Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDoing the maths on the temporary stamp duty relief

Homebuyers will face far lower stamp duty bills for the next nine months after the Government vastly reduced the cost of the tax.

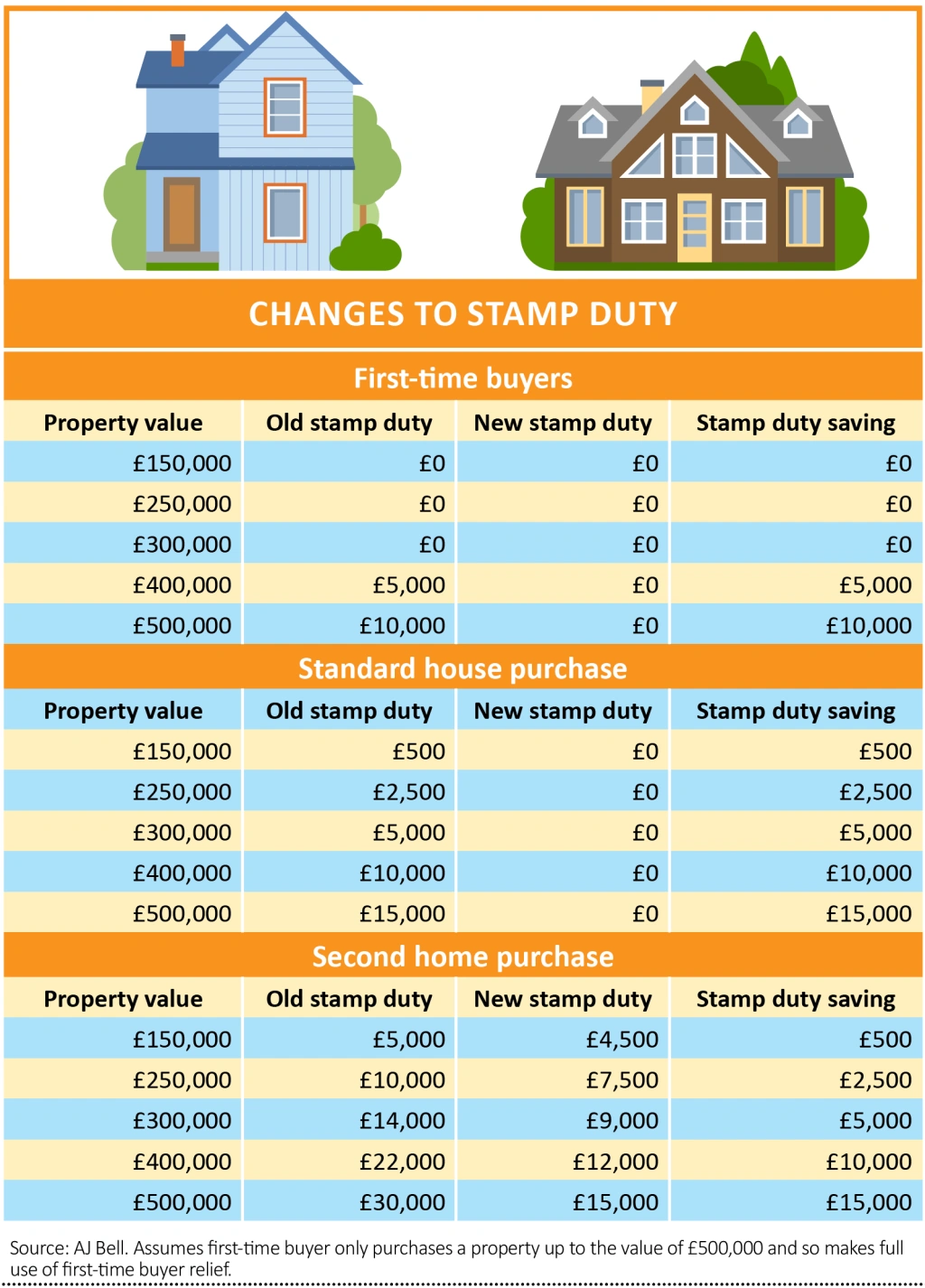

The mini-Budget from Chancellor Rishi Sunak revealed that a temporary stamp duty relief would be implemented immediately, running to 31 March 2021. Currently no-one pays stamp duty on the first £125,000 of any home purchase in England and Northern Ireland, but this will now be increased to £500,000.

The move means that anyone buying a main home worth £500,000 or less will now pay no stamp duty. It is intended to kick-start the housing market after a summer of lockdown and uncertainty about house prices. The maximum saving under the new scheme is £15,000, for someone buying a property worth £500,000 or more.

WHO IS AFFECTED?

The change in the tax-free limit applies to anyone who buys a property in England or Northern Ireland, including those buying a second home or landlords who own multiple properties.

An additional 3% surcharge was introduced in 2016 for anyone buying a second or additional home – this surcharge will remain, but these buyers will still benefit from the new reduced rate (see table).

First-time buyers already benefited from first-time buyer relief, where they paid no stamp duty on the first £300,000 of their home purchase, so long as the property they were buying was worth less than £500,000.

However, the change in the rules means that they will pay no stamp duty up to £500,000 and that those buying a property worth more than £500,000 will be eligible for the tax break – where they weren’t under the first-time buyer relief.

REGIONAL DIFFERENCES

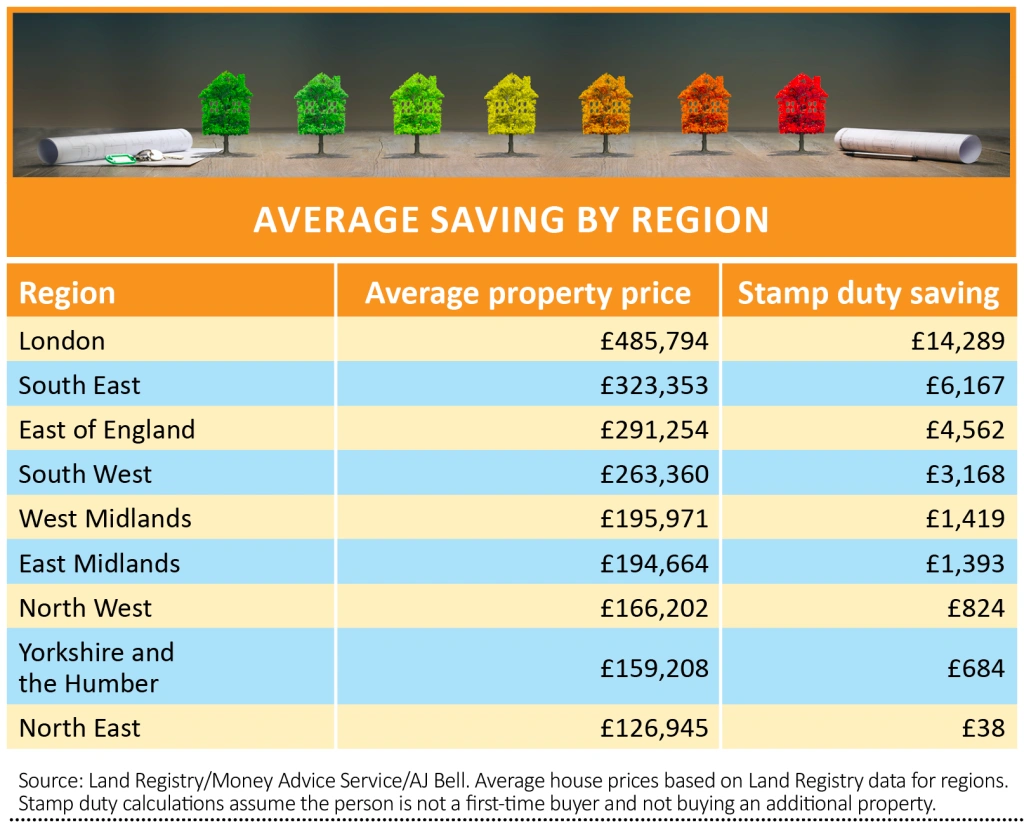

Those in areas where property is worth more will undoubtedly enjoy a greater benefit. The average house price in the north east is £126,945, according to the latest Land Registry house price data, meaning it is only a shade above the current £125,000 tax-free limit. The average buyer in this region will save just £38 under the new stamp duty system – the cost of a new toaster for their new house.

Compare that to the average house price of just under £485,800 in London, which means from today the average buyer will save £14,289 in stamp duty – the cost of new Ford Fiesta car.

Those in the south east will save an average of £6,167 under the new system, compared to just £684 saved by the average homebuyer in Yorkshire and the Humber.

First-time buyers fare worse and only those buying in London and the south east will see any additional savings on top of the existing first-time buyers’ relief, on average.

Only London and the south east have average house prices above the £300,000 mark (the existing relief). In the south east on the average house price a first-time buyer will now save £1,167 in stamp duty, while in London at the average price they will save £9,289.

WHY MAKE THE CHANGES?

The Government is hoping the tax cut will encourage more people to move home, and to get the housing market moving again. While some estate agents and online estate agent portals have reported a pick up in interest, there are worries that this is a short-term blip or that it won’t transfer into an actual boom in sales.

In his Summer Statement speech, Sunak himself referred to the fact that property transactions fell by 50% in May and that house prices had fallen for the first time in eight years.

If people don’t move home, not only does an entire industry face lower revenues and potential job losses but the Government generates less in tax. While the stamp duty cut is expected to cost almost £4 billion, the Government will be hoping that its tax cut will help to encourage more people to move home and so generate tax revenue in stamp duty.

GLOOMY OUTLOOK

Unfortunately, the outlook for the property market doesn’t look too rosy. The Bank of England’s mortgage approval figures, which are a good indication of the pipeline of new home purchases, have fallen dramatically and are a third lower than their worst point in the financial crisis – showing just how dire the outlook is for the market for the rest of this year.

Getting a mortgage is a big hurdle at the moment for homebuyers who want to make use of the Government’s tax break, as many mortgage companies have tightened their lending criteria or increased the amount of deposit you need in order to be approved.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Market share gains to fuel Motorpoint

- Analyst upgrades Luceco forecasts for the second time in as many months

- Play the healthcare boom via ‘best in class’ UDG

- QinetiQ growth strategy progressing despite challenges

- Buy care home investor Target Healthcare for a 6% yield

- Hipgnosis is cashed up and ready to buy more songs

- Ocado has a monumental growth opportunity

Investment Trusts

Money Matters

News

- US earnings season unlikely to add clarity to full year outlook

- Red hot Tesla could put huge stock offering on the table

- Fevertree shares fall on margin concerns

- Global company debt could jump by $1 trillion in 2020

- Halma’s record profit streak set to end

- B&M shares hit new record high as analysts upgrade forecasts