Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe great misconception about investment trust revenue reserves

Revenue reserves are often touted as a major advantage of owning investment trusts over traditional funds (also called open-ended funds). However, there can be some misunderstanding over how this feature works, which we will now explain.

Investment trusts (also called closed-ended funds) are allowed put aside up to 15% of their income to support dividend payments during harder times, which is called the revenue reserve. This is one of the factors why many investment trusts have a long track record of rewarding shareholders with consistent dividend growth.

Today’s Covid-19 scorched economic landscape is just the time when this unique feature of investment trusts should come into its own.

After all, income investors have been battered and bruised this year as the forecast dividend payout for the FTSE 100 has shrunk by a third to £62 billion, lowering the forecast yield to 3.6% from 4.7%.

The knock-on effect to open-ended investment funds has been evident too, leaving income investors with large holes in their portfolios, in turn reducing investment income by an average of 27%.

RESERVES AREN’T RING-FENCED

Investment trusts are required to pay out at least 85% of their income in order to retain their tax status (or 90% for real estate investment trusts), while open-ended funds must pay out all the investment income they receive.

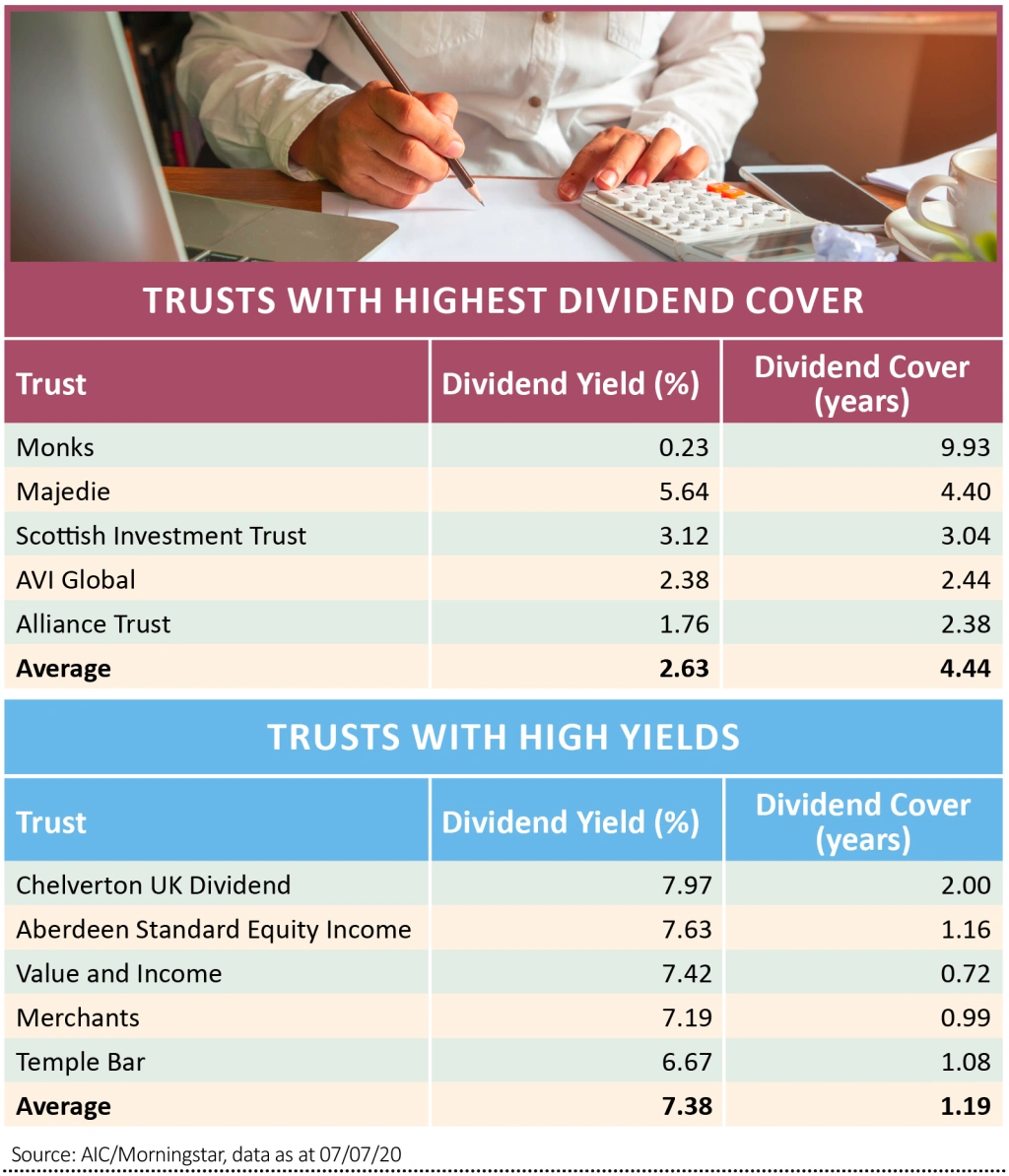

The effect of retaining 15% of earned but undistributed income over many years has resulted in many investment trusts boasting enough reserves to cover many years of future dividends. For example, the Monks Investment Trust (MNKS) managed by Baillie Gifford has enough reserves to pay out almost 10 years of dividends, although it is worth pointing out its tiny yield of 0.2%.

It is important for investors to be aware that revenue reserves are effectively bookkeeping entries and are in no way ring-fenced in separate legal structures or held in protected cash accounts as some may believe.

HOW DOES IT WORK?

The undistributed cash is invested in the trust’s assets and therefore the reserves benefit from the growth of the assets.

A spokesperson for the Association of Investment Companies says: ‘If the revenue reserves are invested in assets and they increase in value, the gain adds to the revenue reserves.’

In order to release revenue reserves, investment trust managers need to sell down assets in order to raise cash and pay dividends to shareholders. Depending on the liquidity of the trust’s portfolio, turning capital into income is relatively straightforward.

One other thing to bear in mind is that the decision to make up any income shortfalls by dipping into undistributed income sits entirely with the board of directors. Just because they exist doesn’t mean they will be paid out.

The board needs to consider the interests of shareholders looking for income with those focused on long-term capital growth. Paying out today reduces future growth potential.

CHANGING THE RULES

In 2012 the tax rules were changed which allowed investment trusts to pay dividends from the accumulated profits built up, providing a potentially much bigger capital pool from which to distribute future income and plug any holes caused by falling dividends.

One investment trust that distributes dividends from capital is the International Biotechnology Trust (IBT) managed by SV Health Managers, which pays out the equivalent of 4% of net asset value.

Investors wouldn’t normally buy a biotech trust for income, but the board reasoned that it would help reduce the shares’ discount to net asset value, in addition to buying back shares. Over the last years the shares have traded at an average discount of 2.5%.

WATCH OUT FOR HIGH YIELD TRAPS

While paying dividends from capital is more secure than relying on investment income, it would be dangerous to lump all trusts together and assume the ones with the highest dividend yields are the best.

Focusing on the UK Income and Global Income sectors, the tables show trusts with the highest dividend cover, expressed in number of years and compares them with the highest yielding trusts.

The cover calculation takes the revenue reserves as reported in the latest set of accounts and compares it with the current dividend to see how many years it could be paid purely from those reserves.

The highest yielding trusts have very poor cover with the Value and Income Trust (VIN) and Merchants Trust (MRCH) having less than a year’s cover. A top 10 holding for Merchants includes Royal Dutch Shell (RDSB) which was one of the UK market’s highest yielding stocks until recently when it slashed its dividend by two thirds.

In contrast, Majedie Investments (MAJE) is yielding more than the market average and has more than four years of dividend cover.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Market share gains to fuel Motorpoint

- Analyst upgrades Luceco forecasts for the second time in as many months

- Play the healthcare boom via ‘best in class’ UDG

- QinetiQ growth strategy progressing despite challenges

- Buy care home investor Target Healthcare for a 6% yield

- Hipgnosis is cashed up and ready to buy more songs

- Ocado has a monumental growth opportunity

Investment Trusts

Money Matters

News

- US earnings season unlikely to add clarity to full year outlook

- Red hot Tesla could put huge stock offering on the table

- Fevertree shares fall on margin concerns

- Global company debt could jump by $1 trillion in 2020

- Halma’s record profit streak set to end

- B&M shares hit new record high as analysts upgrade forecasts