Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe FTSE 350 stocks making our lives better

Invest in what you know is the golden rule for first time investors. This advice has stood the test of time and is a great way for people to get to know what investing is all about.

Fortunately, there are many companies on the FTSE 350 which are household names.

But when you get more comfortable with investing and how the stock markets generally work, there’s a whole host of companies less familiar to the general public, but which are vital to our everyday lives.

They could one day make you a mint or least keep your money ticking over nicely.

Having looked at FTSE 350 consumer stocks last week we now take a look at those working behind the scenes, the quiet operators of the index which in one way or another help provide the heating in your house, the engine in your car, or just generally make sure you’re able to do your online shopping, for example.

In industries such as chemicals, engineering and oil and gas services, we also pick five of our favourites among these unsung heroes.

Next week (5 September) conclude our FTSE 350 series by looking at the FTSE 350 stocks with inflation-busting dividend growth.

In an age where the UK’s reputation may have taken a battering from Brexit, good old British engineering still flies the flag for the country globally, and as such is well-represented on the FTSE 350.

Aside from engine-maker Rolls-Royce (RR.), you may not have heard of most of the engineering firms in the index such as IMI (IMI), Spirax-Sarco (SPX) and Weir (WEIR).

Many of them provide specialist products in niche areas of the market, meaning they are considered to be in a good position to weather the storm of a no-deal Brexit and/or escalations in US/China tensions. However, investors have been nervous to own them, as reflected by widespread share price declines in the past year.

Cybersecurity has become an ever increasing part of our lives, thanks to the rapid rise of technology and the corresponding spike in digital crooks.

There are two main players in the FTSE 350: Sophos (SOPH) and Avast (AVST). Sophos is likely to be the one that keeps your employer safe online, while Avast would be the one that keeps you safe online.

Both have opportunities aplenty going forward, given that the global market is expected to be worth $1trn by 2021, compared to the $120bn it was worth in 2017.

So many products are now bought online and delivered straight to our doors. While the delivery companies may seem to be the unsung heroes, it’s worth considering the packaging guys, without whom our

love of online shopping may never have grown so big.

FTSE 350 group DS Smith (SMDS) is the one that makes those cardboard coverings you get when you buy something off Amazon, while shares in big-time wrappers Mondi (MNDI) and Smurfit Kappa (SKG) also trade on the UK stock market.

Packaging firms tend to be cyclical and sell off when investors get worried about global growth, hence why the sector has been weak of late. Yet there is still long-term structural growth driven by online shopping.

Oil and gas firms power our world. A structural shift to renewable energy is under way across the globe, but oil and gas still make mega bucks and in a recent Forbes list the industry had the most profit growth globally.

Nonetheless, oil prices in particular can be highly volatile and would be vulnerable if there is a slowdown in global economic growth, something markets are quite scared about at the moment.

Aside from BP (BP.) and Royal Dutch Shell (RDSB), most oil and gas firms in the FTSE 350 tend to be explorers, and one in particular, Tullow Oil (TLW), has made strong gains this month following a major oil discovery.

Mining companies are among the biggest in terms of market value in the FTSE 350 index. They are important, digging metals and minerals out of the ground that are vital to our everyday lives such as copper which is a bellwether for global trade due to its widespread use.

The sector has some big, dividend-paying companies like Anglo American (AAL), BHP (BHP) and Rio Tinto (RIO) which produce lots of different commodities.

Others only focus on one thing, such as gold or copper. Gold miners in particular have done well recently as the gold price soars due to worries over the world economy.

If you’ve bought a new build house, you may know the name of the company who built it. But you probably don’t know the company that built the road leading up to your house or who provided the materials to build the road.

In the FTSE 350, Balfour Beatty (BBY) is an example of a company doing building work. But its share price now is no higher than when it first listed back in 1995, and these types of companies – called contractors – are struggling in the current environment. You only have to look at the woes of Carillion and Kier (KIE).

An alternative is to look at companies supplying materials, such as CRH (CRH), Marshalls (MSLH) and Keller (KLR), who have performed strongly this year.

5 ‘MAKING OUR LIVES BETTER’ STOCKS TO BUY NOW

JOHNSON MATTHEY (JMAT) £28.55 BUY

Chemicals expert Johnson Matthey (JMAT) makes most of its money, around 70% of its total revenue, from catalytic converters, which reduce the toxicity of gases from your car before they’re released via the exhaust.

The FTSE 100 firm has had a volatile couple of months, disappointing investors with underwhelming first quarter growth figures.

But long-term, investors remain excited about the company’s prospects. Not because of its catalytic converter business, but because of a tiny part of its business that could become a significant source of revenue in the future.

In this division, called New Markets, Johnson Matthey is developing a type of battery that could disrupt the whole electric vehicle market.

The firm has invested heavily in developing enhanced lithium nickel oxide, or eLNO for short, which has a higher energy density than all other battery materials, making it a lot more attractive for electric vehicle manufacturers.

The firm recently told investors it needs a much better second half of the year if it is to meet full year expectations, so the share price could be volatile in the short-term. But if it gets eLNO right, it has the potential to be a strong long-term winner.

HILL & SMITH (HILS) £11.41 BUY

If you’ve ever driven down a motorway or ridden a train across a bridge you’d have seen some of Hill & Smith’s (HILS) safety infrastructure products.

It manufactures the roadside crash barriers placed on bends or the central reservation of motorways, as well as bridge-side fencing, street lighting and pipe network supports. It also has a galvanising business that provides zinc corrosion coating protection against rust.

It’s one of those key suppliers whose kit helps keep the UK and all of our day-to-day lives ticking along smoothly. It is also a capital growth and income returns story worth knowing, one that has increased dividends every year since 2002, typically in the high single-digits or better.

The stock has hit the skids over the past year after a series of project delays, partly due to the previous Beast from the East winter, but it seems to be back on track.

Half year results on 7 August underlined robust road infrastructure spending both in the UK and in the US as the company posted double-digit increases in revenue and earnings.

A 2020 price-to-earnings multiple of 13.1 is good value for a business noted for its ‘strong medium-term outlook,’ as one analyst puts it, even with the uncertainties surrounding Brexit.

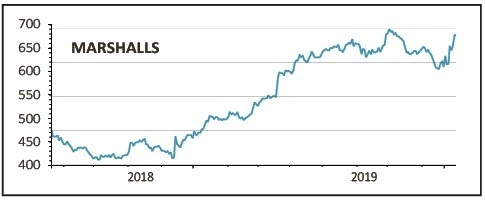

MARSHALLS (MSLH) 676p BUY

Specialist building products firm Marshalls is focused on landscaping products such as bollards and paving slabs. Despite an uncertain outlook for the wider construction space, it continues to tick along nicely with 10% like-for-like growth in first half sales in 2019.

A recently refreshed strategy out to 2023 will see the company continue to focus on areas in which it sees long-term potential including housebuilding and transport infrastructure.

The company is also investing in innovative new products and in upgrading its digital platform, which should make its products more accessible to clients.

The shares aren’t cheap at 22 times forecast earnings but we think it is worth paying up for a quality business which has a clear plan of how to thrive in the future no matter the market backdrop.

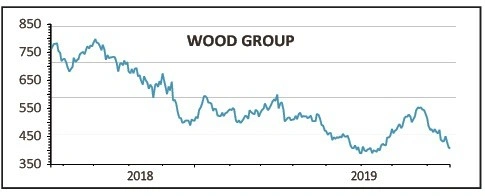

WOOD GROUP (WG.) 397.1p BUY

Wood Group is a more diversified business since its $11bn merger with Amec Foster Wheeler in October 2017, with exposure to areas like renewables and industrial manufacturing alongside its more traditional oil and gas focus.

The business provides a range of services, from supporting oil rigs in the North Sea and improving the performance of industrial equipment, to running and maintaining clean energy projects.

First half results were a bit untidy with a fair number of adjustments but still showed a solid performance overall as the company swung to a $13m profit for the period. Unchanged full year guidance was also underpinned by the fact 87% of 2019 revenue has already been secured or delivered.

A key sticking point has been the company’s elevated debt position but the £250m sale of its nuclear business will help the deleveraging process.

Reducing borrowings could also help unlock the value in the shares which trade on 8.2 times 2020 earnings and yield around 7%.

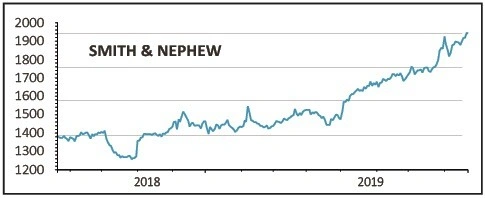

SMITH AND NEPHEW (SN.) £19.47 BUY

Medical devices firm Smith & Nephew (SN.) is well positioned for growth, targeting the right markets with the right products.

While the historic track record for the business has been patchy at times, recently-appointed CEO Namal Nawana has wasted no time in reinvigorating the business since his appointment in May 2018.

Under Nawana there is a more focused approach built on three key pillars: orthopaedics, sports medicine and advanced wound management.

Orthopaedics is the largest of these at 44% of revenue and makes replacement hips and knees. The sports medicine arm, which uses implants to treat ligament tears and ruptures, is benefiting from demographic changes which see an increasing number of people stay active into later life.

The company’s wound management division has a fast-growing component in active healing where materials used on wounds help heal through the release of antiseptics or plant extracts, for example.

The company’s mid-single-digit organic growth could be augmented by M&A activity in expanding markets, something Nawana has signalled as a priority.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.