Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInvestment trusts offer a way of accessing firms that stay private for longer

Many of the world’s most exciting businesses are not yet listed on a stock exchange, but that doesn’t mean investors can’t get exposure to this part of the universe. A number of investment trusts have holdings in unlisted (also known as unquoted) companies, giving you plenty of options as we discuss in this article.

While venture capital trusts and specialist private equity vehicles tend to focus purely on this space, these options can feel too racy for some investors.

An alternative is to look at the growing number of more general equity investment trusts which have a smaller proportion of their assets in private companies. This may be a good starting point for newcomers to the space and those wanting to take a more blended approach.

Driving this part of the investment market is the fact that companies are staying private for longer.

Historically, the average age of a business when it floats is five years old, today it is closer to 10. Companies no longer need to turn to the stock market to get capital to invest in their businesses and this is why we have seen a growing number of so-called Unicorn firms, which are already worth $1bn before they float on a stock market.

Spectacular rewards from one investment trust

Scottish Mortgage +594% – MSCI World +154%

Scottish Mortgage has achieved nearly four times the gains of MSCI World, an index of more than 1,600 mid and large-cap companies in 23 countries, over the past decade.

ARE UNLISTED COMPANIES HIGHER RISK?

Investing in unlisted companies does not necessarily mean investing in risky, early-stage enterprises. There are many established, profitable businesses that have simply chosen not to go public. That is not always the case and any investor considering the unlisted space should be aware of the risks and have a long time horizon over which to invest.

Thomas McMahon, senior analyst at research group Kepler, says: ‘Due to the risks, choosing a manager with the pedigree and resources to invest in this part of the market is critical.’

Investment trust Scottish Mortgage (SMT) currently has 16% of its assets in unlisted companies. Fund manager James Anderson has good form in picking out future winners; companies the trust has held from unquoted through to listing include Alibaba and Spotify.

Charles Cade, research director at stockbroker Numis says: ‘These private investments are not immature venture capital companies, but are typically established, often highly cash generative businesses, some with valuations over £1bn. James Anderson now sees the majority of emerging growth opportunities being in private rather than public companies.’

Baillie Gifford, the asset manager running Scottish Mortgage, last year launched Baillie Gifford US Growth Trust (USA), with a view to tap into the bounty of exciting, unlisted firms across the pond.

The trust is able to hold up to 50% of assets in unlisted businesses although co-manager Helen Xiong says this is ‘a limit not a target’. After meeting 200 companies over the past 12 months, the team have invested in just nine unquoted businesses, representing around 9% of assets.

These include Zipline, a business which delivers medical supplies uses drones. The delivery of blood has been particularly ground-breaking in areas such as Rwanda, where the infrastructure for road delivery is poor and the substance has a short shelf life.

Xiong is also excited about an investment in Peloton, a fitness business which offers time-poor people access to top-of-the-line exercise classes from the comfort of their own home using its own exercise bikes. The firm films around 14 hours of live footage a day and streams it to people so they can have the fun of a group class at a time and place of their convenience.

Xiong says: ‘We think the trend of companies staying private for longer is structural rather than cyclical. The number of listed companies in the US has halved over the past 20 years. Investing in private companies is about cultivating relationships over the long-term; we think about what the purpose of the business is and what problem it is trying to solve.’

A NEW NAME ON THE SCENE

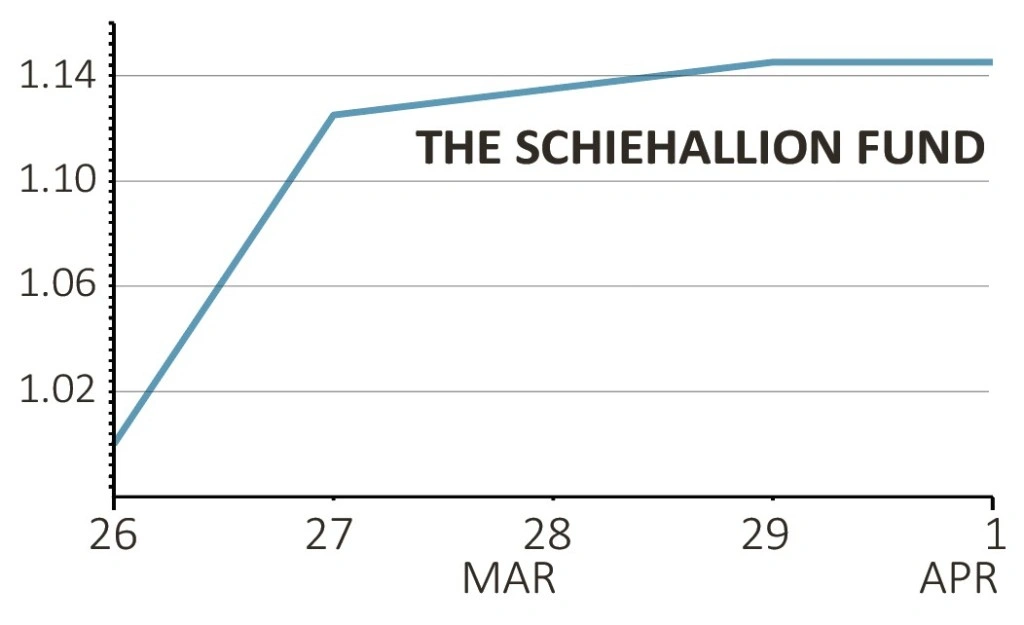

Baillie Gifford last month launched investment trust The Schiehallion Fund (MNTN), raising $477m to invest in later stage private businesses that have the potential to list on a stock market with a value of at least $500m.

Managed by Peter Singlehurst, head of the unlisted equities team at Baillie Gifford, the trust will aim to be at least two-thirds invested within two years, with a portfolio of between 20 and 60 companies.

It already trades at a 15% premium to its listing price, however it is important to note that the fund is not available to retail investors (see box-out below).

RETAIL INVESTORS CANNOT BUY THE NEW BAILLIE GIFFORD FUND

Shares in London-listed The Schiehallion Fund have done very well since floating last month. However, the investment trust isn’t available for retail investors to buy as Baillie Gifford has classified the product as not being suitable to this audience because of the risks around capital losses, liquidity and the long-term nature of investing solely in the unquoted market. The investment trust launch has been deliberately low-profile for this reason.

A handful of institutional investors including pension funds have provided Schiehallion’s seed money. The fund is targeting a net total return (on a net asset value basis) of three times invested capital over a rolling 10 year period, which Numis estimates is equivalent to c.11.6% per year compound growth. The fund doesn’t expect to pay dividends.

MIXING QUOTED AND UNQUOTED

Despite the specific restrictions around Schiehallion, the growing group of trusts focusing on unlisted companies (alongside quoted stocks) highlights how the area is becoming more appealing and mainstream among investors.

Woodford Patient Capital (WPCT) is perhaps the best-known equity trust focusing on this area; currently it has around 77% of assets in unlisted films.

Other trusts with significant exposure include Tetragon Financial Group (TFGS), Caledonia Investments (CLDN) and Majedie Investments (MAJE) which have 36%, 35% and 33% of assets in unquoted companies respectively.

Unlisted companies often attract investors’ attention because of the small number of high-profile success stories, which have gone on to become huge global enterprises. But there are far more failures than Unicorns in this area of investing and investors should be cautious.

McMahon says: ‘There is greater uncertainty around the valuation of unlisted companies as they don’t have the daily price discovery that comes from being traded on a public exchange.’ Because unlisted entities are priced less often, they can move significantly at these valuation points.

One thing that experts do agree on, however, is that if you are looking to invest in unlisted businesses then doing so through an investment trust is better than doing so through an open-ended fund such as a unit trust or Oeic.

With open-ended funds, a fund manager could be forced to sell their holdings if there is a change in sentiment and redemptions from the fund, whereas this is not the case with trusts, which have a fixed level of assets.

Simon Elliott, head of investment trust research at Winterflood Securities, says: ‘Although guidelines exist for valuing unquoted companies, it would appear to be an art rather than a science and failure to meet milestones or achieve fundraising targets can result in write-downs on a company’s value.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.