Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSurf the ‘third wave’ of healthcare innovation with Syncona

Life science focused investment trust Syncona (SYNC) generated an excellent net asset value (NAV) total return of 37.9% for the year to 31 March 2019, building on the previous year’s impressive 18.7% advance.

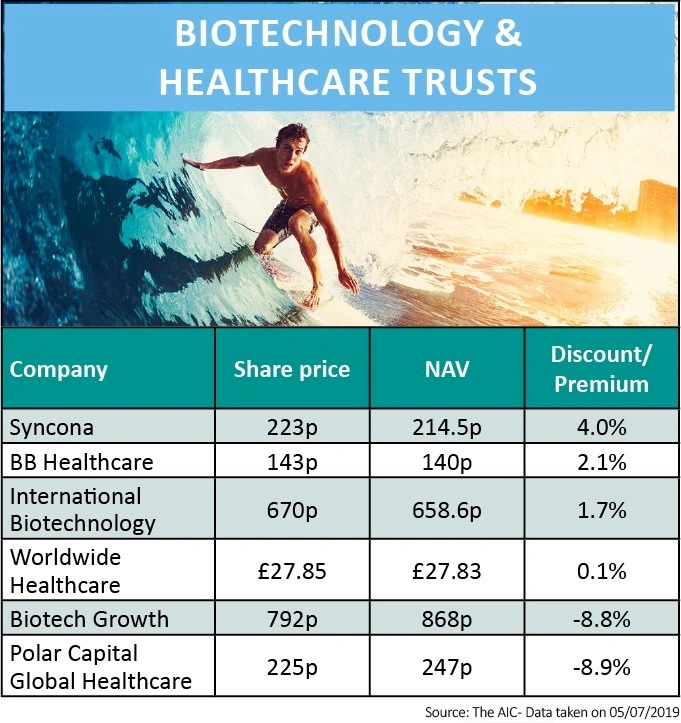

Following a share price drop from April’s 294p high point to 223p, this well-followed fund now trades at a more modest 4% premium to net asset value (NAV).

This could interest investors keen to back a FTSE 250 healthcare company with an impressive record of creating shareholder value and commercial therapies to boot.

Following its latest successful portfolio company sale, Syncona’s capital pool has risen to £963m. That accounts for around 72% of the current NAV, so investors are pricing in this ‘cash drag’ on performance and the fact drivers for its other unlisted, early stage investments over the coming 12 to 18 months are less visible.

And there are risks to weigh. Despite the share price decline year-to-date, Syncona still trades at an NAV premium, so investors are still having to pay over the odds to access the potential of the underlying portfolio.

New early stage investments will take time to deliver and asset write-downs cannot be ruled out given the risky industry in which the trust operates.

SYNCONA 101

Formed in 2016 out of the merger between Battle Against Cancer Investment Trust (BACIT), a closed-ended fund of funds, and the life science investor Syncona Partners, Syncona focuses on investing in and building global leaders in life science. Besides exciting, high quality investee companies, the portfolio consists of a large strategic capital pool of cash and fixed income products.

Under chief executive officer Martin Murphy, Syncona is differentiated from sector peers by being typically the founder and largest shareholder of its portfolio of assets, a risky approach that has proved a successful formula to date.

Unlike peers, Syncona adopts a high conviction, preliminary stage investment strategy, and has the ability to take majority stakes and support portfolio companies.

The legacy BACIT/fund of funds portfolio is becoming history, yet it has left current day Syncona well endowed in terms of cash, so the trust hasn’t needed to raise capital.

BACIT used to donate 1% of its NAV to cancer research charities each year, a philanthropic aspect of the trust which attracted investors and allowed it to access many funds at discounted terms.

That contribution continues with 0.3% of NAV, so Syncona retains a cancer cure angle, although it is now a riskier, albeit strongly performing, investment proposition than BACIT.

In its results statement covering the year to March, Syncona set aside £4.3m in donations to support charities in the field of healthcare, in particular cancer, taking total charitable donations since the company was established in 2012 to £27.1m.

STRATEGIC DEEP DIVE

Syncona’s stated vision is to ‘deliver transformational treatments to patients in truly innovative areas of healthcare while generating superior returns for shareholders’.

Sector luminary Murphy and his team seek to partner with ‘the best, brightest and most ambitious minds in science to build globally competitive businesses’. Syncona is an established leader in gene and cell therapy and focuses on delivering ‘dramatic efficacy for patients in areas of high unmet need’.

The company has gone to the lengths of being the founding partner for its carefully handpicked early life science start-ups, helping build the companies and recruit their management teams together with leading academics.

A strong and extensive academic relationship includes links to University College London (UCL), the Institute of Cancer Research (ICR) and its connections with Wellcome Trust to access the best researchers, entrepreneurs and start-ups.

Wellcome previously backed Syncona Partners and remains the largest shareholder of the Syncona we know today with a 28% stake. In addition, Syncona proactively reaches out to leading scientists and supports them with funding and commercial expertise.

This higher reward approach comes with commensurate higher risk, because Syncona bears the majority of the funding burden for its focused portfolio and takes equally large exposure to the risks of failure.

This is much more risky than committing smaller amounts each to a highly diversified, relatively latter stage portfolio of assets that already boast clinical validation.

To date, Syncona has founded and funded Autolus, Nightstar, Blue Earth Diagnostics and Freeline in collaboration with leading academics and research institutes.

HEALTHY RETURNS

Sparkling NAV gains since formation have been driven by the fruition of early investments in Blue Earth Diagnostics as well as Autolus, a clinical-stage biopharma company developing Chimeric Antigen Receptor CAR-T therapies for haematological cancer and solid tumours.

This venture completed an IPO on NASDAQ in June 2018 and Syncona retains a 30.4% stake.

Nightstar, a gene therapy company for inherited retina diseases that floated on NASDAQ in 2017, was recently acquired by Biogen for $877m. That takeout price represents a 4.5 times return on Syncona’s original investment and a 72% internal rate of return (IRR), with the recently received proceeds of £255.8m further boosting the cash coffers.

BLUE EARTH & THE NEW KIDS ON THE BLOCK

In its most recent positive development, Syncona announced the sale of Blue Earth Diagnostics to Italian-based diagnostic imaging leader Bracco Imaging for $475m or £374m, out of which £337m will be distributed to Syncona for its 89% stake.

The sale delivered a 10 times multiple (including prior distributions) on Syncona’s original £35.3m investment and represents an IRR of 87%.

Founded and funded by Syncona in 2014, the now profitable Blue Earth Diagnostics develops and commercialises molecular imaging agents with a commercially available product called Axumin, which is standard of care for the diagnosis of recurrent prostate cancer patients in the US.

These Blue Earth proceeds have strengthened Syncona’s strategic capital pool and enhanced its ability to build and fund portfolio companies that are scaling rapidly.

Syncona’s new kids on the block include Freeline, a gene therapy company for chronic systemic diseases, as well as other earlier stage but promising businesses such as Gyroscope, Achilles, SwanBio, OMass, Anaveon and Quell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.