Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe income and renewable funds going cheap

Investment trusts differ from other types of fund as they can trade at a discount or premium to the value of their underlying assets. This can present interesting opportunities, particularly when trusts are trading at larger than usual discounts to net asset value (NAV).

To offer insights into some of the trends in this area Shares is going to start regularly tracking movements in trust share prices relative to their NAV using data from Winterflood.

In each article we will shine a spotlight on one part of the investment trust universe and discuss the dynamics around how its constituents trade relative to their assets.

The NAV in these tables is calculated with any debt held by the trusts at book value, which is how much it will cost to repay the lender when the loan is due, rather than fair value, which is how much the debt is worth now.

We have ignored Real Estate Investment Trusts and more complex products which invest in areas like hedge funds and structured finance. Our focus is on trusts which are trading at larger discounts or premiums to NAV than their 12-month average.

It is worth noting this 12-month average currently encompasses a period of significant volatility when the premium or discount to NAV will have swung wildly at times due to the coronavirus market sell-off in early 2020.

TRUSTS AT LARGER THAN AVERAGE DISCOUNTS

It is not surprising to see several income-related trusts trading at larger than average discounts given the impact the pandemic had on dividends.

At 12.7%, UK-focused BlackRock Income & Growth (BRIG) trades at a significantly larger discount to NAV than its 3.5% 12-month average.

Investment trust researcher Kepler comments: ‘The Covid-19 pandemic and the lockdowns that followed have clearly proven a substantial challenge to dividend generation globally, as a vast swathe of companies found their operations either impeded or forced to stop entirely.

‘Secondary impacts to resources demand (energy) and interest rates (banks and insurers) further affected many significant contributors to UK dividends.’

Kepler notes the board has ‘substantial’ revenue reserves and has previously displayed its willingness to deploy them to sustain dividend payments.

The increased discount at Premier Miton Global Renewables (PMGR) of 11.7% (versus 6.7% one-year average) might seem counter-intuitive given the last 12 months has seen growing interest in investments linked to ESG (environmental, social, governance) themes.

However, the company attracted some investor dissent having switched its focus from a broader infrastructure remit in 2020.

Another trust which experienced changes last year was Brunner (BUT) which saw the departure of well-regarded lead manager Lucy Macdonald who had successfully narrowed the discount on the trust during her tenure.

TRUSTS AT LARGER THAN AVERAGE PREMIUMS

In terms of trusts trading at larger than average premiums

to NAV, there are several which tap into popular themes.

The build in an already hefty premium from 17.2% to 45.1% at life science focused trust Syncona (SYNC) reflects the prominence of healthcare amid the Covid-19 pandemic. In the words of Numis: ‘We believe that Syncona has an exceptional management team that have built a strong track record and are one of the leading investors in the cell and gene therapy space.’

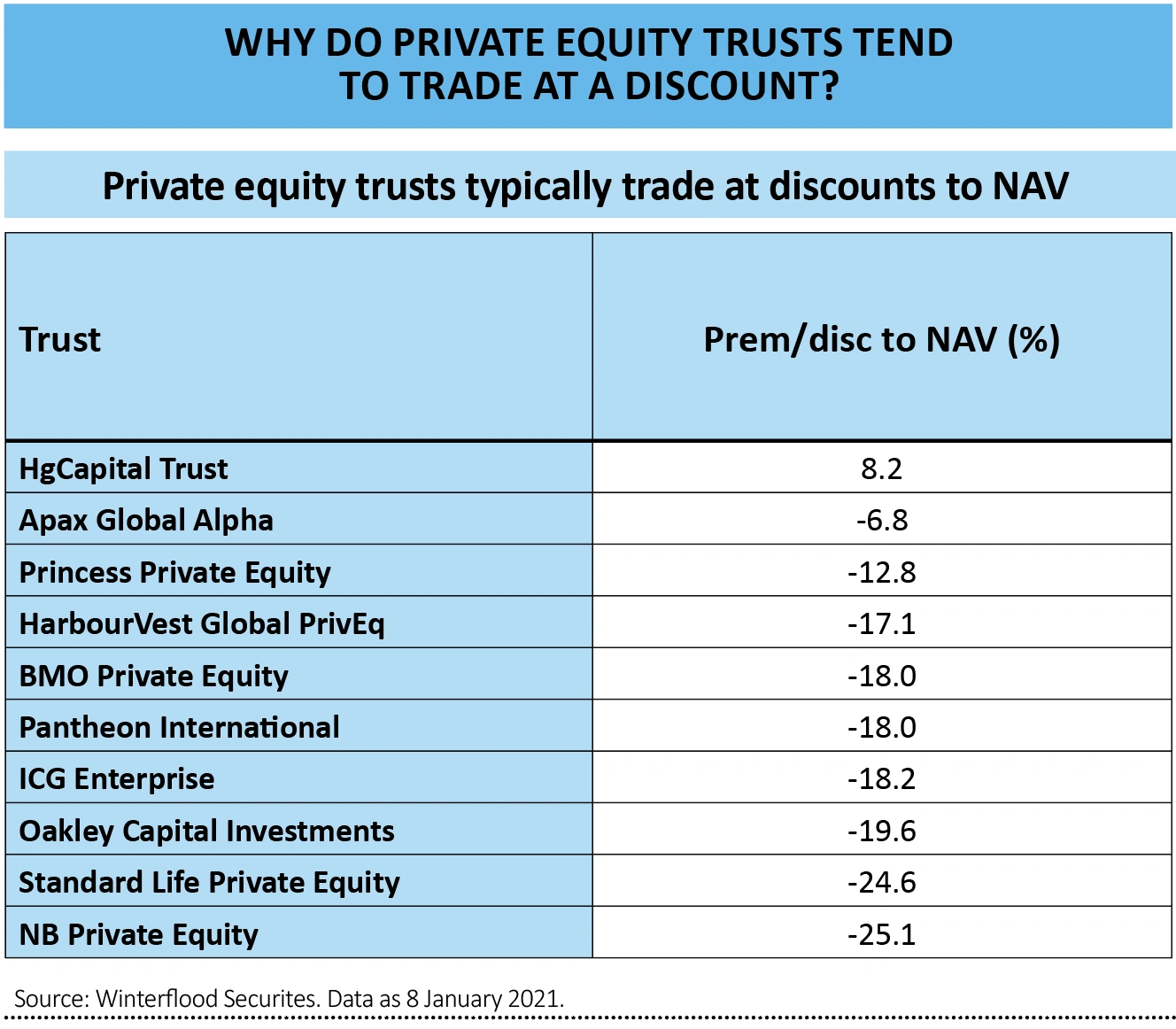

Why do private equity trusts tend to trade at a discount?

Most private equity trusts trade at a discount to net asset value. This reflects their exposure to unlisted assets which do not have a daily market value.

As a result, they offer more limited transparency to investors and they also have

less liquid underlying assets – or in other words they are harder to buy or sell. Trusts in this space include those making direct private equity investments and those investing in several different private equity portfolios managed by third parties.

Hg Capital (HGT) is notable in that it currently trades at a premium, unlike most of its peers. This likely reflects the make-up of the portfolio

which as broker Numis observes: ‘Includes high quality, resilient and high growth companies providing non-discretionary software and services, typically with highly predictable business models and high levels of robust, recurring revenue.’

Coronavirus has seen an increasing number of activities shift online – so it is no surprise to see increased appetite for Augmentum Fintech (AUGM) in that context, with the portfolio made up of financial technology start-ups across Europe. It has gone from an average 7.2% discount to NAV to trade at a 14.6% premium.

The election of Joe Biden to the US presidency is seen as good news for green industries across the Atlantic – with US Solar Fund (USF) benefiting handsomely.

The strong performance of Japanese equities – with the flagship Nikkei 225 recently marking record highs – has also helped Japanese-focused trusts attain decent premiums. While the more rapid recovery from the pandemic in China, relative to the West, helped lift Baillie Gifford China Growth (BGCG) to a substantially higher premium of 9.8% versus a 12-month average of 0.3%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

First-time Investor

Great Ideas

- Alibaba faces baptism of fire at start of 2021

- IP Group still offers upside as it eyes further realisations

- Play a regional recovery with BlackRock Latin American

- Buy Sainsbury's now before the shares surge

- Gamma run could speed up if it can nick a bit of Twilio’s limelight

- Recent acquisition provides growth and security for Gresham House