Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineNine ways to fill your ISA

You may find it odd to celebrate the start of the new tax year as 6 April often brings rising taxes and falling benefits. However, the one thing in investors’ favour is that the ISA allowance clock is reset. It means you can invest up to £20,000 over the coming tax year and not pay any tax or capital gains on investments inside the wrapper.

The start of the new tax is often one of the busiest times of the year as many investors are eager to take advantage of the new ISA allowance. For this reason, we’ve analysed the investment trust market and picked nine products which are worth buying at the current price.

The selection is quite diverse in terms of style, assets and geographic focus. You may be familiar with some of the investment trusts and others may be less well known. We include the reasons to buy them and some guidance on the type of person they may or may not suit. Any reference to the term ‘OCF’ stands for ongoing charges figure.

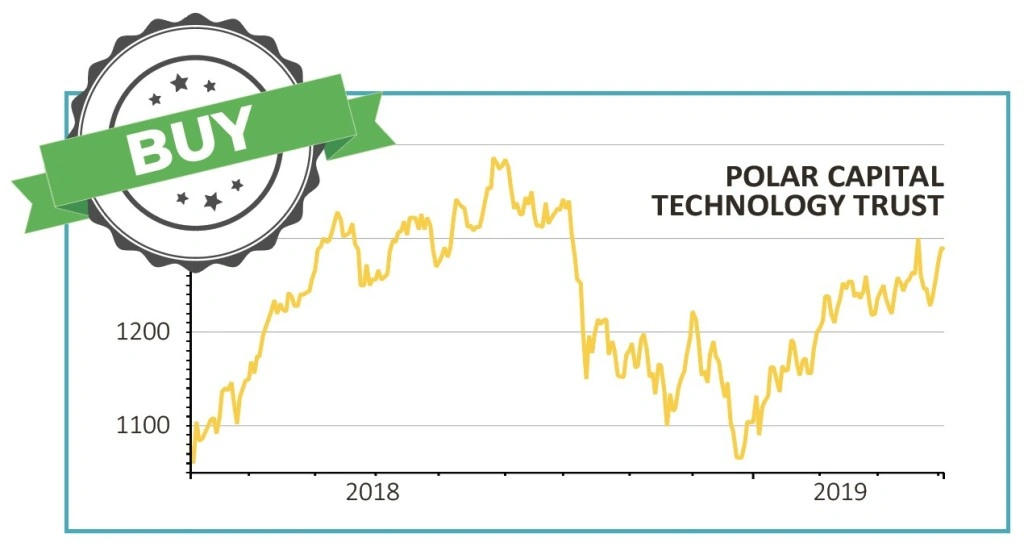

Polar Capital Technology Trust (PCT) £12.88

Discount to NAV: 6.8% – OCF: 0.99%

A technology fund might sound high risk to many investors yet fund manager Ben Rogoff might argue that the biggest risk is ignoring the space when technology is disrupting existing business models and carving entirely new industries.

Imagine how different the world might look without Apple’s iPhones, Googling the internet or Microsoft’s desktop applications – these services helped so many people to become computer literate in the first place.

Names in Polar Capital’s portfolio include chip maker Advanced Micro Devices and software stocks like Alteryx, Twilio, New Relic and Hubspot.

Over the past decade the trust has delivered net asset value (NAV) total return of 551% (to the end of 2018), smashing the 423% return of the Dow Jones World Technology benchmark.

Recent months have seen an extreme spell of volatility across technology markets and that may scare off some investors for this type of trust. Yet this is currently reflected in a NAV discount far in excess of its 3.7% average over the past 12 months, according to data from Winterflood.

Rogoff remains highly optimistic about the long-run prospects for select technology themes. Areas like cloud computing, software-as-a-service, digital marketing, complex microchips and robotics/automation are some of his particular favourites.

Witan Investment Trust (WTAN) £10.38

Discount to NAV: 2.9% – OCF: 0.79%

The near-3% discount to net asset value represents a good opportunity to secure access to an investment trust with a strong track record.

Witan uses 10 different third party fund managers who are experts in different fields. Together they invest in global equities and account for the bulk of Witan’s portfolio.

The aim is to also generate less volatile returns than a portfolio steered by a single manager.

The managers appointed by Witan have varying geographic focuses and investment approaches which can perform well in different circumstances.

Among them is Nick Train from asset manager Lindsell Train who likes quality companies, as well as Derek Stuart from Artemis who specialises in spotting out-of-favour stocks with unrecognised growth potential.

Around 10% of the portfolio is managed in-house by Witan’s executive team, with a focus on specialist funds in areas like healthcare and private equity. This team includes Andrew Bell, who has been responsible for the overall running of the fund since 2010.

Witan has only underperformed its benchmark in two out of the last nine years. The trust is well placed to extend a record of 44 consecutive years of dividend growth with revenue reserves equivalent to one-and-a-half times the cost of its latest annual dividend.

Broker Numis Securities sums up the appeal of the trust: ‘We regard Witan as an attractive core holding for investors seeking global equity exposure. The fund provides access to a number of leading managers, and has a competitive ongoing charges figure given its multi-manager approach.’

Watch our video interview with Witan’s CEO Andrew Bell

Baillie Gifford Shin Nippon (BGS) 180.6p

Premium to NAV: 4.9% – OCF: 0.89%

Managed by Praveen Kumar, Baillie Gifford Shin Nippon offers a way for growth-hungry investors to gain exposure to Japan’s legion of under-researched, innovative smaller companies.

Kumar’s mission is to generate long-term capital growth through investment in small Japanese companies which boast above-average capital growth prospects.

He targets high growth, entrepreneurial companies with the potential to disrupt traditional Japanese business models or exploit niche market or overseas opportunities.

With Kumar seeing more and more opportunities on the ground, the board is also seeking shareholder approval to permit investment in unlisted companies at a level of up to 10% of the portfolio at the time of purchase.

While Baillie Gifford Shin Nippon has delivered impressive net asset value total returns over the past decade, significantly outperforming the MSCI Japan Smaller Companies index, NAV actually fell 6.1% in the year to 31 January 2019.

Weak Chinese demand over the year had a negative impact on some Japanese small caps, with risk-averse investors viewing them as more vulnerable to external shocks.

Yet Kumar remains positive on the Japanese outlook, isn’t concerned about Brexit (around half the investments are domestically focused within Japan and the remaining holdings have minimal exposure to the UK) and the portfolio is packed full of growth potential.

Top holdings include specialist medical equipment company Asahi Intecc, online legal advice website operator Bengo4.com and online food delivery service Yume No Machi.

The shares have typically traded at a near-5% premium to NAV over the past few years.

Invesco Income Growth Trust (IVI) 267p

Discount to NAV: 14.8% – OCF: 0.75%

Savvy investors often look for something out of favour in the hope they can pick up a bargain or an investment that could bounce back. It may seem odd looking for unpopular assets but these are often where the best returns can be obtained.

Managed by Ciaran Mallon, Invesco Income Growth Trust is certainly unloved after three straight years of underperforming the FTSE All-Share Total Return benchmark. Its focus on UK equities is doing it no favours as this part of the investment world has de-rated on Brexit fears.

To make matters worse, there are various negative points working against the trust. Canaccord analyst Alan Brierley suggests it doesn’t need six people on the board given it isn’t a large trust. He also implies Invesco hasn’t been very good at marketing the product and he is disappointed that long-standing directors have only invested a small amount of their own money in the trust.

Those are the negatives – if you look deeper you will find plenty of reasons to buy while everything looks bleak. The trust is trading close to 15% below the net value of its assets which Brierley says is the widest since the TMT bubble in 2000. That means you can get access to some fantastic companies for much less than they are worth. The yield is also good at 4.2%.

Its portfolio contains a mixture of small and larger companies with growing earnings including pubs group Young’s (YNGA:AIM), chemicals specialist Croda (CRDA) and credit checking specialist Experian (EXPN).

Thomas McMahon, investment trust analyst at research group Kepler, says: ‘Providing a stable and growing dividend is one of Ciaran Mallon’s key priorities, and the trust hasn’t cut its dividend for over 20 years.

‘Over the past decade, the trust’s dividend has grown by an average of 3% per year, well above the 2.2% average for the CPI rate of inflation and above the 2.8% average for RPI over the period.

‘Mallon’s balanced, cautious approach could appeal to those who prioritise a stable and growing dividend over aggressive capital growth.’

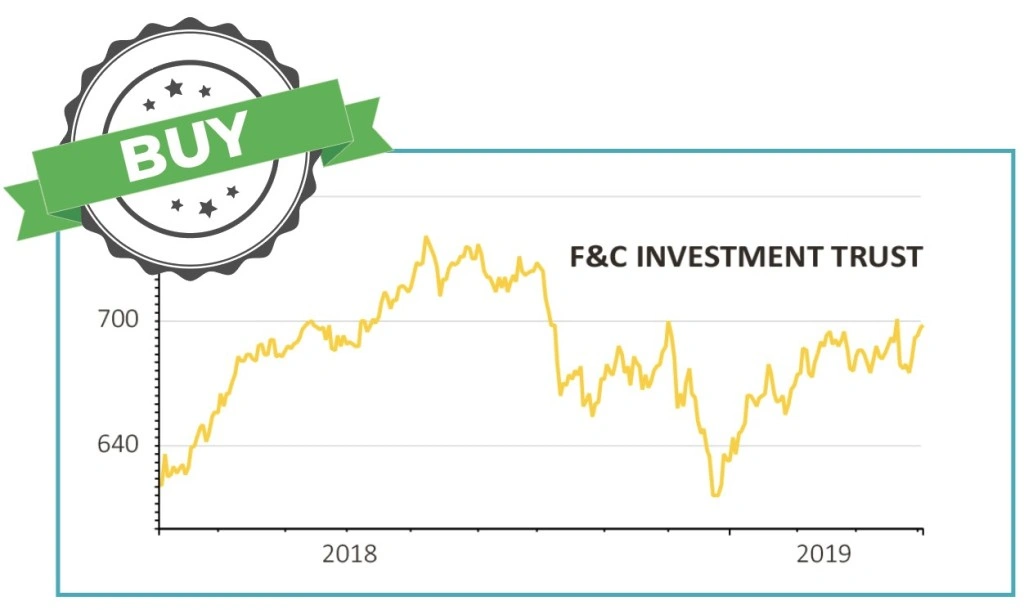

F&C Investment Trust (FCIT) 697p

Premium to NAV: 0.3% – OCF: 0.56%

Formerly-known as Foreign & Colonial, the 150-year-old trust has been run by the experienced Paul Niven since 2014, with its different portfolios largely steered by external managers.

As part of reaching its century-and-a-half milestone in 2018 the fund has reshuffled its portfolio, with the result that its shares have consistently traded at a premium to net asset value in the last 12 months. There are suggestions it could buy back shares if they returned to a material discount.

F&C has the flexibility to invest in companies not quoted on a stock exchange and in private equity, as well as quoted firms.

It provides genuine global diversification at a time of considerable political and financial domestic uncertainty.

Having fallen to 5% of total holdings, UK investments have now been folded within a pan-European sub-portfolio.

The top holding in the trust is Amazon at 2%, with software business Microsoft second at 1.8%.

On a five-year view, F&C has achieved a share price total return of 104.3% against 75.6% for its FTSE All World benchmark.

F&C suggests the trust may appeal to someone looking for their first investment or a building block for their portfolio. It would also suit someone looking to invest their money over numerous years or a person interested in regular dividends with payments made four times a year, although the current yield isn’t that generous at 1.6%.

Winterflood Securities comments: ‘In our opinion F&C Investment Trust offers investors diversified, low-cost, well-managed exposure to global equities, with a lower level of volatility than many of its peers.’

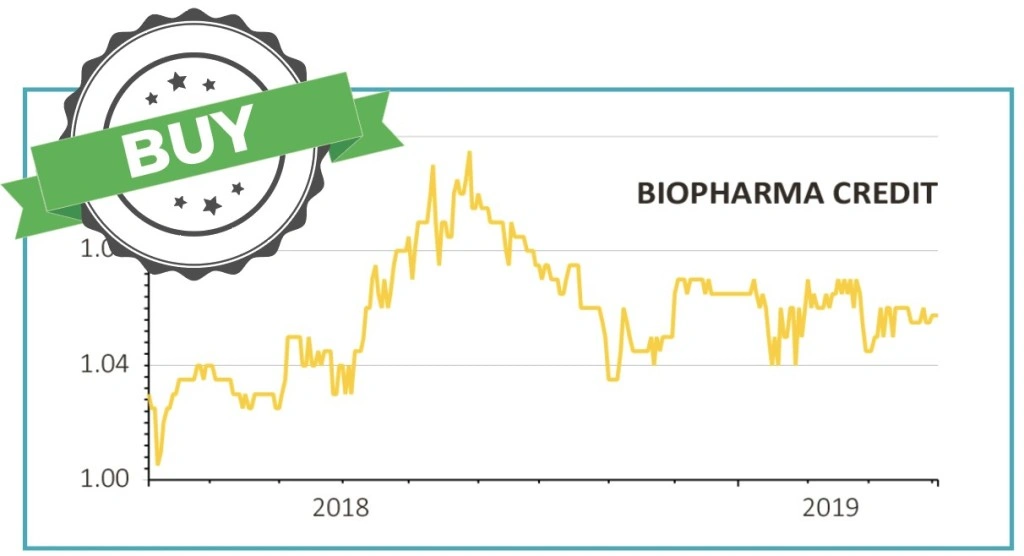

BioPharma Credit (BPCR) $1.05

Premium to NAV: 2.1% – OCF: 1.47%

Biopharma credit may suit an individual seeking to diversify their income streams via a fund where returns have a low correlation with equity markets. It isn’t for the faint-hearted as the fund isn’t easy to understand and so we suggest only more sophisticated investors take a look.

BioPharma is London’s only listed specialist debt investor in the life sciences industry. It yields an attractive 6.6% and delivered annual price and net asset value returns of 15.35% and 13.27% respectively in 2018.

Strong investor appetite for the strategy has enabled the investment trust to issue new shares and grow in size.

Manager Pharmakon invests mainly in corporate and royalty debt secured by cash flows derived from the sale of approved life science products.

Last year saw the trust significantly increased the scale and diversity of the portfolio. For example it deployed $194m as lead investor for a loan to a subsidiary of Sebela Pharmaceuticals, a private speciality pharmaceutical company focused on gastro-intestinal medicines, dermatology and women’s health.

BioPharma Credit also made $150m senior secured loan agreements with oncology group NovoCure and Amicus Therapeutics, a rare metabolic disease-focused biopharmaceutical firm.

Demonstrating the healthy returns on offer, GlaxoSmithKline’s (GSK) recent $5.1bn takeover of NASDAQ-listed Tesaro, then the fund’s biggest holding, saw BioPharma Credit receive a princely $370m payment on its $322m share of a loan. It benefited from repayment of the loan and an early repayment fee.

Around 50% of the fund’s assets are currently in cash, so Pharmakon will be under pressure to deploy this money wisely in new investments.

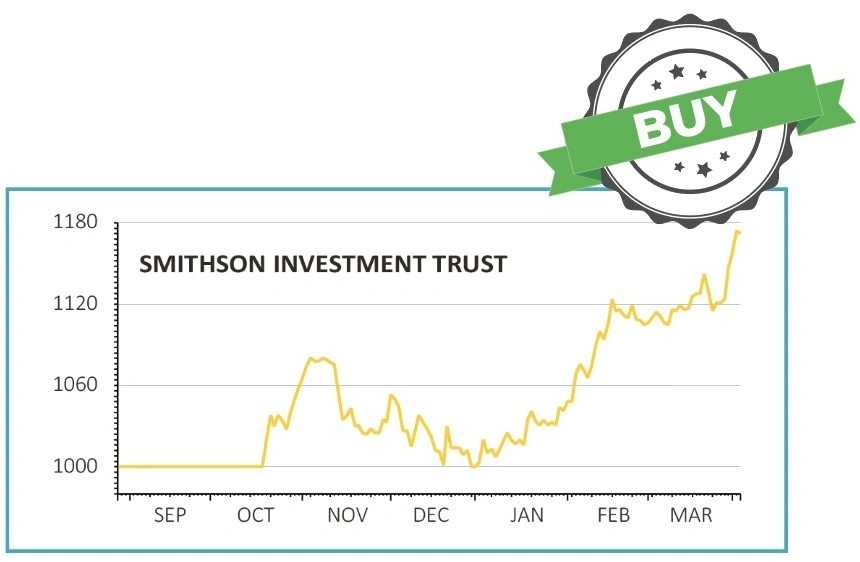

Smithson Investment Trust (SSON) £11.72

Premium to NAV: 3% – OCF: 1.05%

Fundsmith’s newest investment trust is on a roll with its shares enjoying a decent rally since the start of the year. Its launch last October certainly looks well timed as it was able to take stakes in companies during a weaker time for the market, so it could have picked up some relative bargains.

Smithson is following the same investment approach that has made Fundsmith Equity Fund (B41YBW7) so successful, albeit focusing on the mid-cap space rather than very large companies.

We believe it is an ideal holding for someone seeking to build a diversified portfolio and is happy to buy and hold for at least five years. This might be someone using a Lifetime ISA to save for retirement, an individual in their 20s, 30s, 40s or 50s using an ISA or a SIPP, or indeed it would be suitable for an investment in a Junior ISA.

One could even make an argument for owning the shares during the early stages of retirement although Smithson has guided that it doesn’t expect to generate a significant income from its portfolio so that might put off retirees who are relying on dividends to fund their lifestyle. Ultimately investors would principally own the shares for capital gains.

Smithson invests in high quality businesses around the world. The portfolio currently includes data analytics provider and credit scoring expert Equifax, medical technology group Masimo and IT security firm Check Point.

We acknowledge that it has a short performance track record and that some investors may not like the fact that Terry Smith who runs Fundsmith Equity Fund isn’t the fund manager on Smithson.

However, the people running the trust – Simon Barnard and Will Morgan – are following a proven investment process and still confer with Smith about their investment decisions.

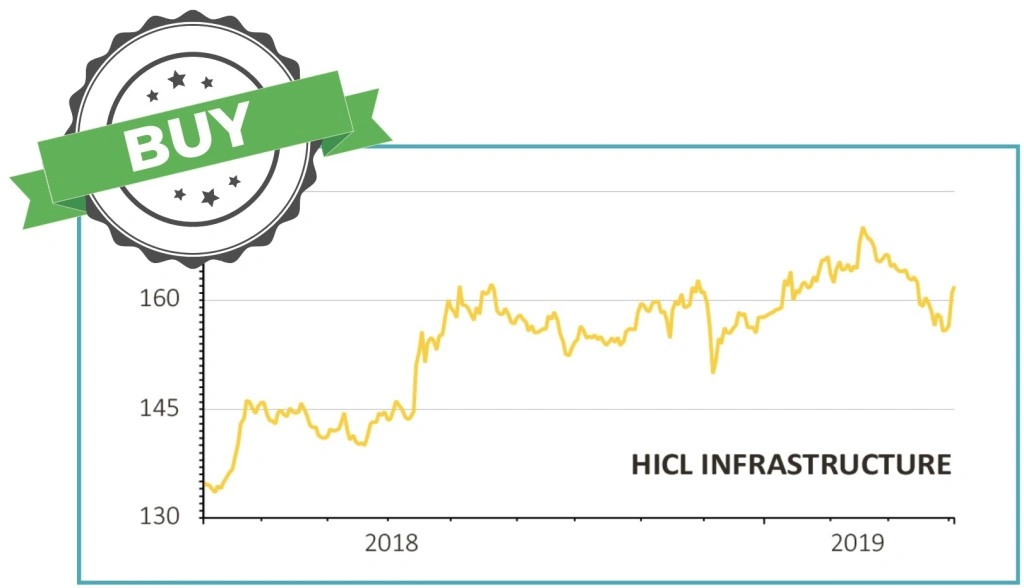

HICL Infrastructure (HICL) 162.7p

Premium to NAV: 4.1% – OCF: 1.26%

Despite heightened political risk due to Brexit uncertainty as well as growing nationalisation concerns with Labour eyeing 10 Downing Street, HICL Infrastructure stands out thanks to diversification by asset risk, a growing dividend backed by predictable cash flows and strong inflation correlation.

Admittedly, the collapse of Carillion highlighted a sector negative in the transfer of counterparty risk to infrastructure fund investors.

Furthermore, HICL really needs to stay disciplined in terms of pricing as market demand for infrastructure investments is high in a low rate environment.

Nevertheless, Shares considers HICL a canny play for investors seeking a progressive, quarterly dividend-paying investment with scope for capital growth.

A long term equity investor in infrastructure, HICL has defensive attributes, since the projects and assets it backs support communities and facilitate the delivery of essential public services in the UK, Europe, North America and Australia.

Managed by infrastructure specialist InfraRed Capital Partners, the investments are positioned at the lower end of the risk spectrum, spanning PPP (think social and transportation projects), regulated assets (including electricity transmission projects) and also demand-based assets (student accommodation, for example).

As the pricing of PFI projects has increased in recent years, HICL has invested in other areas such as utilities and also economic infrastructure assets such as toll roads and the HS1 rail project.

Based on HICL’s year to March 2019 target dividend of 8.05p, there’s a tasty 4.9% yield on the table.

Investment bank Stifel even suggests that HICL could be a takeover target.

Watch our video interview with HICL’s co-head of infrastructure, Harry Seekings

JPMorgan Claverhouse Investment Trust (JCH) 716p

Discount to NAV: 1.08% – OCF: 0.76%

A solid re-rating of JPMorgan Claverhouse Investment Trust’s stock so far this year needn’t put investors off given the trust’s stellar track record. Since switching to a more concentrated, fundamentals-backed strategy in 2012, net assets have increased by 87.1%, about a third better than the FTSE All-Share.

Yet the shares remain some distance off the 750p to 780p range where they spent most of 2018.

This is a popular investment trust selection for investors who want attractive income returns to bolster capital growth, particularly those happiest putting their money to work in UK-listed companies. That it pays quarterly dividends suits both those looking to reinvest back into the market, and investors using regular income to pay their bills.

It has raised its dividends annually for more than 40 years and yields approximately 4%.

The investment trust invests in a mixture of growth and value stocks largely drawn from the FTSE 100, although stakes in smaller companies augment the portfolio. This explains a relative who’s-who of FTSE 100 names among its largest holdings, such as Royal Dutch Shell (RDSB), GlaxoSmithKline (GSK) and drinks giant Diageo (DGE).

The managers are not afraid to hold stocks out of favour with the market. These include a stake in BT (BT.A), believing that its war of words with regulators is easing off, and in commercial property through Segro (SGRO), thanks to its structural growth levers.

Financials remain its biggest UK bet. Trustnet data ranks the trust as the UK’s fifth best performer over a five-year period within the UK equity income field.

DISCLAIMER: Editor Daniel Coatsworth owns shares in Smithson Investment Trust referenced in this article.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- The week's big news: Saga, Debenhams and more

- Funding Circle income fund to close after performance flop

- Brexit blamed for worst business investment figures since 2008

- Superdry shares still weak despite Dunkerton win

- Jupiter European funds downgraded as star manager set to step down

- Lack of IPOs is bad news for brokers