 10% of group sales.

Coats has a history of generating more than 20% return on capital employed, a metric which shows how well a company is investing money in capital to generate profit. A figure above 15% is generally considered to represent a good business.

Investors should note ongoing weakness in its North American Crafts arm and some analysts hope this part of the group will be offloaded in the future, although Coats hasn’t formally put it up for sale. Other risks to consider include an economic downturn which may depress demand, plus rising labour costs which could put a squeeze on profit margins. A forecast 2018 year-end net debt position of £152m is small relative to its £1.1bn market cap.

James Goldstone, manager of Keystone Investment Trust (KIT), says Coats is ‘the most exciting story I’ve found in industrials’ and says the shares are terrific value.

The fund manager says customers love Coats’ premium product and premium service. ‘But most importantly, it is the audited supply chain (which really appeals) for global brands who are determined to have an ethical supply chain.’

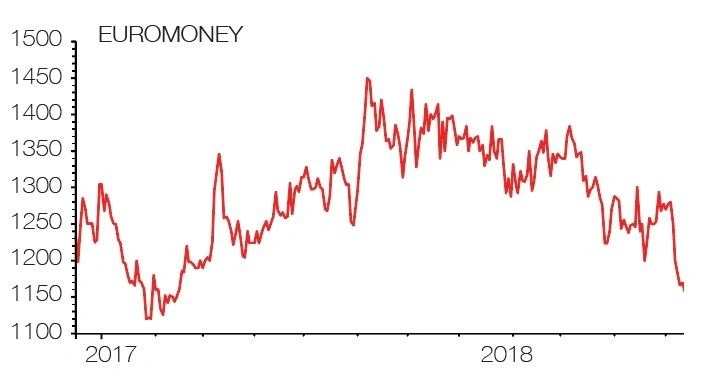

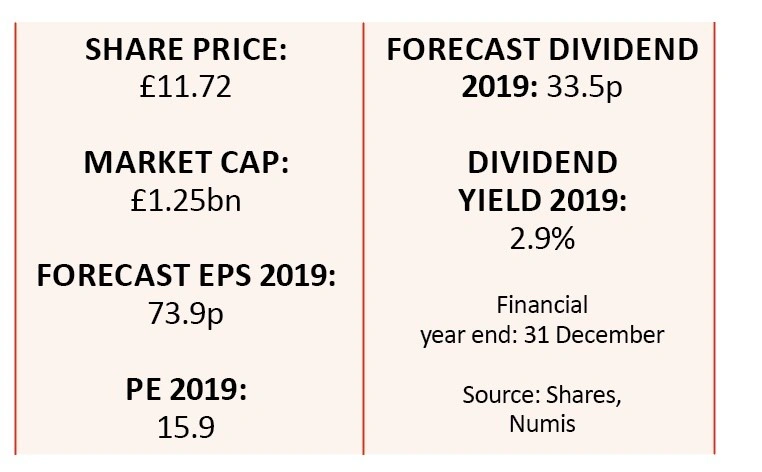

EUROMONEY (ERM)

We think the transformation of Euromoney (ERM) from an old-fashioned media business to a higher quality data services outfit will hit home with the market in 2019 and help drive the share price higher.

The company is rapidly growing its pricing and data side, diversifying away from a weaker asset management business made up of Institutional Investor magazine and offshoots as well as the BCA investment research arm.

The pricing, data and intelligence division does smarter things like providing prices for opaque markets using traditional journalism. This might mean finding out what parties are paying for different commodities, for example, and then monetising this highly valuable market intelligence.

With much of the income from this part of the business linked to subscriptions, Euromoney enjoys a good level of earnings visibility.

Even after the company splashed out $87.3m on the acquisition of two US businesses – BoardEx and TheDeal – the company should still be in a net cash position thanks to a series of previous disposals of non-core assets. This includes the Indaba mining industry event.

Prior to the two recent acquisitions, Numis forecast net cash of £135m by the end of 2019, a total which also reflects inherently strong cash generation from operations.

This situation provides headroom for further M&A activity to accelerate its shift to a higher quality business profile and a buffer in case times get significantly tougher.

The shares still trade at a material discount to global financial data peers despite the headway chief executive Andrew Rashbass has made since joining in 2015.

Euromoney trades on a forward PE of less than 16-times compared to a peer group average of 25.6-times, according to research house Edison.

Boardex and TheDeal are expected to be immediately earnings enhancing. Both are data-driven outfits with subscription-based models and therefore a good fit with the current strategy. BoardEx provides executive profiling and relationship mapping, while TheDeal is a database of M&A information.

There are some risks for investors to weigh. The asset management arm, which still accounted for nearly 40% of revenue in the past financial year, is struggling thanks to industry cost-cutting, which was exacerbated by the disruptive Mifid II regulations on financial sector transparency.

We accept Brexit could result in further pain. Additionally Daily Mail & General Trust (DMGT) continues to hold a 49% stake in the business and if it were to look to offload its holding this could depress the share price.

However, we still believe the shares are incredibly attractive given the tighter business focus and relatively cheap valuation.

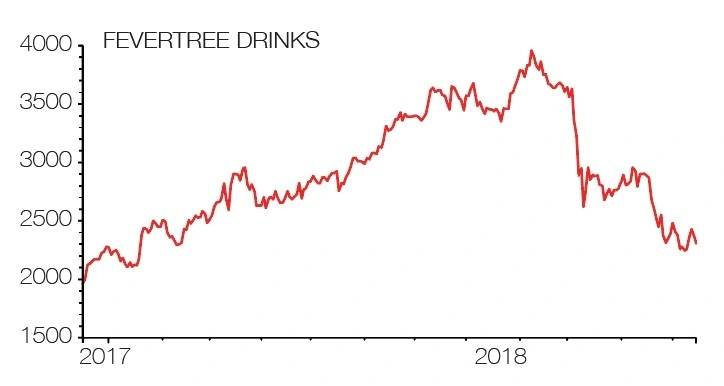

FEVERTREE DRINKS (FEVR)

From selling its first bottles of tonic water in Selfridges in 2005 to forecast sales this year of £225m, the Fevertree brand has been one of great marketing success stories of the last decade.

Having spotted the demand for quality mixers to go with premium spirits, the company behind the brand has toppled Schweppes to become the world’s leading producer of premium carbonated mixers by retail sales value.

Today it sells its products in 70 countries through both the ‘on trade’ to hotels, restaurants and bars, and through the ‘off trade’ to retail customers via supermarkets and other stores.

In terms of products, as well as half a dozen varieties of tonic water, lemonades and soda water for the white spirits mixer market, the firm has launched ginger ales, ginger beer and cola to tap into the dark spirits mixer category.

Greater availability of premium mixers is good news for spirits producers like Diageo (DGE) which are trying to drive their customers towards higher-margin premium products, creating a ‘virtuous circle’ between Fevertree and leading brands.

In terms of geographic spread, roughly half of the firm’s sales were in the UK last year and half were overseas with the major markets being the US, Spain and Belgium.

This summer the firm signed a new deal with Southern Glazers Wine & Spirits, the largest wine and spirits distributor in North America with $17bn in annual turnover, to distribute its products in the ‘on trade’ across 29 US states.

The US is the next area of excitement for its investment case. The Fevertree brand is best associated with tonic water and according to figures from the Distilled Spirits Council the US premium gin market alone was bigger than the entire UK gin market so the sales potential is large.

However gin only accounts for 4% of US spirits consumption while whisky accounts for 28% and vodka accounts for 32%, so the move into premium ginger ales and cola opens up an even larger market.

With markets around the world slumping this quarter and growth stocks out of favour, Fevertree shares have almost halved from their September peak.

There have been some market concerns that Fevertree’s growth has slowed in the UK, yet the absence of any comment from the company would suggest there isn’t anything serious going on – although we can’t say for certain.

Assuming the company meets analysts’ estimates the shares are trading on 45 times current year earnings which sounds high but if sales in the US do take off that ratio could fall sharply during 2019 should earnings forecasts be upgraded.

DISCLAIMER: The author owns shares in Fevertree

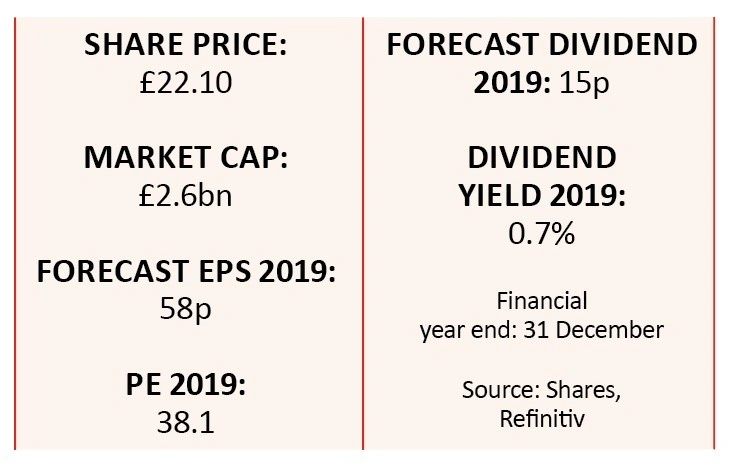

GB GROUP (GBG:AIM)

It’s hard to escape talk of Brexit uncertainty and potential growth slowing on a global scale as we enter 2019. So a company at the top of its structurally growing market, one that is potentially insulated from economic wobbles and capable of expanding for years to come, should be attractive.

GB Group (GBG:AIM) is a rare British-made world leader at the heart of the digital transformation.

We all know that people are embracing the internet at a rapid pace, from the online shopping explosion to booking travel, buying services and much else. Chester-based GB provides identity data intelligence and location insight, essentially giving primarily business-to-consumer customers and government organisations the information required to decide who to trade with, who to block, and fraud prevention all within a compliance-friendly platform.

Divided into two divisions – Location and Customer Intelligence and Fraud, Risk and Compliance – the company has what some analysts have called unparalleled and compliant access to data from more than 500 different sources. These include areas like credit reference agencies, electoral rolls, passport and national ID registers, postal services, retail consumer data and social media.

Staffed by more than 800 people in 18 countries, GB now counts in excess of 18,000 customers for industries as diverse as financial services, gaming, travel and retail.

It remains largely a UK company with two thirds of last year’s £119.7m revenue earned in its own backyard. That is changing, partly through organic means but also via carefully selected acquisitions, such as Vix Verify in Australia in October.

Last year just 2% of revenue was earned in Australia and 10% from the vast US market, and it is this global expansion that represents the other core growth driver of the business beyond the consumer switch to online everything. Recent momentum along these lines has been encouraging.

GB doesn’t have the market to itself. Key competition comes from large credit checking agencies, such as UK-based Experian (EXPN) or Equifax in the US. GB’s view is that its deeply layered and international datasets, plus adaptable technology platform, give it a key edge.

The stock is also not cheap, a point that will put off some investors. The price-to-earnings multiple for the year to 31 March 2020 currently stands at 28-times.

Yet this is based on forecasts that analysts admit may be on the conservative side, with Numis saying earlier this month that it expects an acceleration on the high single-digit revenue growth and 19% operating margins currently forecast. It anticipates a 600p share price over the next year.

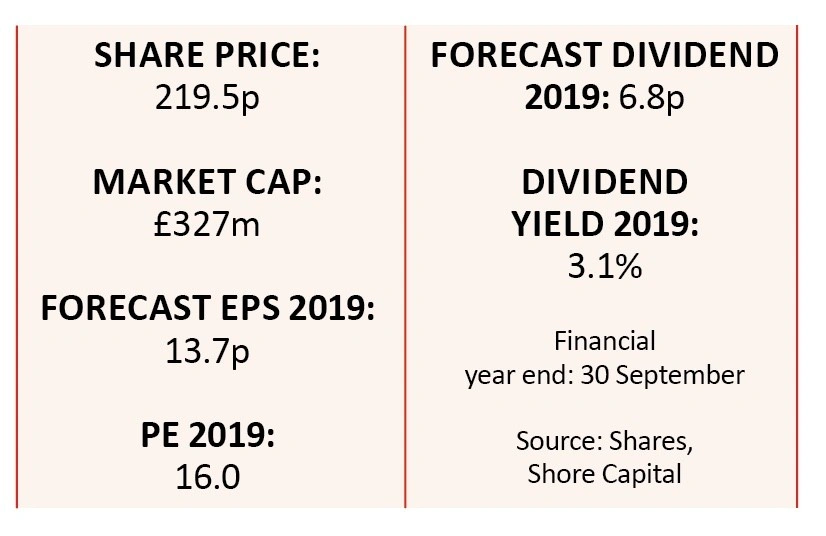

HOLLYWOOD BOWL (BOWL)

We believe the market may favour well-invested, highly cash-generative companies with minimal debt and undemanding equity valuations going into 2019. Hollywood Bowl has all these characteristics and offers slow but steady growth potential, plus scope for decent dividends over the long term.

Bowling is affordable and a nice treat. In tougher economic conditions we still want a break from the stress of work and life and bowling is often the destination of choice to relax and get away from it all.

The company wouldn’t be entirely immune from an economic downturn but we feel it would be more resilient than many other consumer-facing businesses.

Hollywood Bowl has 59 sites in the UK, nine of which were refurbished in its past financial year and a further seven to 10 centres will be revamped in the current financial year. Previous refurbishments have led to a boost in trading.

Retail landlords view the company as a magnet for consumers so they are happy to give sweeteners like free rent for up to 12 months or money towards the fit-out if Hollywood Bowl signs up to new or refurbished centres.

Hollywood Bowl has improved its food offering and spruced up its diners in order to improve customer dwell time.

Various efficiency initiatives are being rolled out to potentially enhance profit in the future. For example, it is introducing a new scoring system where it is much easier for the customer to input their information.

This data is also used for marketing purposes and Hollywood Bowl says more than 80% of people open its emails containing their scores from recent games. This very high engagement rate presents an opportunity to include promotions to get customers visiting its sites more regularly.

Seven sites have been fitted with pins-on-strings to replace the traditional pin setting system which has countless moving parts and has a habit of breaking down. Hollywood Bowl says the traditional system supports an average of 396 games before a fault stops play versus 1,443 games from the pins-on-strings system.

It plans to test a new indoor mini-golf concept which could help to accelerate group earnings significantly if successful.

Hollywood Bowl will pay a 4.23p normal dividend and a 4.33p special dividend in February 2019, both declared at the 2018 full year results on 10 December.

Broker Shore Capital forecasts 6.8p normal dividends for the current financial year, implying a 3.1% prospective yield. While this forecast doesn’t include a special dividend, it is worth noting that Hollywood Bowl has declared ‘specials’ for the past two years in a row.

KEYSTONE LAW (KEYS:AIM)

Top 100 law firm Keystone Law (KEYS:AIM) was set up in 2002 by a group of lawyers who were tired of the lack of modern thinking and creativity in traditional firms.

Building a platform model using technology and modern working practices, they hoped that other lawyers would see the attraction and join them.

Scroll forward to July 2018 and Keystone had almost 300 lawyers servicing thousands of clients across the UK.

By the time the company reports its full year results next May that number is likely to be significantly higher too.

A large part of the firm’s success is its investment in technology. Its ‘Keyed In’ platform provides insurance, compliance, marketing, sales, administration support, paralegals and continuous training.

For high-calibre lawyers and teams with a proven client following, the platform model allows them to plug in and operate as if they were part of a larger firm, outsourcing the support function and choosing where and when they work.

There are no fixed salaries, instead Keystone collects the billings from its lawyers’ clients and retains 25% for its services, passing through 75% of the billings. This is a higher percentage than many comparable businesses and offers the chance of significant upside for lawyers who are successful.

According to the firm’s own figures, of the applicants who are successful 90% generate a sustainable business with an average billing per new lawyer of £150,000.

The UK legal services market is the world’s second largest at over £30bn in fees per year. The mid-market, which Keystone is targeting, is worth close to £9bn in fees alone.

From 2016 to 2018, Keystone’s revenues have risen at a compound annual growth rate of 25%, above the average for law firms. Unlike many of its listed rivals, this growth has been achieved with no acquisitions.

Given first half sales of £20m and an increased number of lawyers and billings in the second half it looks a reasonable assumption that Keystone could beat analysts’ full year revenue forecasts of £40m.

As Keystone’s costs are minimal, almost all of the increase in revenues drops through to profit which means that analysts may have to raise their forecasts when it reports.

The firm joined AIM in November 2017 following a heavily over-subscribed placing at 160p and the shares have been popular with investors ever since, reaching an intraday high of 460p as recently as this September.

Since then the shares have retraced to 370p as markets have rotated towards value stocks, which gives long-term investors a window to buy into a continuing growth story today.

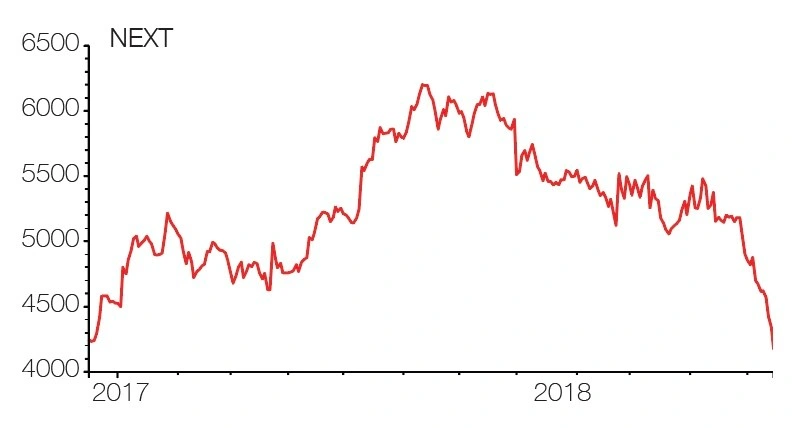

NEXT (NXT)

We recognise retail is completely out of favour with investors and so are UK-domestic stocks. However, it feels the right time to take a contrarian view and look for opportunities in both these categories.

We’ve picked Next in the belief that management can navigate the tricky backdrop and that we may also see a bounce in UK-focused businesses, assuming there is an agreed Brexit plan which brings more certainty to the market.

Led by respected shopkeeper Simon Wolfson, Next’s thriving online operation is widely overlooked. Besides a pristine balance sheet, Next is highly cash generative and should be able to withstand flagging footfall while maintaining profitability.

Next is so much more than a bricks and mortar fashion retailer. Online market share gains, boosted by a growing online overseas operation and the third-party brands business, LABEL, should continue to outweigh the drag from lower shop sales.

Despite falling like-for-like sales, the vast majority of Next’s stores remain very profitable. It also has many stores on short leases. When they come up for renewal, it can shut the worst ones and those being renewed are being done on much lower rents.

It is making more use of in-store stock to fulfil online orders rather than solely depending on warehouse inventory. And there will be a trial using stores as a collection point for third party, non-competing businesses.

While third quarter store sales fell 8%, online sales grew by 12.7% and Next maintained sales and profit guidance for the financial year to 31 January 2019.

With spending migrating to the web, Next is heading in the right direction with more than half of sales now coming from its online and finance businesses.

Invesco fund manager Mark Barnett also argues that having a large physical store estate is no bad thing. He says: ‘Next is combining the best of offline with online. A large number of orders are click and collect ones via stores, so Next needs a high street presence. These stores may not look the same in the future as they do today.’

Broker Liberum forecasts adjusted pre-tax profit will hit £727.3m for the year to January 2019 and then rise to £743.3m in 2020 and £773.4m in 2021.

The shares trade on a mere 9.2 times forecast earnings for the financial year to 31 January 2020. Next is one of the best-run companies on the stock market and that equity rating is an absolute bargain for a business of its calibre. You’re also being paid an attractive stream of dividends, currently yielding a prospective 4.1%.

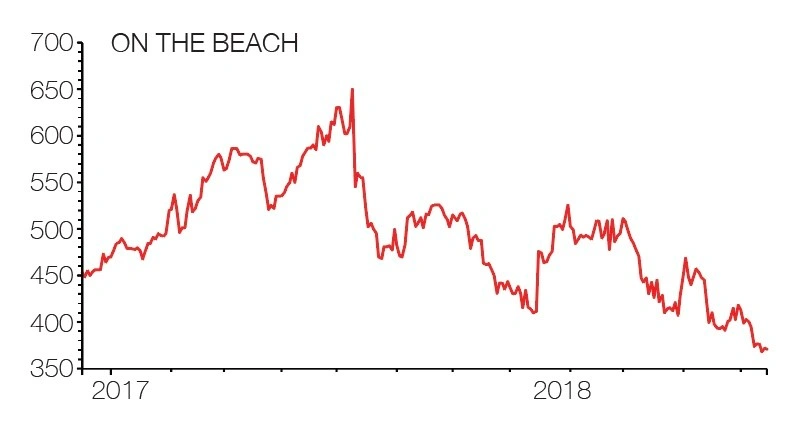

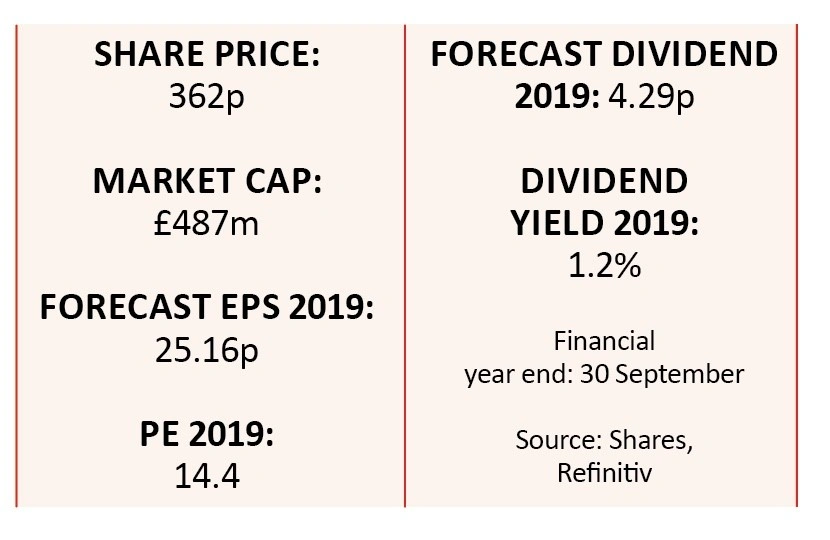

ON THE BEACH (OTB)

We believe On The Beach (OTB) is a great business with a superb track record of using technology and marketing to attract customers and get them to spend money.

It is an online retailer of mainly short-haul beach holidays, allowing people to build their own vacation by picking their flights, hotels and services.

Customers are regularly drawn to On The Beach for its wider selection of flights and hotels at attractive prices compared to tour operators, which often offer less flexible packages at a higher price tag.

It has a bespoke in-house recommendation system which works by taking cues from how someone browses its website and dynamically adapts the content presented. It personalises holiday suggestions based on various facets of hotel and flight browsing detail.

On The Beach continuously tests changes to its website to see the most effective ways of converting visitors to sales. This testing also helps ensure the browsing and transaction process is as smooth as possible for the customer.

Furthermore, it has invested in booking management capabilities and reminder functionality so that customers can interact with the company via an app before, during and after their holidays. The company also offers a 24 hour telephone service if problems arise during someone’s holiday.

All of these initiatives help to improve customer satisfaction and drive repeat bookings. The company said in November that its repeat purchase rates had increased significantly in 2018.

The group is expanding outside of the UK and now has a presence in Sweden, Norway and Denmark. International operations are currently loss-making as the company enters new territories.

On The Beach benefits from both organic and acquisitive growth, with the latter including ownership of Sunshine.co.uk, an online low-cost travel agent; and Classic Collection which is a business-to-business provider of packaged luxury beach holidays to offline travel agents in the UK.

It plans to launch an online B2B platform for Classic Collection’s travel agent users, leveraging On The Beach’s existing technology and breadth of supply.

Group pre-tax profit is expected to rise from £26.7m in 2018 to £40.5m in 2019, according to consensus estimates. The shares look great value at 14.4 times forecast earnings when you consider that rate of predicted growth.

Numis analyst Richard Stuber forecasts 16% compound annual growth in earnings per share between 2018 and 2021.

On The Beach has a £47.3m net cash position, effectively giving it the financial firepower to consider further acquisitions and/or money to support the business if times get tougher.

The group is looking to boost its long-haul beach holiday sales and bolt-on acquisitions could potentially help to accelerate this strategy.

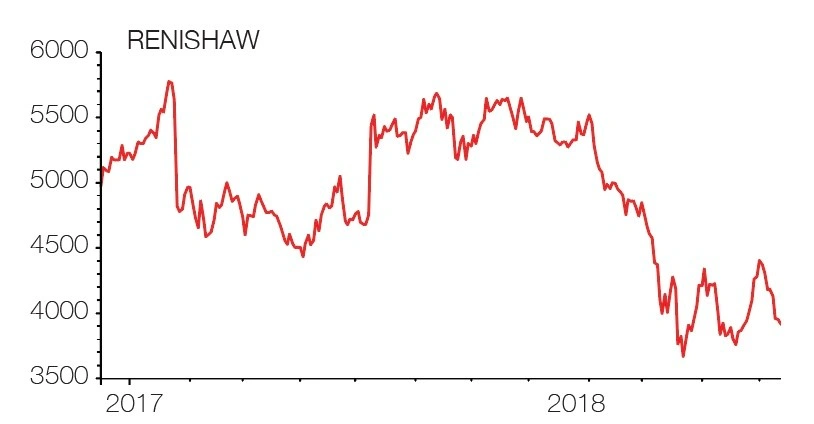

RENISHAW (RSW)

Science-based engineering firm Renishaw (RSW) has a clear and focused approach which it consistently pursues regardless of the macro-economic backdrop.

A big decline in the share price in recent months should spark your interest as it means you can gain exposure to this high-quality outfit at a significantly more attractive price.

The company has been unfairly punished by the market for investing in its business. Its strong commitment to research and development spend and vertically integrated model (it makes its own stuff) means that margins and profit can fluctuate on a quarter-on-quarter view.

This was the story in the first quarter of its current financial year where revenue grew by 8% but costs increased by 14%. As a result, analysts downgraded earnings forecasts for the current year, but these now look very much factored in.

We are happy to pay a premium rating for this outstanding business. The company is a world leader in the development and manufacture of very high-end precision measurement kit. Products are used across a range of sectors from aerospace to automotive, healthcare and a range of other markets.

Products include 3D printed customised medical implants, and hardware and software to improve the calibration and performance of machine tools.

The firm’s sheer level of expertise creates significant barriers to entry and means it faces few true competitors.

This position is underpinned by consistently spending 15% to 16% of sales on research and development, the sort of level traditionally associated with a tech firm or pharmaceutical company, says Milena Mileva, fund manager of Baillie Gifford UK Growth (BGUK). She says Renishaw is an ‘exceptional growth company’ which she wants to hold for the next decade or beyond.

It is also distinct from a lot of other engineers in that it does the bulk of its manufacturing in-house. It has plants in the UK, Ireland, India, Germany, the US and France. This supports quality control and its heavy use of automation drives efficiency.

The stock could suffer some volatility if the global economy struggles, plus some analysts have raised particular concern over exposure to the Chinese automotive industry. The business also has relatively limited visibility (around six weeks) on its order book.

However, we remain confident these concerns will be outweighed by the inherent strengths of the business over 2019 as a whole. This is a best-in-class company to own for the long term.

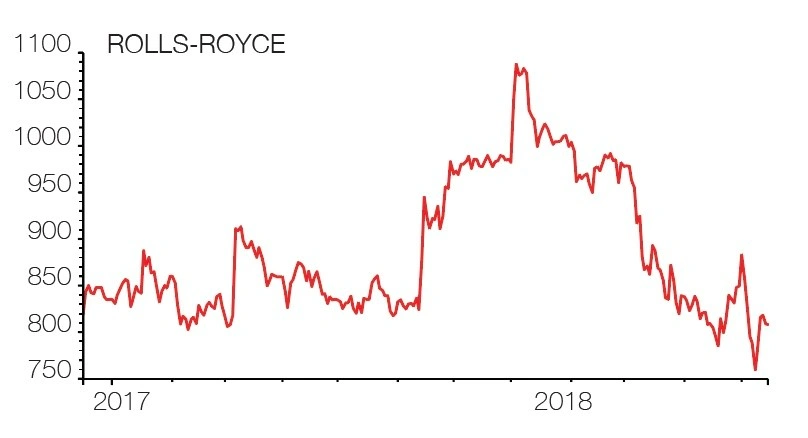

ROLLS-ROYCE (RR.)

It may have been a testing year for Rolls-Royce (RR.) thanks to a series of engine inspection issues yet this remains a global champion now trading at a rare discount. It comes as no surprise to Shares that long-term growth funds run by the likes of Baillie Gifford and activist investor ValueAct Capital are shareholders.

Forget luxury cars, and soon ships (the Marine division is being sold), the future is all about planes, trains and power systems.

Aero engines, both commercial and defence, make up three quarters of revenue and Rolls has grown to become the senior player in an effective global duopoly (ahead of rival General Electric) in civil aviation. This area is worth more than half of its total sales.

While this is a highly technical and cutting edge science-based business, the model is easy to understand. It builds engines, often selling them at cost, and then enjoys substantial profit over the typical 25-year engine lifecycle from servicing.

Get more engines on more planes that fly more air miles and you’ve got a virtuous cycle of bumper cash flow long into the future. That cash should then underpin a growing stream of dividends.

Rolls has enjoyed prolonged spells of growth over the years, and we believe it is on the cusp of a new growth leg that will push the share price higher. For example, in the 10 years between 2003 and 2013 Rolls-Royce’s stock increased more than 10-fold to nearly £13.00.

Since then life hasn’t been as easy. There has been a corruption scandal and multiple profit warnings which nearly saw the company fold, according to its current chief executive Warren East. But the former boss of UK chip design champion ARM is making real headway in putting the pieces back together again.

Efficiency improvement and sharper execution lie at the heart of East’s plan, as well as vastly improved free cash flow. This restructuring will see 4,600 jobs go at its state-of-the-art facility in Derbyshire but they will largely come from bloated admin and middle management layers, so core engineering capacity should not be damaged.

Expectations for 2018 were pared back to reflect the major operational upheaval; the longer-term prospects are getting much brighter. Investors should expect £1bn of free cash flow by 2020 and similar pre-tax profit. Dividends are also set to start climbing again, with 11.7p per share in 2017 expected to increase to 17.4p by 2020.

So while the near term-term price-to-earnings valuation metric looks expensive (29.5-times for 2019), investors are really buying the potential rapid recovery. The 2020 PE falls to 18.7-times. We expect the share price to break back above £10.00 in 2019.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Aequitas

Big News

Editor's View

Feature

Great Ideas

- Share pick for 2019: Hollywood Bowl

- Share pick for 2019: Rolls-Royce

- Share pick for 2019: GB Group

- Share pick for 2019: Euromoney

- Share pick for 2019: Next

- Share pick for 2019: Renishaw

- Share pick for 2019: Fevertree Drinks

- Share pick for 2019: Keystone Law

- Share pick for 2019: On The Beach

- Share pick for 2019: Coats