Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDiscover the funds offering a 30% instant boost and tax-free dividends

The new venture capital trust (VCT) offer season is now in full swing where investors can apply for new shares and enjoy immediate tax benefits.

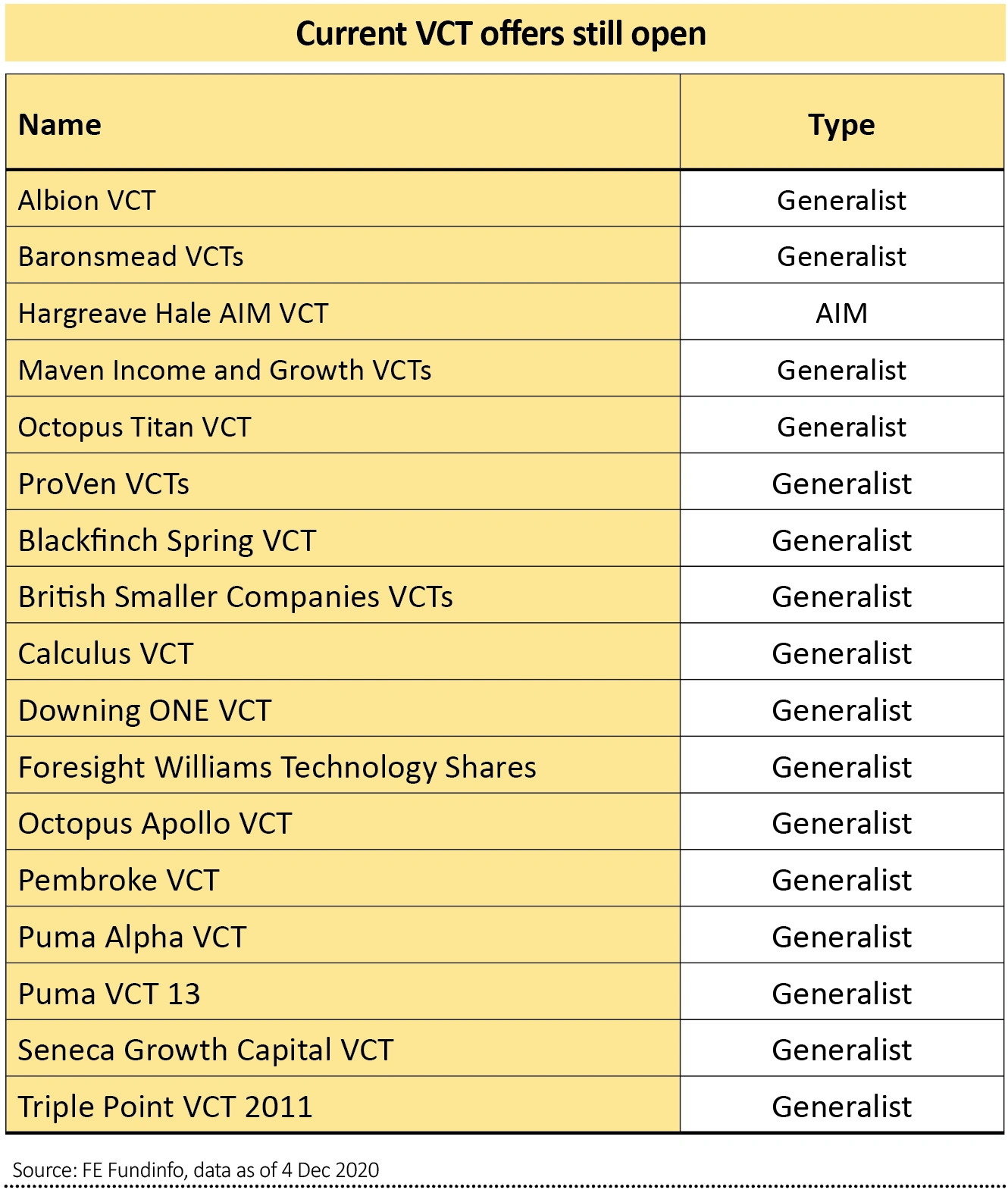

Recent offers from Amati AIM VCT and Octopus AIM VCT have already closed, having hit their subscription target. Others are filling up quickly.

Each year VCTs seem to attract money faster than the previous year, meaning interested investors need to act fast once offers go live – although it is important to understand all the risks involved before making an investment decisions.

This article will explain all the essential points about what VCTs are, why you might consider investing in them, how to purchase, and the important things to note if you want to lower the risk of losing money.

STEP ONE: UNDERSTANDING VCTS

VCTs are close-ended funds which invest in early stage companies. You can’t get your money back for five years, but to compensate for that factor and the risk of investing in young businesses, you can claim up to 30% income tax relief on an investment of up to £200,000 a year. You will also have a capital gains exemption on disposal.

If you do want your money back before the five years are up, you must pay back the tax relief.

By investing in VCTs, the idea is that you are helping Britain’s exciting, entrepreneurial businesses to grow. There is also the bonus of tax-free dividends.

One of the main objectives for VCT managers is to provide shareholders with consistent and if possible progressive dividend payments, something which is often funded by the money made from exiting companies. But VCTs will usually look to hold companies for at least five years and can sometimes hold them for more than 15 years.

STEP TWO: WHO WOULD VCTS SUIT?

Individuals on higher-rate or additional rate tax bands are naturally drawn to VCTs because of their tax benefits.

They can also be of interest to someone who wants to invest in early stage growth companies or individuals who have maxed out allowances on various wrappers such as ISAs and hit or exceeded the £1,073,100 pension lifetime allowance.

But contrary to popular opinion you don’t need to be a high net worth individual to invest in VCTs, with the average investment size in VCTs being around £12,000 and the minimum subscription for many of them being £5,000.

These funds are also popular among those looking to supplement their income as VCTs pay dividends, which are tax free and it is common to achieve a yield of around 5%.

Octopus Investments managing director Paul Latham says a typical VCT investor is someone in their 40s to 70s and can often be people who are investing with a view to supplementing their pensions. They also need to be taxpayers.

Latham explains: ‘It tends to be the mass affluent, often people in their 50s or 60s – their pensions are maxed out so they’re looking to do something a bit different. It’s often a reason to be thinking about VCTs, hopefully getting a good tax-free dividend stream.’

STEP THREE: WHO ISN’T SUITABLE FOR A VCT?

Clearly if you want your money before five years, VCTs are not for you.

Also, those who don’t see investing in the stock market as an option shouldn’t consider VCTs, as they can invest in firms at an even riskier stage in their life, with a stock market float often being the exit stage.

STEP FOUR: UNDERSTAND THAT NOT THE HOLDINGS IN A VCT WILL SUCCEED

Many businesses in VCTs end up failing but there are a number of success stories, some of them quite spectacular, and it’s these winners which ultimately drive positive returns for VCTs.

Latham explains: ‘VCTs invest in smaller companies, and they are deemed by the Financial Conduct Authority as a high-risk investment. We would say overall that the returns do outweigh the losses, but you need to be comfortable with that level of uncertainty.’

Malcolm Ferguson, investment manager at Octopus Ventures, concedes that a majority of exits tend to be failures, but points out that this outweighed overall by the success stories.

Giving an insight into how the exits work, he says: ‘Exits tend to be in three categories: mistakes – we don’t sell them, we write them off; quite good – these tend to be in the £50 million to £100 million range, and we usually sell those to private equity funds or trade buyers; and excellent, the companies with revenue of £100 million plus, we float them on a stock market or sell them to a huge corporation, companies like Twitter, Microsoft, Nestle, Unilever (ULVR), etc.’

STEP FIVE: CHARGES CAN BE HIGH

Another point worth considering is the charges. Initial charges for VCTs are typically in the region of 4%, on top of an approximate 2% annual management charge and possibly other fees for administration costs, running costs and performance fees.

It’s worth pointing out though that these costs arguably reflect the complexity of the space and the need to make sure investments qualify for the relevant tax relief.

STEP SIX: HOW TO BUY A VCT

You should buy VCTs direct from the fund manager or a specialist VCT broker during the offer periods to get all the tax benefits.

You can buy VCTs on the open market (also known as the secondary market) but you would lose the 30% income tax relief.

STEP SEVEN: WHAT DO THEY INVEST IN?

Most of the companies in VCT funds are start-ups, and the rules mean managers have to invest at least 80% of their portfolios in qualifying companies.

These are firms that promote innovation and industrial change but are not generating enough cash flow to get loans or other traditional sources of finance, and need a lot of capital, usually between £100,000 and £2 million.

Among these firms there are some well-known names that have come through the VCT route, including Zoopla, Secret Escape, Graze.com, while there are also VCTs that invest in AIM stocks and these funds have backed companies that have gone on to become successful such as Abcam (ABC:AIM) and Tristel (TSTL:AIM).

STEP EIGHT: VCTS CAN HAVE DIFFERENT STRATEGIES

Another thing to consider is that managers can take different approaches to what they choose to invest in. Andrew Wolfson, who runs the Pembroke VCT (PEMB), prefers to back either consumer facing businesses or firms that supply tech that enables companies to reach consumers.

He says: ‘We look for companies that are disrupting their sector and have that product uniqueness with their offering. But we don’t like businesses where the consumer needs education. Put it this

way, I don’t back businesses that I don’t understand – so I don’t back medtech, fintech, proptech, etc.’

Pembroke’s top holdings include Popsa, an app which makes photobooks from the photos on your phone or tablet, organic juice firm Plenish and womenswear brand ME+EM.

Other managers can take a different approach. Chris Hutchinson, manager of the Unicorn AIM VCT (UAV), takes pride in the fund’s relative lack of exposure to consumer-facing companies, with some of its top holdings including Abcam and Tristel, as well as others like biotech firm MaxCyte (MXCT:AIM), software business Tracsis (TRCS:AIM) and brake disc manufacturer Surface Transforms (SCE:AIM).

Hutchinson says: ‘We do a lot of work getting to know the management teams as closely as we can. We don’t claim to be experts in areas like life sciences, but my team has bucket loads of experience and I think we’re really good at telling which management teams are genuine long-term builders of value and which are just short-term “get rich quick” merchants.

‘We often ask management blunt or what they might view as “stupid” questions, but those questions are carefully designed to get a sense of what motivates them.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Alibaba faces baptism of fire at start of 2021

- IP Group still offers upside as it eyes further realisations

- Play a regional recovery with BlackRock Latin American

- Buy Sainsbury's now before the shares surge

- Gamma run could speed up if it can nick a bit of Twilio’s limelight

- Recent acquisition provides growth and security for Gresham House