Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy US equities need a trade deal

The US stock market safely negotiated October this year, as the S&P 500 index gained 2% in the month and reached a fresh all-time high in early November. The Dow Jones Industrials and NASDAQ Composite have also surged to new peaks.

Market accidents are usually caused by the combination of rising interest rates, earnings disappointments and an economic downturn or recession, in conjunction with lofty valuations which provide no protection from this trio of challenges.

The good news is that interest rates are falling, the US economy is growing and the third quarter earnings season is almost finished, with positive earnings surprises outpacing negative ones by a ratio of 4.4 to 1, according to Standard & Poor’s.

What could possibly go wrong? The answer is quite a lot and it is worth checking each of those possible catalysts for a correction, just to ensure that investors can manage risk most effectively in the context of their own personal portfolio strategy, target returns and time horizon.

Federal frenzy

It is easy to pin the latest surge in US stock prices on Federal Reserve policy. The US central bank has cut interest rates three times this year and begun to intervene in the interbank lending markets with a resumption of its bond-buying programmes.

While chair Jay Powell is insisting this is not a return to quantitative easing, the renewed expansion of the Fed’s balance sheet would say otherwise. Its assets have just swollen at the fastest pace since the height of the financial crisis in 2008.

A lot of cheap cash is looking for a home and equities seem to be a logical choice for many, as price momentum is tempting and the 1.9% dividend yield compares favourably enough with benchmark US 10-year government bonds.

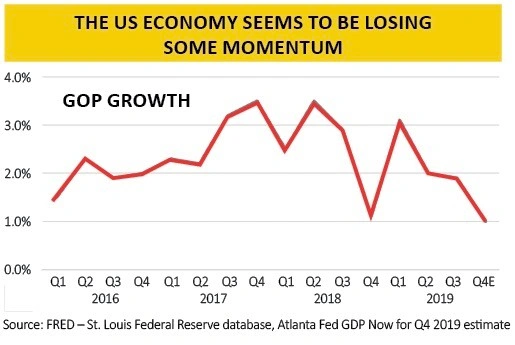

The US economy is still growing, more than a decade into the post-crisis recovery and the third quarter GDP growth number of 1.9% was steady enough.

However, the Atlanta Fed GDP Now and New York Fed Nowcast services are forecasting an increase in the fourth quarter of just 1.0% and 0.7% respectively.

This does hint at a loss of momentum and raises the stakes for the trade talks between Washington and Beijing in particular, since the surge in the benchmark US equity indices is at least partly predicated on Presidents Trump and Xi reaching a settlement.

Profit parade

That apparent slowdown may be weighing on corporate profits growth. The majority of US companies skipped past consensus estimates for Q3 that may have owed as much to expectations management as strong performance.

S&P 500 earnings per share (EPS) are expected to fall in aggregate in Q3, even though share buybacks are adding about 4% to the stated EPS number, so the actual operating performance is even worse.

Hopes for the future are providing support to share prices, since analysts are pencilling in a rapid return to double-digit profits growth, helped by a trade deal. Yet investors had better hope they are right.

Aggregate EPS forecasts for the S&P 500 have fallen by 8% since March 2018, according to S&P, while the index has risen by 17%. History suggests that stocks cannot defy such gravity for ever.

Price point

The other effect of prices rising as earnings estimates slide is that valuation multiples expand. The S&P 500 index trades on 19.4-times this year’s earnings and 17.5-times for next year, based on consensus forecasts. These are not unprecedented levels but they are toward the top of the range – and need the consensus earnings forecasts to be right (when they have been consistently too optimistic for 18 months).

To try and take the guesswork out of analysts’ forecasts, Professor Robert Shiller’s cyclically-adjusted price-to-earnings (CAPE) ratio looks at valuations across a 10-year cycle and adjusts for inflation. This approach suggests that US stocks have only been more expensive for any length of time on two occasions – 1929 and 1999 and both of those episodes ended very badly.

The counter-argument is that Shiller’s approach has warned about US equity valuations for years, to absolutely no avail.

If you look at the Shiller multiple and then set it against the 10-year compound annual return from US stocks that actually followed, buying at these valuation levels has never worked well on that 10-year view.

And since that is the sort of time horizon that would test the patience of many a portfolio builder, this is worth considering, especially if an investor’s style is to happily go with the flow and chase near-term momentum. And in this scenario, a trade deal would perhaps help stocks to hold their ground and not make fresh advances.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.