Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

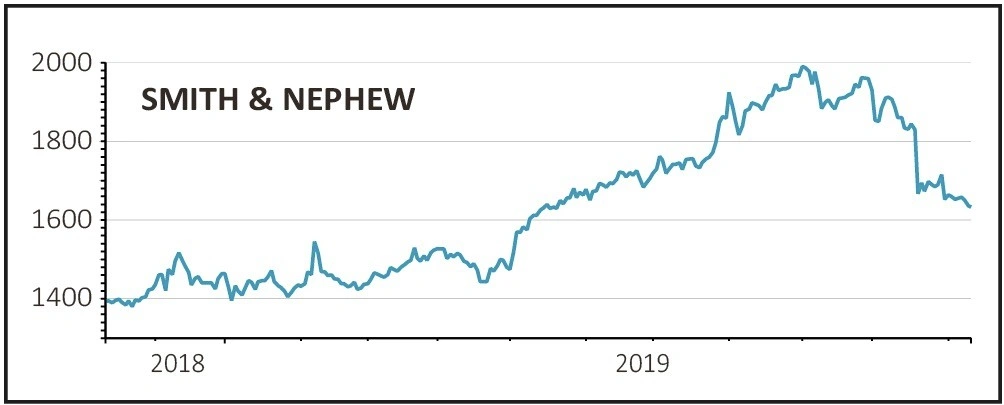

magazineSmith & Nephew sell-off looks overdone

Smith & Nephew (SN.) £16.33

Loss to date 14.4%

Original entry price: Buy at £19.09, 8 August 2019

Diversified medical devices maker Smith & Nephew (SN.) has twice upgraded its expectations for revenue growth in the past six months, demonstrating that the new operational structure is seeing tangible and sustainable commercial benefits. Sadly the shares have recently taken a dive.

On 21 October chief executive Namal Nawana resigned, reportedly over pay, to be replaced by Roland Diggelmann, who was the chief executive of Roche Diagnostics. The shares fell 9% on the day and have drifted lower since the announcement.

Nawana wanted to make acquisitions in faster growing areas and was targeting higher debt levels to accommodate up to $1.5bn of further deals.

While there aren’t doubts about the business continuing as usual under the senior management team, the acquisition side of the equation is now under more scrutiny until we hear from the new chief executive.

Narrowing the trading margins guidance from 22.8%-23.2% to ‘around 22.8%’ on 31 October also troubled investors even though this was only caused by foreign exchange, inward investment and recent acquisitions rather than something major.

We originally said the shares weren’t cheap on 21.4 times forecast earnings and they have since de-rated slightly to 19.4-times.

SHARES SAYS: We see no reason to change our positive view while business momentum remains strong.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.