Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineExploring small cap stocks on single-digit multiples

With markets and financial commentators seemingly obsessed with the notion of big companies getting bigger – Apple being a prime example, having doubled in value to a record-breaking $2 trillion just in the last two years – investors shouldn’t overlook the long-term attraction of smaller companies.

It’s well established that small companies tend to grow faster than big companies. Partly this is down to the law of big numbers – it’s much harder for firms with sales of £1 billion or £10 billion to increase their sales and earnings by 10% or more a year than it is for firms that turn over £100 million a year, for example.

However, another part of the equation is that successful small companies tend to be niche players, exploiting leading positions in narrow yet profitable fields.

RISKS AND REWARDS

As their markets are typically fragmented ones – that is, with one or two leading players and a ‘long tail’ of smaller competitors – these firms often grow by acquisition as well as organically.

As well as consolidating their position as the ‘go-to’ provider of goods and services, they can become the buyer of choice for companies where management are looking for a bigger partner or owners are looking to step down.

Yet investing in small companies doesn’t come without risk. Typically small firms need to keep raising capital to grow and many can spend years building out their business before they generate any profits.

Evidence from the US suggests that during the pandemic, large companies were able to borrow money relatively easily while many smaller companies struggled to secure funding as banks tightened their lending requirements.

Smaller companies are by their nature less liquid investments, meaning the shares can be difficult to buy or sell and they tend to be more volatile. Also, while they can offer higher growth, there are no guarantees.

SEARCHING FOR IDEAS

When looking for small-cap ideas, they should be cheap enough to compensate you for the risk of owning them and should have fairly solid finances, ideally with little or no net debt.

With this in mind we screened the UK market on SharePad using two easy-to-understand metrics – the forward price-to-earnings (PE) ratio for the next 12 months and the forecast net debt-to-earnings before interest, tax, depreciation and amortisation (EBITDA) for the next 12 months. This made it easier to see if there were any interesting, financially solid smaller cap companies which had been overlooked by mainstream investors.

We excluded investment trusts and companies forecast to make net or EBITDA losses over the next 12 months, leaving us with a list of over 700 stocks of all different sizes.

HOT OR NOT

Unsurprisingly, with the pandemic having impacted consumer behaviour particularly hard, few travel, leisure or hospitality stocks passed muster.

Small biotech stocks – of which there are several dozen listed in London – were also thin on the ground as they tend to run losses.

At first glance, many of the cheapest stocks in the market on forecast PE multiples appear to come from the construction, industrial goods and services, metals and mining, or real estate sectors, which stands to reason as these aren’t exactly ‘glamour’ businesses in hot demand among investors.

Many financial stocks looked cheap on a PE basis but failed to score on net debt-to-EBITDA as debt is accounted for differently within financial companies.

Conversely, the most expensive stocks – many trading on three-figure forward PE multiples – tended to be in the ‘hot’ sectors of healthcare and technology, with the exception of a handful of consumer-facing businesses where earnings have been severely depressed but not quite wiped out by the pandemic.

When we added the screen looking at forecast net debt-to-EBITDA, a fair few of the industrial and real estate stocks fell through the net as their gearing was much too high for our liking.

We were left with around 35 stocks which were cheap – trading on a forward PE multiple of less than 10 times – and had fairly solid balance sheets – net debt-to-EBITDA of less than 1, or preferably net cash, assuming the analysts are correct.

CHEAP FOR A REASON

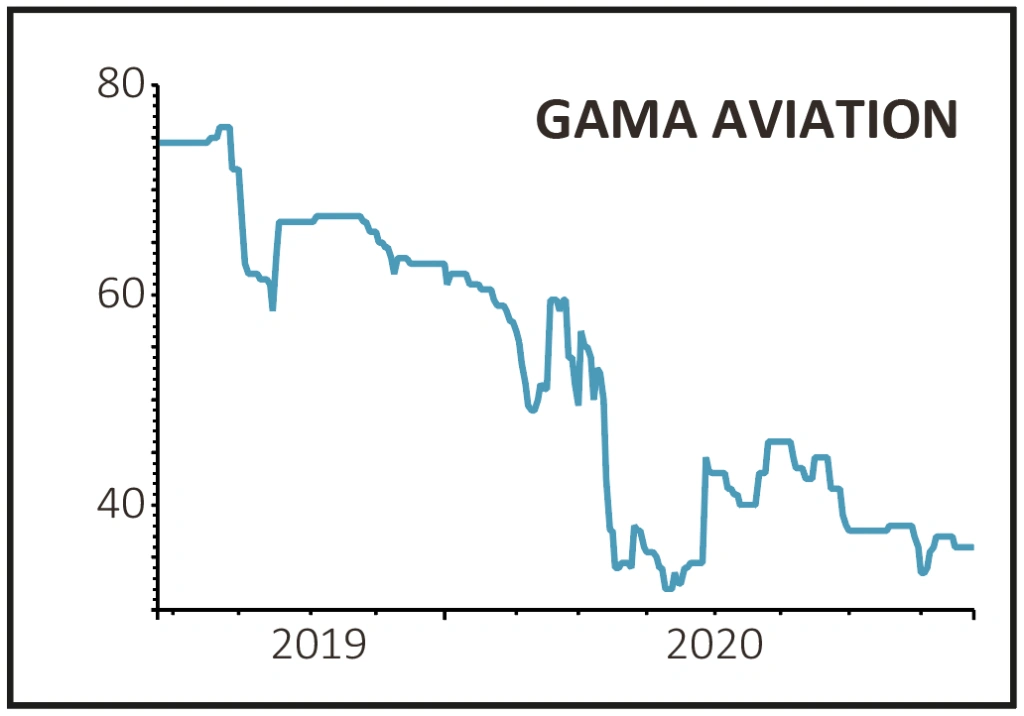

In many cases, the stocks are clearly cheap for a reason. For example, Gama Aviation’s (GMAA:AIM) profit outlook for the next 12 months is about as depressed as it could be, explaining why the shares trade on less than four times prospective earnings.

While private business jets may have been replaced for now by Teams and Zoom meetings, most of the firm’s service contracts are with central and local government and the armed forces, and are long-term in nature, which suggests it should make it through the pandemic in one piece. It is also forecast to have a small net cash position in 12 months’ time.

However, the shares have a very unappealing 25% bid/offer spread, highlighting the illiquid nature of the shares.

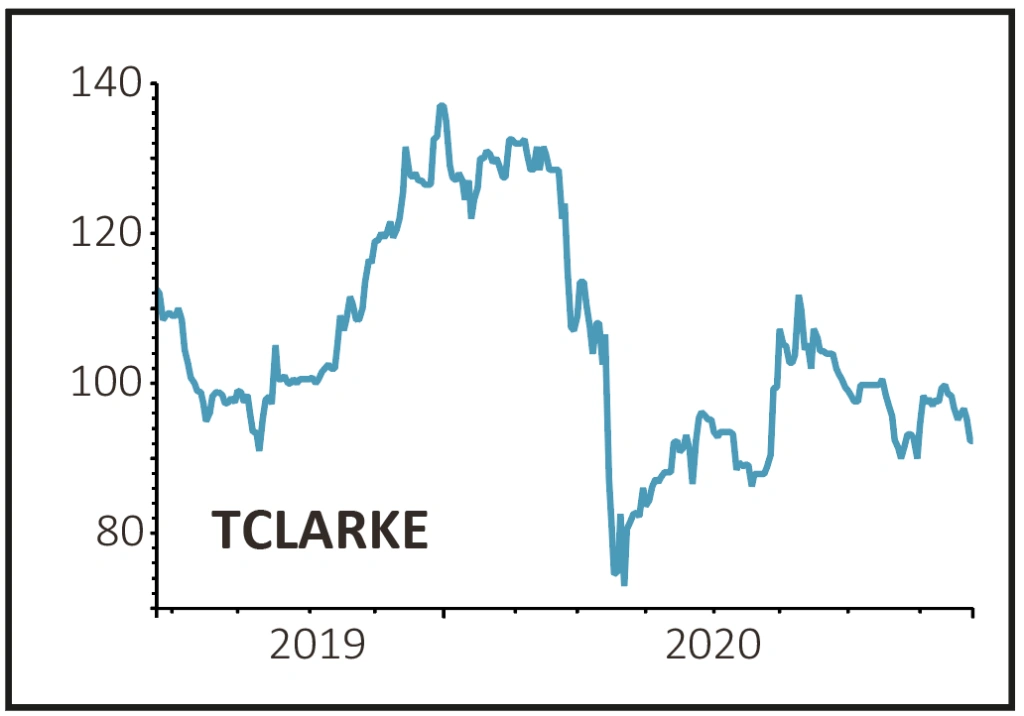

A near-9% bid/offer spread also dilutes the appeal of investing in T Clarke (CTO), which is a shame as there is a lot to like about the business. It builds data centres and infrastructure projects, and played a frontline role in the pandemic fitting out the 200-bed Nightingale Hospital in Exeter in just six weeks.

It generated earnings and positive net cash during the first-half while increasing its order book to over £400 million and bidding on a further £600 million of projects.

Costs have been trimmed and banking facilities have been renewed with no debt due before 2024.

As well as building data centres, where T Clarke is currently involved in three projects and could tender for a further dozen in the second-half, the firm offers an ESG-friendly ‘smart building solution’ which controls heating, lighting, air quality and security and which can be retrofitted into existing building as well as installed in new builds.

THE STOCK TO BUY

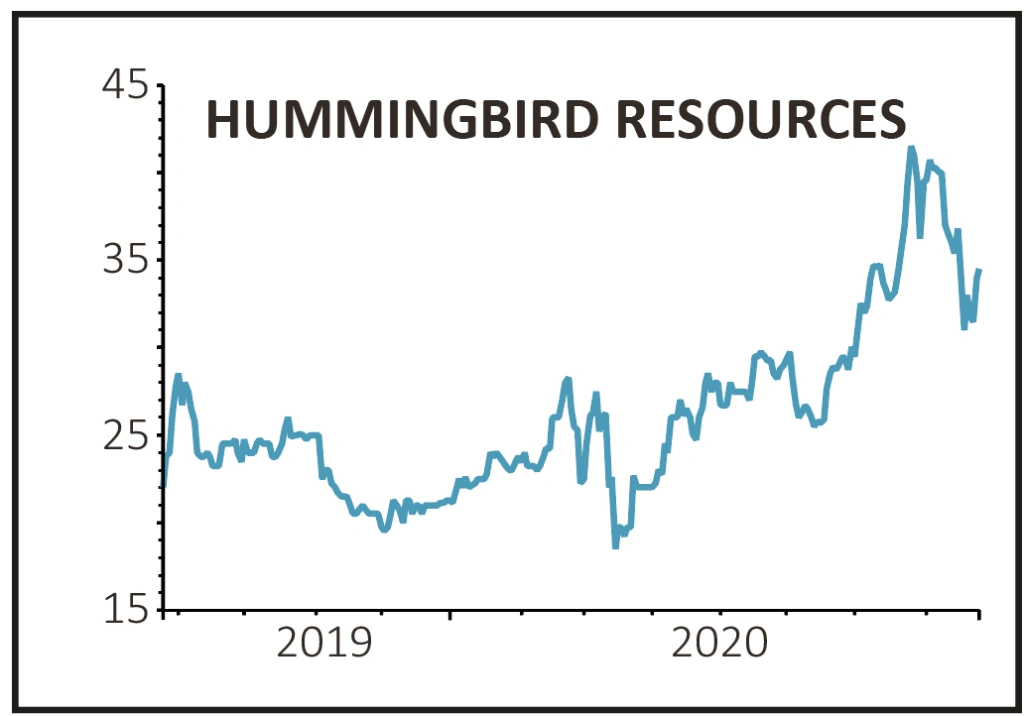

Hummingbird Resources (HUM:AIM)

Like most gold miners, Hummingbird has had a good 2020 as reflected in its share price, yet it still trades on less than five times forecast earnings.

Last week it revealed it had paid down a chunk of its debt and reiterated its commitment to having no borrowings by July 2021, consistent with the consensus forecast on SharePad.

The firm’s all-in sustaining cost of production is $995 per ounce while gold is trading at nearly twice that level.

A key risk to the share price is that one of its mines is in Mali, where there has recently been unrest, but for gold investors political risk is not that unusual.

Quite a few analysts are excited by the company including Canaccord Genuity’s Sam Catalano who likes the look of the Kouroussa gold project in Guinea that Hummingbird has just bought.

‘We believe the acquisition and development of the Kouroussa project can be entirely funded through internal cash flow,’ said Catalano, commenting before the deal completed on 1 September.

‘Successful completion of the proposed Kouroussa acquisition should provide meaningful value accretion for existing holders (20p-30p/share) as well as broadening Hummingbird’s appeal to a larger range of investors through operating life extension, doubling of output to more than 200,000 ounces per year, and becoming a multi- asset producer.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Money Matters

News

- Saga white knight welcomed by investors

- SDL’s tie-up with RWS offers a compelling story

- Shock resignation of Japan PM hits Nikkei

- US markets flash warning signs with echoes of past corrections

- US Federal Reserve tweaks monetary policy goals

- Beauty website owner prepares for biggest London listing of 2020