Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat sort of economy will the new Prime Minister inherit?

As they continue to jostle for position, Boris Johnson and Jeremy Hunt are starting to outline their policies on tax and spending, areas that could both have an influence on the trajectory of the UK economy, regardless of whether Brexit happens on 31 October or not.

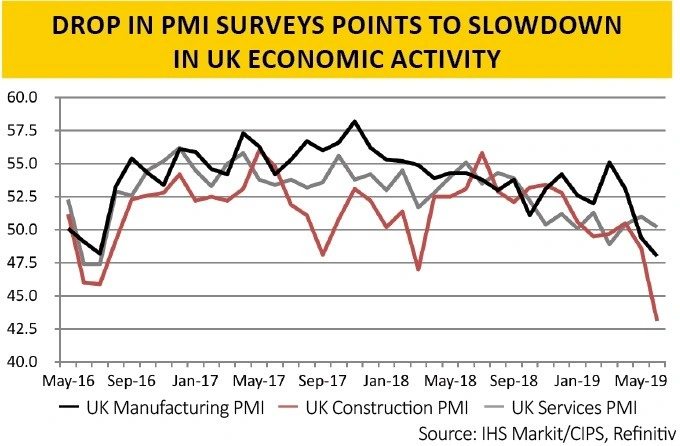

It is therefore worth taking stock of how the UK economy looks right now to see what the new Prime Minister will inherit. At first glance, the omens are not great. The latest purchasing managers’ indices showed a slowdown in manufacturing and a slump in construction, as well as a near-stalling of activity in the dominant services sector.

Whether this is down to Brexit or a wider global slowdown is not easy to divine. If the monthly PMI surveys prove to be a reliable guide then the UK economy could shrink in the second quarter versus the previous three months – the first such drop since the fourth quarter of 2012.

There has been a deceleration in growth of household consumption since the Brexit vote in summer 2016 to a run-rate below 2%.

The good news is that wage growth is nearing 10-year highs and outpacing inflation. Proposed tax cuts from the Conservatives could add around 1.5% to household income, although Labour’s proposed tax increases could take off around 1.0%, according to estimates from Capital Economics.

Interest rates could go down before they go up, depending on Brexit. Perhaps a bigger wild card is the savings rate which at 4% of disposable income is near historic lows and any increase could act as a brake on spending.

Investment also appears to have slowed ahead of Brexit. This can be seen in the manufacturing PMI but also the investment intentions reading from the Bank of England’s agents survey.

If businesses get some degree of visibility over Brexit, they may start to loosen the purse strings but the risk is that the global economy slows. This is something that we could already be seeing, judging by the easing in capacity constraints shown by the same Bank of England report.

Growth in Government spending looks set to accelerate, given Johnson and Hunt’s policy plans – and that is before anyone dips into Chancellor Philip Hammond’s £26bn of fiscal headroom. This is not a pot of cash, but extra spending that would take the UK’s annual budget deficit back to 2% over the next five years.

A Labour government could lead to another step up, although increased taxation could have some impact on consumer and corporate spending.

Export growth has sagged of late while import growth has surged. The soggy exports may be the result of a global slowdown in business activity, which is becoming more marked as a result of trade disputes between the US and its major trading partners.

GLOBAL ANGLE

The UK’s fortunes cannot be seen in isolation. The identity of the new Prime Minister and his policies, the response of the EU and Westminster to Brexit and the action they in turn prompt from the Bank of England provide plenty of variables. And that’s before the possibility of a Labour victory in a general election between now and 2022.

Then there is the issue of global growth on top – and this may be the most important of all, at least from a stock market perspective.

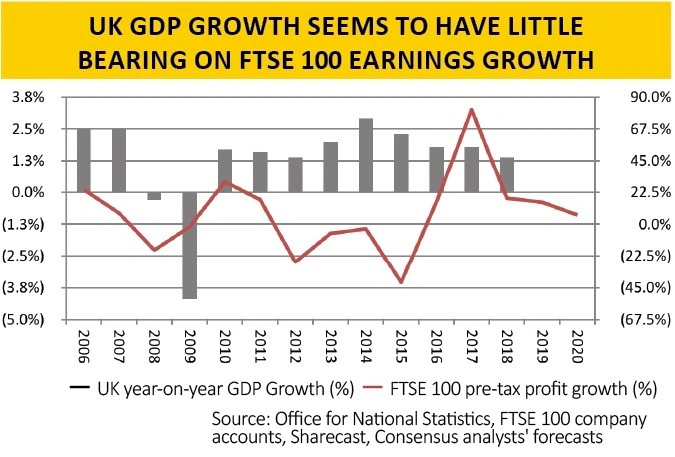

Two-thirds of the FTSE 100’s revenues come from overseas and there is little apparent correlation between UK GDP growth and the rate of change in aggregate FTSE 100 profits.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.