Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineChemicals sector remains attractive despite sell-off over past six months

The chemicals sector has historically been a very good place to invest with significant share price gains over the past decade and occasionally generous dividends.

Unfortunately momentum has stalled in parts of the sector over the past six months amid concerns about a global economic slowdown and how that could feed into weaker demand for chemical products. There have also been some concerns about growing competition, falling margins and high inventory levels.

This has resulted in widespread share price weakness which has pulled down, on a broad basis, what are often high valuations for the sector.

Investors with a long-term view may therefore wish to take advantage of this situation.

TWO STOCKS TO BUY

Our top pick among the sold-off shares is Synthomer (SYNT) which has a cheap valuation and boasts higher returns on money invested in its business than the peer group average.

We also like Croda (CRDA) as a best-in-class chemicals business although investors will need to pay a premium to own the stock.

BROAD RANGE OF APPLICATIONS

The London-listed chemicals sector has a wide range of companies providing products used to make a very large range of goods.

For example, Johnson Matthey (JMAT) manufactures emission control catalysts to control the amount of harmful pollutants from cars, while Zotefoams (ZTF) creates high-performance foam materials for the likes of Nike.

Synthomer’s products are used in many different places such as footwear insoles, condoms, packaging tapes, carpets and waterproofing products. Treatt (TET) helps food and drink taste better and Victrex (VCT) makes a high-resistance plastic.

All of these companies have stand-out products and are vital to the needs of businesses and consumers around the world.

Sadly various headwinds have led some investors to turn their back on the sector. In particular, investors are concerned about a slowdown in industrial production in China and what will happen in the event of a no-deal Brexit, says Berenberg analyst Sebastian Bray.

‘China currently accounts for over 40% of global chemicals demand and this is predicted to rise to 50% by 2030,’ comments the analyst.

This means Chinese industrial production is vital for setting the chemical industry’s growth expectations. When Chinese factories struggle, they will buy fewer chemicals and this has depressed the market’s growth expectations for the sector according to Bray.

VICTREX BATTLES COMPETITION ISSUES

On a stock-specific basis, Victrex has already seen falling medical sales hit gross margins. These could fall further as much of its growth comes from industrial sectors where it will need to expand capacity in order to stay competitive. There are also market concerns that competition is growing for Victrex’s flagship product called Peek, a super-strong, heat resistant and lightweight plastic used as an alternative or replacement for metal in areas like transport, the

industrial sector, electronics and medical devices.

Shares in Victrex have enjoyed a very good run over the past decade up until late 2018. The same applies to Synthomer whose shares have recently been hurt by weaker demand and lower prices. It has also faced the threat of competitors expanding capacity for nitrile latex – Synthomer is the world’s largest producer and nitrile accounts for more than half of its organic growth.

At 384.4p, Synthomer’s shares now trade at close to a 25% discount to the five-year average of 14.3 – the current price-to-earnings ratio is 10.9-times based on 2019’s forecasts. ‘The shares are set to grow operating earnings in line with the wider European chemicals sector, and at higher returns (16% versus 14% return on capital employed),’ notes Bray at Berenberg.

The analyst believes recent negative issues are only temporary. He says nitrile latex market tightness bodes well for 2019 and that that Europe and North America should return to volume growth this year. On that basis, negative factors look fully priced into the shares, although investors should treat this as a higher-risk stock for now.

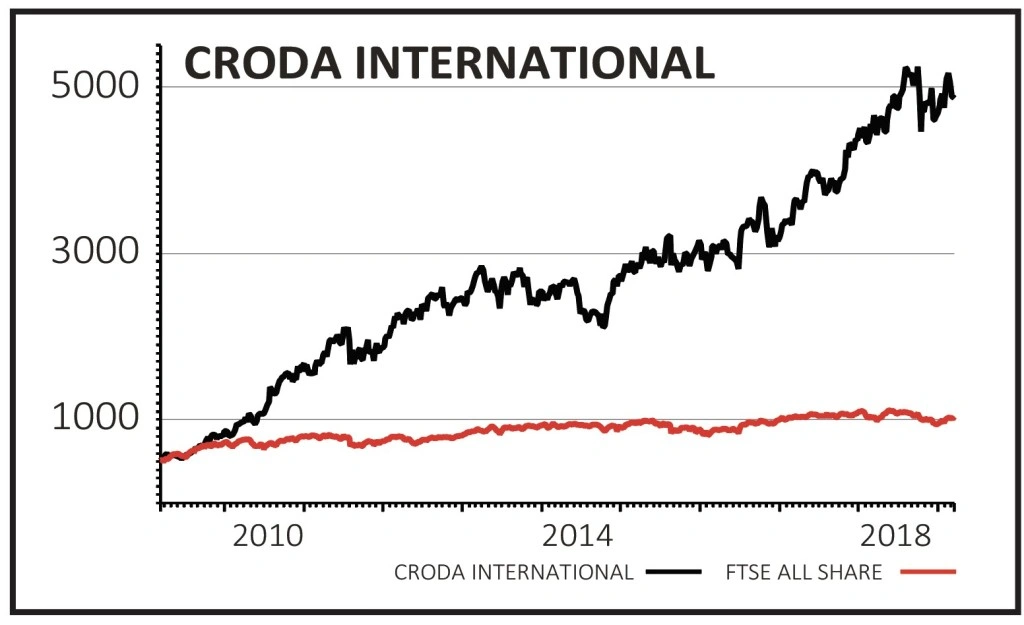

CRODA’S BRIGHT OUTLOOK

Croda is highly regarded in the world of business and has rewarded shareholders with 999% total return (share price gains and dividends) over the past decade.

It creates and sells speciality chemicals for a range of beauty products, including moisturisers and colour cosmetic products, among other areas.

The shares have been volatile of late, partially down to earnings downgrades from analysts linked to US production delays. That should only be a temporary set-back.

Investment bank UBS believes the personal care side of Croda could do well in 2019. ‘Recent comments by L’Oreal, especially on the China skin care market, and innovation initiatives underway at Henkel bode well for new project growth,’ it says. ‘Croda’s doubling of research and development labs in the last four years is hardly likely to be speculative investment, more a direct response to customer demands, in our view.’

Croda hopes to drive future growth by investing in speeding up product innovation and focusing on new technologies, which will hopefully accelerate sales over time.

At £48.67, Croda trades on 24.4 times forecast earnings for 2019. UBS believes capital expenditure peaked in 2018 and so this highly cash-generative company should have more money to pay down debt, pay dividends in the future or even make acquisitions. It estimates Croda will have virtually no debt by the end of 2021.

Investors buying shares in Croda are getting a company with a solid track record of achieving great returns from money invested in its business, slow but steady sales growth and a rising stream of dividends.

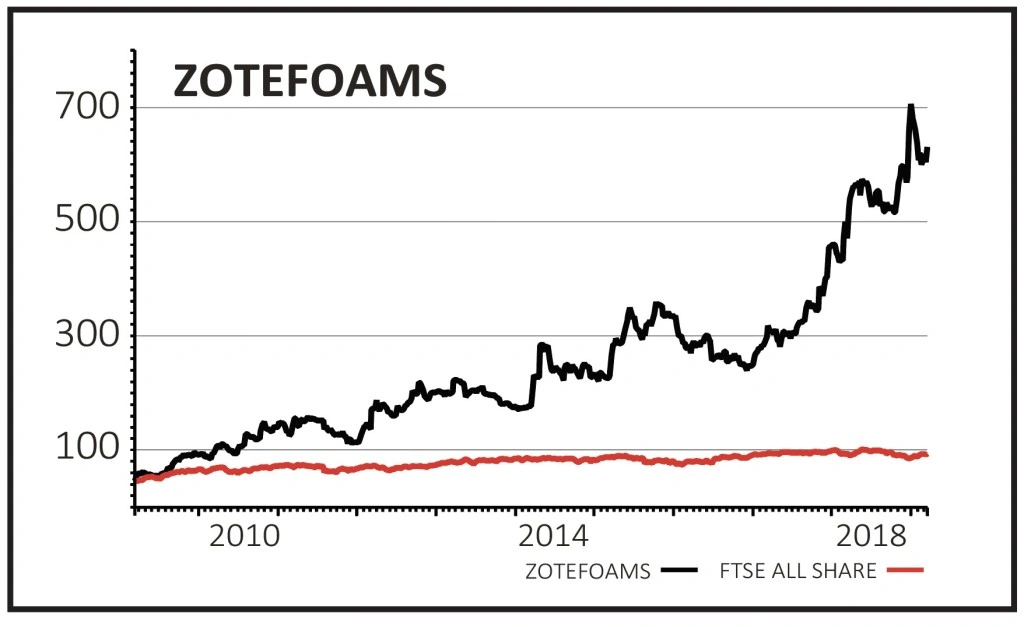

Zotefoams is another standout performer in the UK-listed chemicals space in share price terms. Its lightweight foam sheet material is used in packaging, transport goods and shoe padding among other things. The company is investing in capacity to try and keep up with demand.

WHAT HAS GONE WRONG AT ELEMENTIS?

Elementis’ shares have struggled since 2016. It provides additives for hair, skin care and cosmetic products. The company also supplies high value additives to help improve and preserve products and serves a range of end markets, including life sciences and aerospace.

Coatings, Elementis’ biggest division representing approximately 40% of sales, has been struggling with lower demand for coatings and paint – a trend also flagged by chemicals giant AkzoNobel.

Its acquisition last year of industrial talc additives producer Mondo Minerals also divided investor opinion. Shareholders initially expressed concern over the $600m acquisition price and told it to renegotiate. The deal was then secured for $500m but at a cost of rising debt and a dilutive rights issue.

Elementis plans to grow its position in personal care, coatings and Asia, get rid of unloved assets, improve manufacturing productivity and expand its product pipeline.

OTHER CHEMICAL STOCKS

Johnson Matthey’s shares have been very volatile since 2014. Investors have increasingly questioned whether its catalytic converter business has a future given the shift from combustion

engines to electric vehicles which don’t need the anti-pollution devices.

The FTSE 100 member is developing an enhanced lithium nickel oxide cathode material for use in the electric vehicle market but the proposition is still in the development stage.

Also exposed to the automotive market is Victrex, which creates high performance polymer solutions for a range of products, including smartphones, aeroplanes, cars and medical devices.

Victrex has been hit by market softness in its automotive division and underwhelming consumer electronics sales, but there has been an improvement in the former in January and February.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.