Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStrap in for the car sector recovery

Britain’s automotive industry has stalled as low global demand and weak domestic consumer confidence weigh on sales, profits and sentiment.

Disruption is impacting the global car industry and many of the businesses whose fortunes are tied to the automotive sector are in for a very bumpy ride. Yet those able to adapt to the shifting landscape could see exciting times down the road.

In this article, Shares examines the headwinds putting the brakes on growth and poses the question, ‘is there value in the broader automotive sector for contrarians?’

GLOBAL GRIND

Automotive is among the globe’s most challenged industries with air quality and CO2 reduction at the top of the priority list.

Diesel sales have slumped following emissions scandals – Volkswagen is still trying to repair the reputational dent – while the trade war between the US and China is triggering slowdowns in the European and Chinese markets.

Original equipment manufacturers are cutting costs while investing in new product developments in the area of vehicle electrification – everything from hybrids to full battery electric vehicles, connected vehicles, vehicles with greater autonomy and virtual product development.

COLLISION COURSE

Alarmingly, the CEO of car parts supply colossus Continental, Elmar Degenhart, has warned of an ‘emerging crisis’ in the auto industry as his charge drives through a major restructuring.

The company is responding to a decline in global automotive production fuelled by digitalisation and the rapid shift to battery-powered vehicles, boosted by stringent emissions and fuel-efficiency regulations.

On the home front, Brexit uncertainty has meant investment in British factories has stalled. Aston Martin Lagonda’s (AML) shares recently hit the skids again after the luxury brand announced (25 Sep) it had raised $150m from a bond issue on a very high rate of interest, with the option to raise another $100m if order targets are met, to bolster its cash position against a dire backdrop for car makers.

YEAR-TO-DATE DEFICIT

British car factories make vehicles for companies including Jaguar Land Rover, Nissan and Mini, yet many car industry executives believe Brexit will be damaging for the sector.

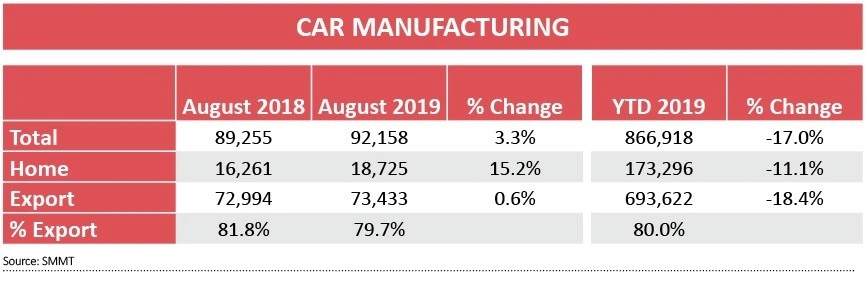

UK car production grew 3.3% in August, according to figures from the Society of Motor Manufacturers and Traders (SMMT), to 92,158 units. But this monthly growth couldn’t offset substantial April losses, meaning there is a year-to-date deficit of 17% with output failing to reach 1m units by August for the first time in five years.

August’s increase, the first in 15 months, was largely down to several key plants pulling forward planned summer shutdowns to April to guard against the disruption of the-then 29 March EU withdrawal date, which then kept their production lines rolling through the summer.

Exports registered negligible 0.6% growth in August, but even this disguised weakness in major global markets with production for China down 43.8%, exports to the US falling 9.1% and those to the EU declining 13.7% in the first eight months.

Industry representatives from 17 of the EU’s biggest car producing and buying countries, including Germany, Italy, France, Belgium and Spain, have joined forces in united opposition to a no-deal Brexit, spooked by tariffs threatening affordability on both sides of the Channel and the end of barrier-free trade bringing disruption to efficient just-in-time supply chains.

Spluttering growth engines

Other businesses being impacted by global automotive industry headwinds include engineering-to-environmental consultancy Ricardo (RCDO).

With car manufacturers distracted by Brexit and market slowdowns in Europe and China, Ricardo has seen reduced levels of orders across its global automotive businesses amid ‘uncertainty in outsourcing trends’.

This summer (8 Aug), specialist automotive firm TI Fluid Systems (TIFS), which makes automotive fluid storage, carrying and delivery systems for light vehicles, posted a drop in first half sales and earnings. Given challenging market conditions, the company said it expected revenue to continue to outperform global light vehicle production volume levels, although it anticipated this revenue outperformance for the year to be lower than the prior year.

Should you invest in a car retailer?

Risk-averse investors may recoil at the thought of climbing behind the wheel of the quoted UK motor retailers, though the sector has deep value appeal.

Car dealers are cyclical businesses with skinny margins, making money from the sale of new and used cars, higher margin car servicing and repairs and through commissions from selling credit and insurance products.

Selling new cars is crucial, because they eventually become the used cars that will require periodic (and higher margin) servicing and repair.

Until a few years ago, the UK new car market was motoring ahead thanks to easy credit in the form of so-called personal contract plans (PCPs), under which motorists rent rather than buy a car.

Consumers usually signed up to three-year PCPs where they paid the depreciation on the car plus interest, with the monthly payments reduced by any money they provided upfront via a deposit.

Some doom-mongers fear this build-up in credit is a bubble that could go pop. This is why the Financial Conduct Authority (FCA) reviewed the market, although it concluded PCP is not yet a threat to UK economic financial stability.

Electric dreams

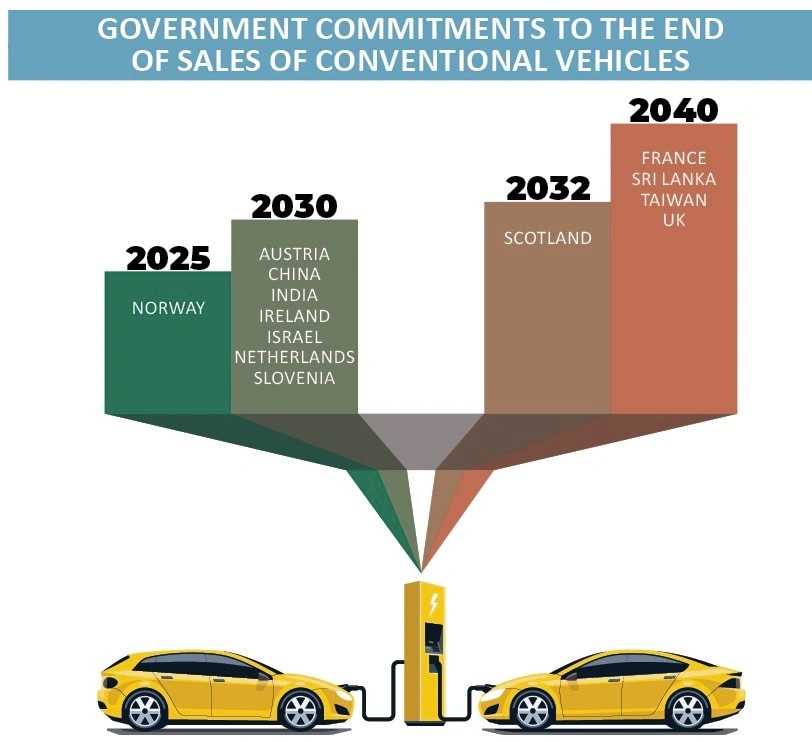

Governments including China, India and the UK have committed to bans of new gasoline and diesel vehicles, leaving electric vehicles as the obvious market replacement.

Bloomberg New Energy Finance has forecast that new sales of electric vehicles will overtake internal combustion engine vehicles by 2038. In the UK, electric vehicles are forecast to grow rapidly with National Grid’s scenarios suggesting more than 35m vehicles by 2050 with 80% of this figure hit by 2037 in the two most aggressive scenarios.

One radical question some are now pondering is whether we are nearing ‘peak car’. Neil Brown, co-manager on the Liontrust Sustainable Investment team, says: ‘Short-term problems in our auto industry are well known but we look beyond the profit warnings of 2018 and trade war tweets of 2019 to the underlying drivers.

‘Emissions controls have been an issue for decades but we believe something more fundamental is at work: the problem is not should we buy a diesel, petrol, hybrid or full electric but rather whether to own a car at all’.

DEALERSHIP PROBLEMS

As for the quoted dealerships, their challenges are legion. Consumer and business confidence has deteriorated due to uncertainty caused by the seemingly unending Brexit process.

Big ticket purchases including cars have been put on the back burner despite record high employment, with a knock-on impact for the new and used car markets, not helped by weak sterling and sharply reduced demand for diesel cars amid environmental concerns and stricter emissions regulations affecting supply.

The removal of incentives to buy plug-in hybrid vehicles has thrown up yet another roadblock.

VALUE IN THE WRECKAGE

Investors looking for contrarian opportunities among quoted car retailers need to consider if all the bad news is now priced into the shares and whether the companies have strong enough balance sheets to withstand the storms.

Interestingly, many of the car retailers have freehold and long leasehold property and their shares are now trading at less than the value of their tangible assets.

Free cash flow could start to steadily build as the capital expenditure cycle for most dealers comes to a close.

‘Looking longer term, we do believe there is a clear future for mid/large well-capitalised dealer groups and believe there is strong value on offer for long-term investors,’ wrote Zeus Capital’s sector expert Mike Allen in a recent research note.

He added: ‘Free cash flow yields are healthy across the sector and a sign of strong value emerging – we believe this will be the key catalyst to any share price recovery coupled with the stabilisation of earnings.’

Car for hire

A less obvious way of looking at the car sector is Anexo (ANX:AIM), a specialist credit hire and legal services provider for not-at-fault drivers involved in an accident.

As well as handling the customer’s claim through its legal department, Anexo provides a replacement hire car while its appointed garages repair the damaged vehicle, taking all the burden off the customer.

In the six months to 30 June turnover grew by 55% to £36.7m and pre-tax profit jumped by 63% to £11m as the firm handled a higher volume of customers and a higher volume of high-value claims.

WHAT IS THE STATE OF PLAY WITH LISTED COMPANIES?

The biggest car retailer on the London Stock Exchange is Inchcape (INCH), which is a global player. It has partnerships with high-end car brands and a higher margin distribution business at its core. Its shares have traded in a fairly narrow band this year.

Pendragon (PDG) is the largest London-listed UK car retail player whose first half results (18 Sep) revealed a bigger loss than expected and the dividend was scrapped.

Pendragon has issued a string of profit warnings amid new car market weakness and the cost of clearing legacy used car stock, while a monster cost base and management flux partially explain prevailing poor sentiment.

Investors were left reeling by the relatively recent shock departure of chief executive Mark Herbert after just three months in the hot seat following a review of the group’s profitability and strategic focus.

Pendragon’s peers include dealership Lookers (LOOK) which is facing higher costs over the next few years as it fixes issues uncovered in its sales practices.

An alternative way of investing in the car sector

S&U (SUS) owns of one of the UK’s leading car finance providers, Advantage, which serves the huge ‘non-prime’ market for cars up to £6,000 which are typically non-discretionary purchases by people who need a car for work or the school run.

In the six months to 31 July Advantage received a record 680,000 applications for credit, such is the demand for used-car finance.

Its credit criteria are so strict that only 1.8% of applications were approved, taking its total customer base to around 62,000. Turnover in the six month period was up a steady 7% to £47.7m while pre-tax profit was up 4% to £17.1m, meaning a respectable 35.8% return on sales.

Considering that the total used car market is worth over £40bn per year, and the number of used car sales on finance was up 3% in the year to July while new car sales were down, the potential market for S&U is still huge relative to its current size. We have a ‘buy’ rating on the stock.

Lookers is being investigated by the financial regulator into how it incentives staff selling car finance packages, having flagged up issues in its sales practices during an independent review of its internal control and audit processes.

Motorpoint (MOTR) in July said it was seeing market share gains against a declining market and that it remained confident. That triggered a sharp rally in the shares although they’ve since come back.

Cambria Automobiles (CAMB:AIM) said on 4 September that its results for the year to 31 August would be ahead of market expectations and the management gave fairly upbeat remarks about the company’s prospects.

OUR TOP 2 CAR RETAIL STOCKS TO BUY

VERTU

Shares remains bullish about the longer term prospects of freehold property-backed Vertu Motors (VTU:AIM), the UK’s fifth largest car retailer, currently languishing at 33.7p. That is a major discount to last reported tangible net assets per share of 44.9p.

Vertu has performed resiliently in the face of industry challenges. No-nonsense boss Robert Forrester is understandably cautious about the short-term outlook, but Vertu is well positioned to consolidate a fragmented market given its strong track record and balance sheet. Tough industry conditions mean that acquisition opportunities, including distressed assets, are increasing.

MARSHALL MOTORS

Daksh Gupta-steered Marshall Motor (MMH:AIM) also has deep value allure, reporting net assets of £200.7m or 257p per share at the 30 June balance sheet date versus a 144p share price at the time of writing.

Its first half results (13 Aug) demonstrated another sector-leading performance with healthy underlying pre-tax profit of £15.2m, albeit down 5.3% year-on-year, driven by a strong outperformance in used vehicles and a ‘very respectable performance in new cars’, to quote Investec Securities.

Zeus Capital says it remains happy with the long term investment case, aided by a robust balance sheet and solid track record of execution and outperforming the wider market.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.