Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineNice and simple portfolio: Seven ETFs are all you need

Investing doesn’t need to be hard, complicated or even require a lot of time, and you certainly don’t need dozens of all different kinds of investments in your portfolio.

In fact, seven funds could be enough. And they needn’t be active funds either.

Picking the right fund and fund manager is always a tricky task, particularly trying to find ones that have proven they can outperform the wider stock market over the long term, and to such an extent that you don’t feel the impact of the fees they charge.

So here we’ve created a portfolio of seven exchange-traded funds (ETFs), which give you exposure to major asset classes across the world, but with a slight bias to the more familiar territory of the UK.

WHO WOULD THIS SUIT?

This portfolio is a good option for a wide range of people:

– Those who are starting out with investing and want a cost-efficient way to access the markets

– Those who want to invest but are too busy or simply don’t want the hassle of managing their investments on a regular basis

– Those who are just disillusioned with the value, or lack of it, generated by active fund managers and therefore want to go down the passive route

The portfolio is designed to behave fairly conservatively and provides exposure to a wide range of quoted stocks and bonds globally.

In the good times when markets are rising, the portfolio’s returns may not reach the same height as some active funds, but in the bad times when markets fall in theory the losses shouldn’t be as severe as many active funds.

Particularly for a novice investor who’s just getting started with the markets, a conservative portfolio could be a good option. Behavioural science has shown that, psychologically, losses hurt than more gains. In fact, research shows that people tend to feel the pain of a decline twice as hard as the joy experienced when things are on the rise.

With that in mind, this portfolio of seven ETFs is split 70% stocks and 30% bonds.

Admittedly someone in their 20s, 30s or 40s may prefer to have a lower weighting to bonds, as they have time on their side to ride the ups and downs of the stock market and stocks have historically produced better returns than bonds.

However, we think a 70:30 split has merit in the current market environment. Bonds tend to outperform stocks when a recession is on the horizon, while stocks tend to rally when an economic expansion is on the cards. It’s really hard to time the market so by holding stocks and bonds in this proportion you don’t need to be prescient.

It’s easy to change the weightings to more equities if you’re happy to stomach extra risks.

BUILDING THE PORTFOLIO

We’ve got 15% of the portfolio in the FTSE 100, giving exposure to all the well-known blue-chips listed on the London market; and 10% is in the FTSE 250, which is more orientated to mid-caps and provides greater exposure to the domestic economy than the exporter-heavy FTSE 100.

We’ve got 5% in large and relatively safe gilts (UK government bonds) and 20% is in sterling-denominated bonds issued by companies, called corporate bonds.

That leaves 50% for overseas financial markets, with the biggest share going into developed market stocks (40% of the portfolio) and 5% in emerging market stocks, with another 5% allocated for emerging market bonds.

Taking into account the major market sell-off this year as a result of the coronavirus pandemic, in the past five years this portfolio has delivered a total return of 33.1% compared to 8.4% for the FTSE All-Share index, according to calculations by FE Fundinfo.

All the ETFs in the portfolio have been chosen because they represent the cheapest and most liquid way to access the aforementioned markets, with the lowest total cost of ownership when combining the fees they charge and price difference between buying and selling the ETF, known as the bid-ask, or bid-offer, spread.

Read on to discover the seven ETFs you need for a simple, low cost portfolio.

THE STOCKS PART OF THE PORTFOLIO

iSHARES CORE FTSE 100 ETF (ISF)

Even those who are new to investing should have heard of the FTSE 100. It frequently appears on TV news bulletins and in the newspapers, with its direction up or down giving the public a steer as to how the stock market is performing.

The index, a representation of the UK’s 100 largest companies by market value, is packed full of names well-known to the public, like BT (BT.A), Barclays (BARC), Royal Dutch Shell (RDSB) and Vodafone (VOD).

For any investor, having some exposure to the UK’s blue-chips is always a good idea, and many in the investment world currently think the UK stock market represents better value for money right now than the US, where the S&P 500 and Nasdaq have reached new all-time highs despite ongoing weakness in the economy and risks of further shocks ahead.

The FTSE 100 is currently trading on a 12-month forward price-to-earnings (PE) ratio of 17.1 times, according to Stockopedia, compared to a PE of 20.5 for the S&P 500 and 18.3 for the Nasdaq Composite.

iShares Core FTSE 100 (ISF) is the most popular ETF which tracks the FTSE 100 index, and with a total cost of 0.07% a year is a very cost effective method of gaining exposure to the largest companies listed on the UK market.

VANGUARD FTSE 250 ETF (VMID)

While a lot of the country’s well-known companies are in the FTSE 100, the mid cap FTSE 250 – which comprises the next biggest 250 companies in the UK by market value – also contains a number of recognisable names.

The index provides exposure to various sectors in the UK economy, and contains names like EasyJet (EZJ), TUI (TUI), Games Workshop (GAW), Greggs (GRG), Wetherspoon (JDW), William Hill (WMH) and WH Smith (SMWH).

The fortunes of the UK economy aren’t considered great at the moment, particularly if unemployment spikes when the Government’s job retention scheme ends, while there are also headwinds on the horizon if Brexit trade talks end without a deal.

But having the FTSE 250 in your portfolio means you will also get the benefit as and when the UK economy recovers. The index could well rally if the Government’s coronavirus support schemes work as intended and the economic disruption isn’t as severe as some in the market think, while a trade agreement between the UK and EU before the end of the year would also be a positive for both the economy and the FTSE 250.

A good ETF in this area is Vanguard FTSE 250 (VMID), which has more assets under management than any other ETF tracking this index, being responsible for £1.4 billion of investors’ money – meaning it has a very tight bid-ask spread – and is also the lowest cost with an ongoing charge of just 0.1% a year.

LYXOR CORE MSCI WORLD ETF (LCWL)

Providing exposure to 1,601 companies across 23 developed market countries, the MSCI World index is as about as broad and comprehensive an investment as you can get. As such, we make it the largest component in the portfolio accounting for 40% of assets.

With over two thirds of the index made up of businesses in the US, this is the part of your portfolio where you will feel the benefit of the well-documented rising US markets and technology stocks, though also still getting the benefits from diversification with access to other developed market economies like Japan and the Eurozone.

Besides Nestlé, the top 10 constituents of the MSCI World index are all American. The top five names in the index are Apple, Microsoft, Amazon, Facebook and Google owner Alphabet, while Johnson & Johnson, Proctor & Gamble and Visa are also in the top 10.

An exceptionally low cost way to track this index is Lyxor Core MSCI WORLD (LCUW), which has a total expense ratio of 0.12% a year.

Given the sheer size of the MSCI World index, this ETF buys a carefully selected sample of the stocks in the index to mimic its risk and return profile, as well as maintain liquidity and keep transactions costs low, pushing its total cost of ownership lower than many other ETFs which also track the index.

It’s worth noting the UK only accounts for around 4% of the MSCI World index, so not really adding much UK exposure on top of the FTSE 100 and FTSE 250 components of our portfolio.

iSHARES CORE MSCI EM IMI ETF (EMIM)

Given they’re part of some of the fastest growing economies on earth, having exposure to stocks in your portfolio from emerging market (EM) countries is a good idea.

There are risks with these markets, considering they are still emerging and can frequently encounter teething problems as they develop, and so should only make up a small part of a portfolio for a beginner investor or someone who doesn’t have the time to regularly monitor their investments. In our portfolio, EM stocks only make up 5% overall.

But EM companies are definitely still worth including, and a great way to do this is through iShares Core MSCI EM IMI (EMIM), which tracks the MSCI Emerging Markets Investable Markets index and is the cheapest option to do so with an 0.18% a year ongoing charge. It’s also one of the popular ETFs tracking this space globally with responsibility for over $15 billion of investors’ money.

This market cap weighted index covers approximately 99% of available shares in 24 emerging market countries, and also includes small cap stocks, which can provide some extra risk but also offers broader and more diversified EM exposure.

More than 10% of the ETF is made up of Chinese giants Alibaba and Tencent, and another 3.3% alone is allocated to South Korean conglomerate Samsung.

This ETF is a great way to play the China growth story, while also getting the benefit of diversification to other markets and the potential growth in countries like South Korea, India and Taiwan.

THE BONDS PART OF THE PORTFOLIO

iSHARES CORE UK GILTS ETF (IGLT)

UK government bonds, known as gilts, should always be part of any portfolio if an investor is in any way risk-averse.

Government bonds, especially those issued by developed market governments like the UK, are seen as a safe haven in times of uncertainty, something which could be particularly useful right now given the ongoing economic fallout from the pandemic.

Gilts can provide capital preservation in times of market stress. However, gilts become less attractive when there is an increase in inflation expectations or an actual rise in inflation.

Gilt yields are currently near record lows with demand for safe haven assets surging in recent months. Under such circumstances, we think it is prudent to only have a small allocation, at 5% of the portfolio.

The best way to invest in gilts is through an ETF. The world of active fund management has practically given up on trying to add value through gilts, given that interest rates are as low as they are right now and don’t look like going up anytime soon. Investing in gilts directly is possible, but this process can be complex and time-consuming.

A great ETF for gilts is iShares Core UK Gilts (IGLT), which is one of the cheapest with a cost of 0.07% a year, is very liquid with £1.6 billion in assets and has generally exhibited a low level of volatility.

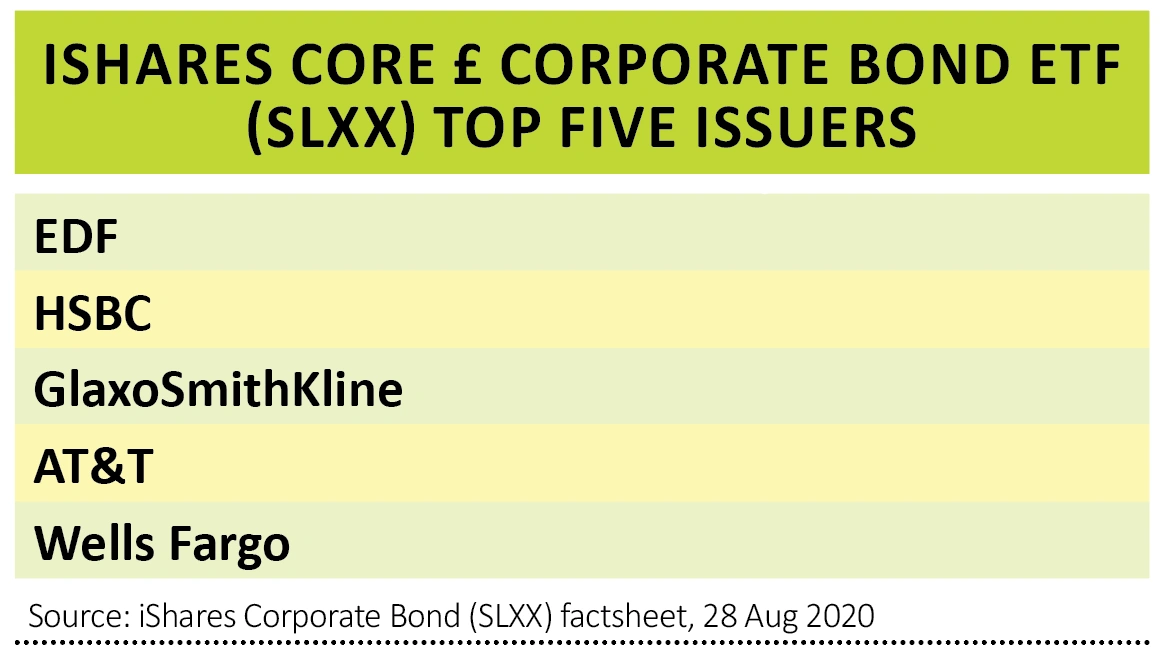

iSHARES CORE £ CORPORATE BOND ETF (SLXX)

Slightly racier than gilts but often still a safer bet than company shares are corporate bonds. For our portfolio we’ve chosen bonds issued in sterling by big, high-quality companies with strong balance sheets.

Making up a fifth of our portfolio overall, corporate bonds offer a better return than UK government bonds, and are higher risk to go with the higher return. However, the risk is still relatively low compared to equities when getting exposure only to bonds issued by companies with an investment grade rating.

One of the best ways to add corporate bonds to your portfolio is through iShares Core £ Corporate Bond (SLXX), the lowest cost option at 0.2% a year to track the Markit iBoxx GBP Liquid Corporate Large Cap index. This only includes bonds from companies with a high quality credit rating and which have a sufficiently large issuance size.

The ETF itself doesn’t hold all the bond issuances in the index, but carefully selects a sample to mimic the index’s risk profile while avoiding illiquidity issues, something which can plague the bond market generally.

iSHARES JPMORGAN EM LOCAL GOVERNMENT BOND ETF (SEML)

Racier still than corporate bonds are emerging market bonds, which while having a safer profile than emerging market stocks also contain more risk than developed market bonds, and so only make up 5% of our portfolio.

But emerging market debt can also provide better returns than gilts and UK corporate bonds, particularly if it’s in the local currency of the issuing country, and are worth including in a portfolio.

Most emerging market government debt is issued in US dollars, but analysts believe yields on local currency emerging market debt could be a bright spot in the global bond market going forward, given the downward pressure on the dollar.

While it is the most expensive ETF in the portfolio, an efficient way to play the local currency emerging market debt theme is through iShares JP Morgan EM Local Government Bond ETF (SEML). Although it costs 0.5% a year, it is still one of the lowest ways to get access to this emerging asset class and is the most liquid ETF available to UK investors.

Disclaimer: Editor Daniel Coatsworth owns shares in Vanguard FTSE 250 ETF and iShares Core MSCI EM IMI ETF referenced in this article

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Money Matters

News

- Saga white knight welcomed by investors

- SDL’s tie-up with RWS offers a compelling story

- Shock resignation of Japan PM hits Nikkei

- US markets flash warning signs with echoes of past corrections

- US Federal Reserve tweaks monetary policy goals

- Beauty website owner prepares for biggest London listing of 2020