Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow much are you taking from your pension?

Half of people who are taking money from their pensions are doing so without taking any advice, new figures show.

Data from the Financial Conduct Authority, a regulator, showed how people in retirement are making use of the pension freedoms – the reforms in 2015 that allow people to access their pensions more freely.

For the period from April 2018 to March 2019 it found that 48% of people took money out of their pension after taking no advice or guidance, while 15% took no advice but did consult the Government’s PensionWise guidance service.

The remaining 37% of people took financial advice before taking money. The figures also showed that four in 10 people who accessed their money had a pension worth £10,000 or less, meaning some may not think their pot is large enough to warrant getting advice.

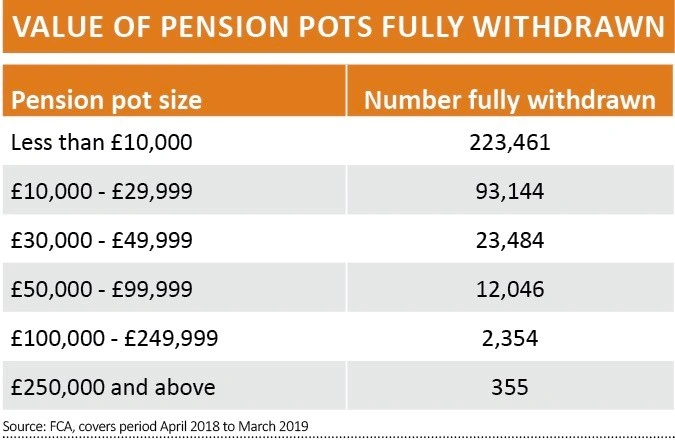

What’s more, 355,000 pensioners took their entire pension in one go when they first accessed it. While some may be doing so because they only had a small amount in that pension pot, others may be falling foul of high tax bills just to access their money.

WATCH OUT FOR TAX ISSUES

The way tax is paid on pension withdrawals is clumsy, and means that your first withdrawal is taxed as though that sum will be taken monthly. It means that many people who make a one-off withdrawal from their pension are charged far too much tax and have to go through an onerous process of claiming it back.

The new data shows that while 90% of the pension pots that had been withdrawn entirely were worth less than £30,000, many took much higher sums. In the most extreme cases, 355 people withdrew pots worth £250,000 or more, while 2,354 people took out pots worth £100,000 to £250,000.

Tom Selby, senior analyst at AJ Bell, says: ‘For some of these people there could be legitimate reasons they would want to access this money, for example being in ill health and having no desire to leave money to beneficiaries. But for some it will simply be a desire to get their hands on the cash.

‘Far too few people are seeking advice or guidance about crucial retirement decisions across the board, and boosting these numbers needs to be a priority for the regulator. The nature of the pension freedoms means while some will use their new found flexibility responsibly, others risk sleepwalking into disaster. Increasing take-up of advice and guidance is crucial to help mitigate this risk.’

Keith Richards, chief executive of the Personal Finance Society, says: ‘The Government and the FCA [should] do more to make sure providers are signposting guidance services and advice and explaining the potential ramifications if you don’t seek assistance. We want to make sure that nobody ends up making the wrong retirement income choice.”

ANNUITIES CONTINUE TO DWINDLE

People are continuing to favour keeping their pension pot invested rather than buying an annuity. A big part of the pension freedoms was removing the requirement for people to buy an annuity when they retired. It meant that many more people chose to keep their pension invested and take an income from the pot.

The figures show that 74,000 people chose to use their pension to buy an annuity in the year, compared to the 191,000 people who started taking an income from the pot.

However, the regulator did flag that some people are taking very large income from their pension pot – in total 40% of withdrawals were 8% of the pension pot or higher. The number taking such large incomes from their pots reduces as the size of the pot grows, for example, 14% of people with pots worth £250,000 or more are taking withdrawals of 8% or more, compared to 74% of those with pots worth £10,000 or less.

It is impossible to know whether these withdrawals are sustainable for individuals without knowing their specific circumstances. Someone with a significant defined benefit pension pot, for example, might be able to draw from a second pension at a faster rate without putting their retirement future at risk.

Some may have seen strong investment performance in their pension that they want to benefit from. Others may be taking far smaller incomes from their pot as they are relying on ISA savings, or attempting to preserve the pension pot to pass on to future generations.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.