Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine10 great stocks: Our best ideas for the year ahead

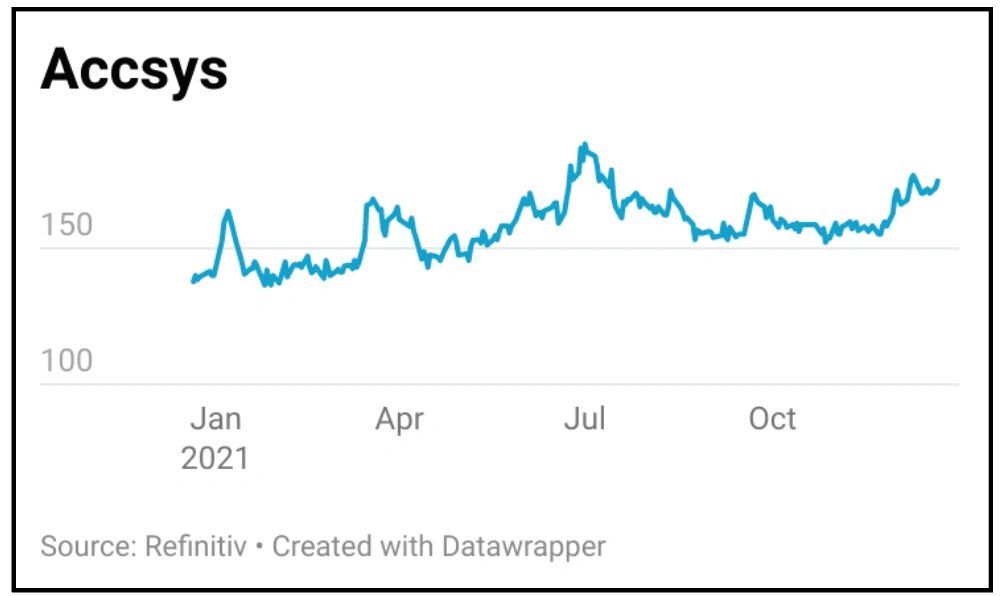

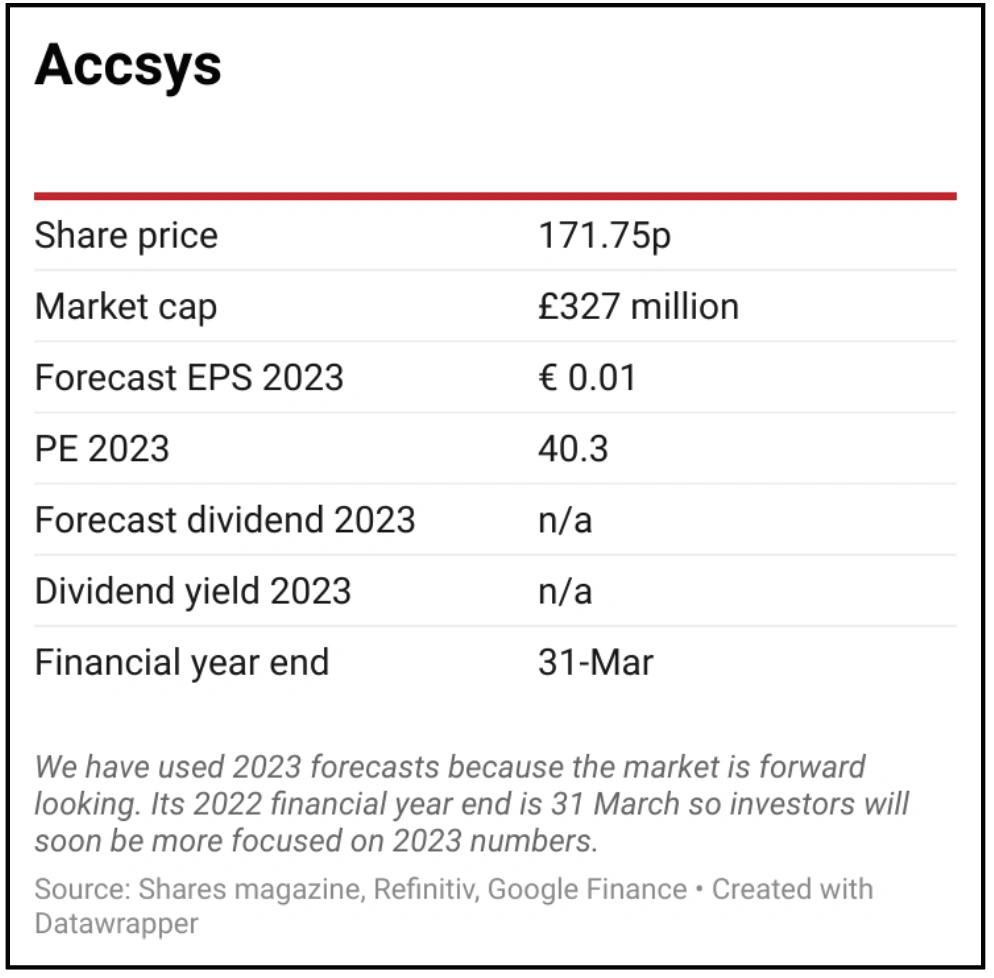

Accsys Technologies

Accsys (AXS:AIM) is a global leader in sustainable wood technology and sells its products into the construction and building materials industries in the UK, Europe, North America and Asia through timber distributors.

Its Accoya wood product is both sustainable and high-performing, with a 50-year guarantee, which makes it an ideal replacement for man-made, carbon-polluting alternatives like aluminium and plastic, which are also difficult to recycle.

Given the firm sold just over 60,000 square metres of Accoya in the year to March 2021, and the addressable global market is over 2.6 million square metres per year, there is significant room for Accsys to expand.

Meanwhile, the potential market for panels made from Tricoya, which is chipped Accoya used to make MDF (medium density fibreboard), is over 1.6 million cubic metres, which is still only 1% of the global MDF market.

Demand is being driven by increasing regulation and the need for firms manufacturing building products, such as doors and windows, to be able to offer more sustainable products.

The company is expanding production of Accoya at its Arnhem plant as quickly as possible to keep up with demand, while its first Tricoya plant in Hull is expected to begin manufacturing next July.

Within five years, Accsys expects its combined output of Accoya and Tricoya to be more than five times last year’s total, and even then it still has an enormous runway for growth.

Producing Tricoya chips in a dedicated plant will not only dramatically improve capacity but it will free up more Accoya wood for sale, which together with increased output at Arnhem will allow the company to meet the demands of larger-scale manufacturers who need to ensure supplies.

The firm has a joint venture agreement in the US with Eastman Chemical for the production of Accoya in North America, which will significantly increase turnover.

As sales ramp up, earnings are set to jump significantly which will naturally bring Accsys’ price to earnings multiple down to a more realistic level, with analysts at Edison forecasting a 2024 financial year rating of around 25 times net earnings and just over eight times operating earnings.

Given the firm is likely to need to invest all its surplus capital to grow the business, we wouldn’t expect it to pay dividends for some time.

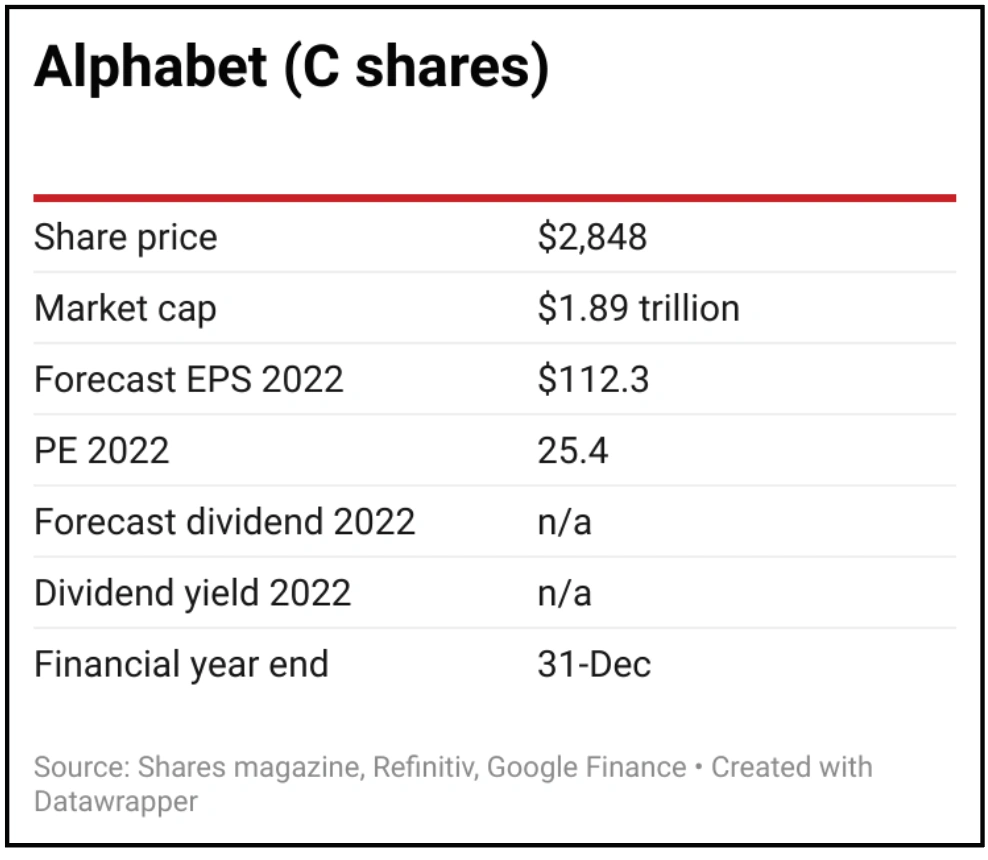

Alphabet

Google-owner Alphabet (GOOG) is a giant in internet advertising. It is growing fast with large technological moats and very attractive operating profit margins of 30%.

In five years, it has doubled revenues and is forecast to have generated nearly 40% sales growth alone in 2021.

Digital advertising will account for 61.5% of global advertising spend for the first time in 2022, according to the latest advertising expenditure forecast compiled by Zenith, and more than 65% by 2024.

Brands are desperate to reach widening audiences on social media platforms, online video, connected TV and e-commerce channels, an established trend that the pandemic super-charged.

Beyond the internet search services for which Alphabet is best known; and YouTube, one of the world’s most visited platforms; the group has continued to acquire and develop new areas, such as a fast-growing cloud computing business, self-driving vehicle venture Waymo and health researcher Verily.

You don’t grow to the size of a small nation’s GDP without locking horns with regulators, and Alphabet does face antitrust challenges ahead.

The company has been accused of hurting competitors by giving priority in its search results to its own products, while its complex ecosystem also makes it difficult for alternative operatorsto succeed.

Furthermore, the tech giant owns the world’s dominant smartphone operating system, Android, which runs close on nine out of every 10 smartphones worldwide.

If push came to shove and the worst happened Alphabet could possibly restructure itself under regulatory pressure, but it would likely fight tooth and nail and a legal battle could drag on for years.

Most analysts don’t see that happening, instead believing some form of deal would be struck that would suit all parties to some degree, albeit with possible financial penalties.

Alphabet’s shares are not expensive given its qualities, trading on 25.4 times forecast earnings for 2022. It has some of the best tech brains on the planet in its talented workforce and the financial resources to back emerging developments and opportunities, with a $128 billion net cash position.

The shares have rewarded investors for years, with total returns of nearly 18.5% a year over 10 years, surpassing both the performance of the S&P 500 and Nasdaq Composite indices during a decade-long bull run.

The only real drawback is that a single share costs several thousand dollars which might deter some investors with limited funds.

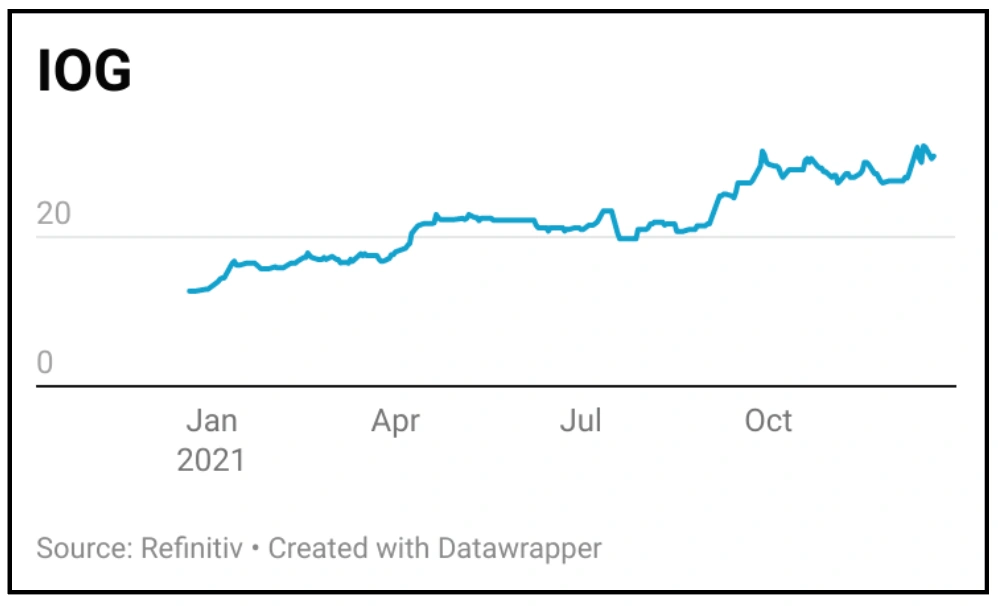

IOG

Shares expects 2022 to be a breakthrough year for North Sea gas play IOG (IOG:AIM). Production should commence imminently of natural gas from its Saturn Banks project in the Southern North Sea.

This production is coming on stream at a time of exceptionally high gas prices and, despite a strong run for the shares in 2021, they do not yet fully reflect the company’s near-term potential.

Based on forecasts from FinnCap, IOG should be in line to generate free cash flow of £71.8 million in 2022, or a little under half the current market valuation of the firm.

The cash generated will be used to progress the phase one development of Saturn Banks which includes the Blythe and Elgood fields, due on stream imminently, and the Southwark field where the company is in the process of carrying out development drilling. The second phase will involve the Goddard, Nailsworth and Elland fields.

IOG has 50% ownership and is operator of these assets which combined encompass 76 million barrels of oil equivalent of proved and probable reserves and contingent resources.

Significantly it owns and has recommissioned the infrastructure required to produce this gas, including the Saturn Banks pipeline and Saturn Banks reception facilities, which are part of the Bacton gas terminal on the Norfolk coast.

The medium to long-term strategy for IOG is likely to involve adding new developments which can use its existing infrastructure.

Once development drilling has completed on the Southwark field, with first output expected by the middle of 2022, the same rig will be used to drill the Goddard and Kelham North/Central appraisal wells which could act as a further catalyst for the shares.

Significantly, IOG is expected to have one of the lowest carbon emissions profiles in the industry; the company has estimated lifetime Scope 1 and 2 average emission intensity at 3.97 kg CO2e/boe (kilogrammes of carbon dioxide per barrel of oil equivalent) for phase one of Saturn Banks, compared to the North Sea average of 20.2 kg CO2e/boe.

One risk for investors to weigh is a €100 million bond due to mature in September 2024. This has a coupon of the Euro Interbank Offered Rate plus 9.5%, paid quarterly. However, the company has flagged an opportunity to refinance this debt at the end of the year, which would reduce borrowing costs.

Jet2

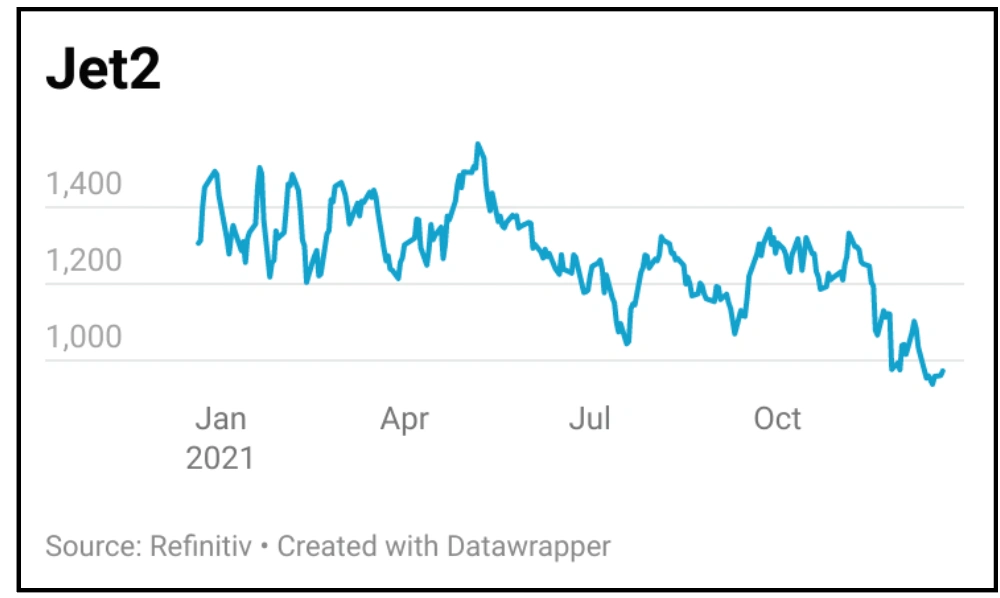

In the face of a growing threat of widespread lockdowns it might seem counter-intuitive to invest in a travel and holidays operator. But we believe that as 2022 progresses, Jet2 (JET2:AIM) will come roaring back on a tide of Omicron recovery. Analysts at broker Jefferies have named it their top recovery pick.

Jet2 is already one of the UK’s top airlines by the number of passengers flown, while the package holidays it offers have stood the test of time with Brits wanting a relatively inexpensive couple of weeks in the sun where everything is done for them – flights, hotel, transfers, car rental, day trips etc.

In its last full year before Covid (to 31 March 2020) it flew nearly 15 million passengers and took nearly 4 million people on holiday. It runs a flexible tour operator model that allows it to rejig its airline operations to serve the routes with the highest level of demand.

This is a strategy it’s pursued exceptionally well in the past. With overall positive brand perception, it puts Jet2 in a great position to pick up market share as the travel industry bounces back as expected through the coming months.

Current seat capacity for summer 2022 is approximately 13% higher than summer 2019 thanks to fleet agreements that secure future capacity growth. Bookings for summer 2022 remain encouraging and load factors – the percentage of available seating capacity that has been filled with passengers – are ahead of summer 2019 at the same point.

Jet2 is also financially sound. Whereas holiday rival TUI (TUI) has needed bailing out multiple times over the years by the German government in a bid to secure jobs, Jet2 had approximately £1.5 billion of cash on its books at the last count (to end September 2021), having already raised money from investors. That excludes any deposits made by holidaymakers booking early.

Admittedly, Jet2 reported a disappointing £200 million loss for the six months to the end of September and could come under pressure if unemployment spikes. But the stock is already trading at its lowest in more than a year and the company has the balance sheet strength to absorb losses in the short-term without capping its investment for the long-term, allowing it to capitalise on industry recovery when it does take shape.

London Stock Exchange

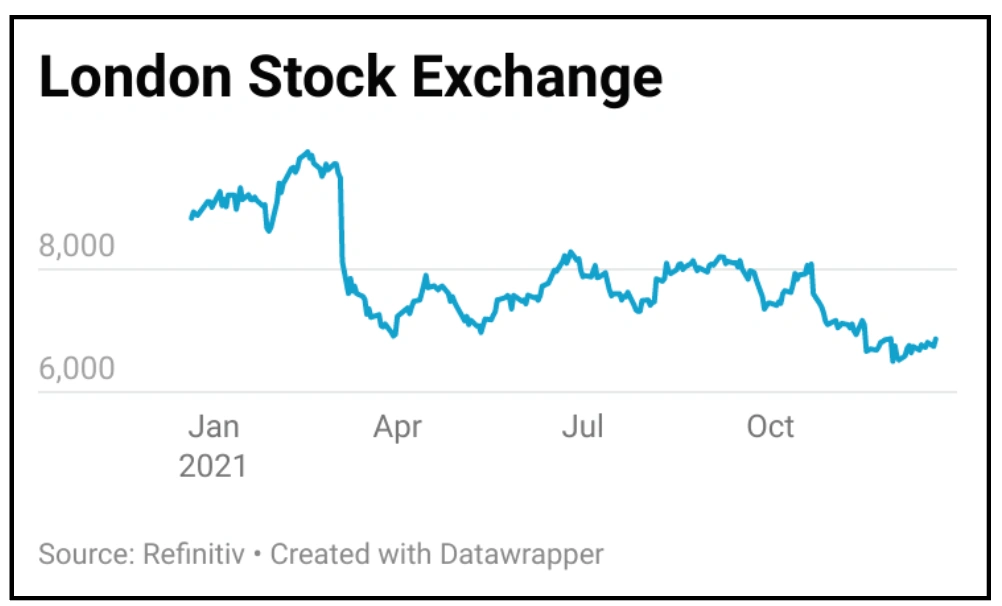

This trade requires taking a contrarian view. Market sentiment is weak towards the stock, yet the valuation has become attractive for what is fundamentally a decent business.

Shares in London Stock Exchange (LSEG) have fallen by a third in value since February on concerns surrounding integration costs associated with the group’s $27 billion acquisition of data provider Refinitiv. However, owning Refinitiv gives London Stock Exchange a new lease of life.

It transitions the group towards higher margin subscription data and analytics revenue, as well as reducing its dependence on volatile stock exchange related business.

It secures the group’s position in the critical growth markets of Asia and America, and it creates the opportunity for the shares to re-rate as a data company.

It also enhances the group’s geographical scale and scope, specifically in the key markets of Asia and America.

The combination of Refinitiv’s foreign exchange and fixed income venues with London Stock Exchange’s equities, ETF and derivatives businesses will undoubtedly foster innovation and new product offerings.

The combined group’s data offering will benefit from the increased adoption of algorithmic and quantitative trading, coupled with the heightened demand for passive and multi-class asset investments.

It currently trades on 20 times forecast earnings per share for 2023, which compares with European and US exchange peers that are also trading on 20-times and information peers on 32-times.

Alex Crooke, fund manager of Janus Henderson’s Bankers Investment Trust (BNKR), believes that ‘while short term costs and higher investment needs have impacted the shares this year, it has created an opportunity to own a high-quality business with large recurring revenues on an attractive valuation.’

The attempt by HKEX (Hong Kong Exchanges and Clearing) in September 2019 to acquire London Stock Exchange for $39 billion reflects the unique nature of the target’s market infrastructure and data assets.

In essence London Stock Exchange is a trophy asset, benefiting from incumbency, high barriers to entry and a dominant local market position.

There are risks in buying a stock when its shares continue to fall as it needs a catalyst to stop the decline. Full year results on 3 March could be the catalyst to win back the market’s favour.

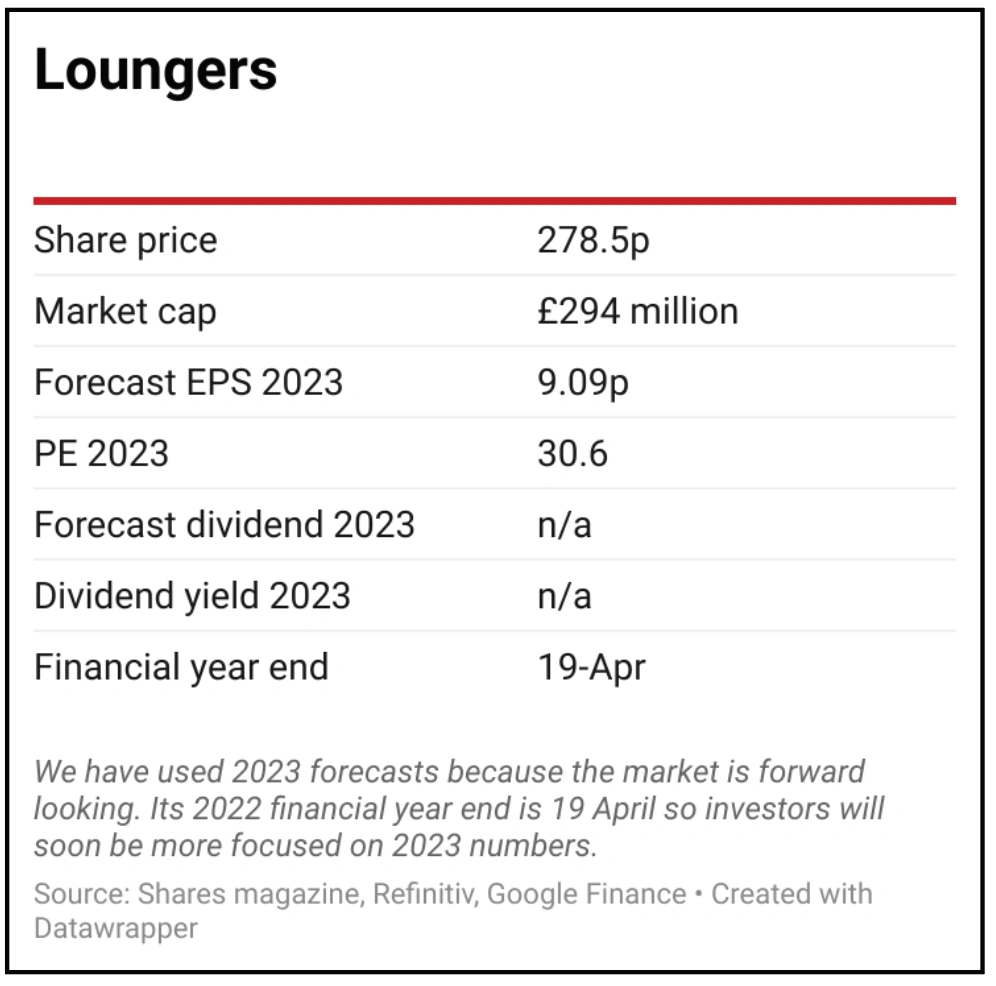

Loungers

Loungers (LGRS:AIM) is in a sweet spot as an investment, offering both revenue growth and increasing margins as it benefits from scale efficiencies.

The ability to trade throughout the day appeals to a broad demographic with around 90% of customers visiting for more than one occasion, demonstrating the attraction of the format.

Arguably the offering is even more relevant in a post-pandemic world and lends itself to hybrid working patterns and community-based socialising while the suburban and high street locations also play into the company’s hands.

The damage caused to hospitality has created a favourable market tailwind for Loungers to exploit and it has plans to accelerate the rollout of sites to 25 a year with flexibility to do more as circumstances permit. The company recently said its pipeline of new sites had never looked so strong.

Management has identified the potential to grow to around 500 sites across the UK over the medium term from the current 184, implying an almost three-fold increase in the size of the group and providing a good growth profile for investors.

Analysts at investment bank Berenberg believe the company is being conservative and there is potential for 1,000 sites over time. Loungers is very profitable and mature sites earn over 30% returns on the capital invested.

The company has reached a tipping point where cash generated from its existing business can fund the opening of new sites while the increasing scale brings efficiencies and provide the potential for expanding operating margins.

Loungers operates two brands. A ‘Lounge’ is equal part restaurant, pub and coffee shop and can be found across the UK in small towns and communities. Each has its own individual name which connects to the history of the town. There are 153 of these sites nationwide.

A ‘Cosy Club’ is a more formal restaurant located in larger towns providing table service and reservations. It has 31 Cosy Club sites.

There are always risks and headwinds to consider when investing in the hospitality sector and another lockdown would impact the business – current disruption to the sector could hurt earnings temporarily so investors need to be patient – but we believe the ship is in strong hands and able to weather future storms.

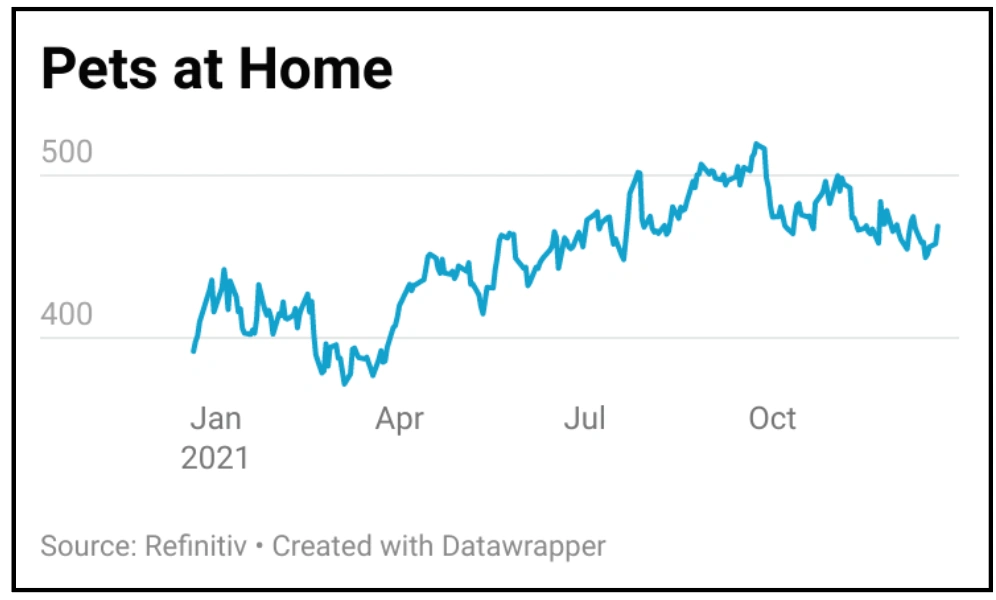

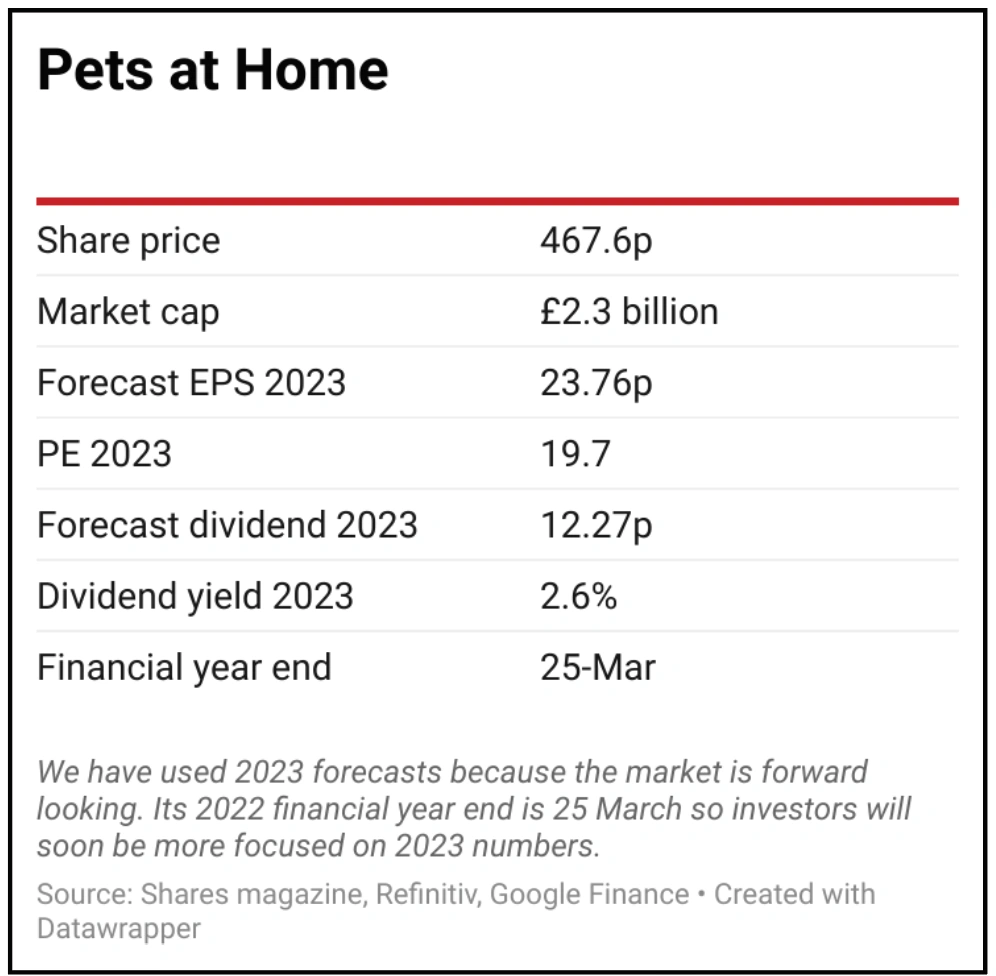

Pets at Home

Pets at Home (PETS) is in an excellent position to take advantage of the opportunities created by an expanded pet population.

It’s one of those stocks easily dismissed by some investors given that the share price has already been a strong performer. We view it as a great business with plenty of room to continue growing earnings and where the valuation is still reasonable.

Unlike some other activities which gained popularity during lockdown, taking in a new pet is a long-term commitment for most people, not a fad.

There are three main ways Pets at Home will benefit from this market opportunity. First through people buying food, treats, bedding and toys for their animals; second as people look to keep their furry friends tidy at its in-store grooming salons; and third by offering veterinary services.

The veterinary business, under the Vets4Pets banner, is high margin and includes directly owned practices, both inside Pets at Home stores and in standalone locations, as well as those operated through a recently launched partnership model.

By agreeing joint ventures with vets, Pets at Home can grow this part of the group rapidly without incurring significant costs.

The firm’s VIP, Puppy and Kitten Club memberships are a smart way of securing customer loyalty. Effectively you gain access to things like in-store discounts and advice, a network of other members who you can call on if your pet goes missing and a donation to an animal charity every time you shop.

These initiatives should help Pets at Home to protect and grow market share, which stood at 23% in the most recent financial year according to the company, by warding off non-specialist rivals like the supermarkets, which are probably the clearest competitive threat.

The company has done a decent job of mitigating supply chain issues, helped by the fact its product range is sourced in the UK and is not perishableor seasonal.

The man behind Pets at Home’s successful strategy, Peter Pritchard, is set to leave in summer 2022. He hands over a business in great shape.

The company is forecast to report £135 million pre-tax profit for the year to March 2022, rising to £152 million in 2023 and £168 million in 2024, according to analyst consensus estimatespublished by Refinitiv.

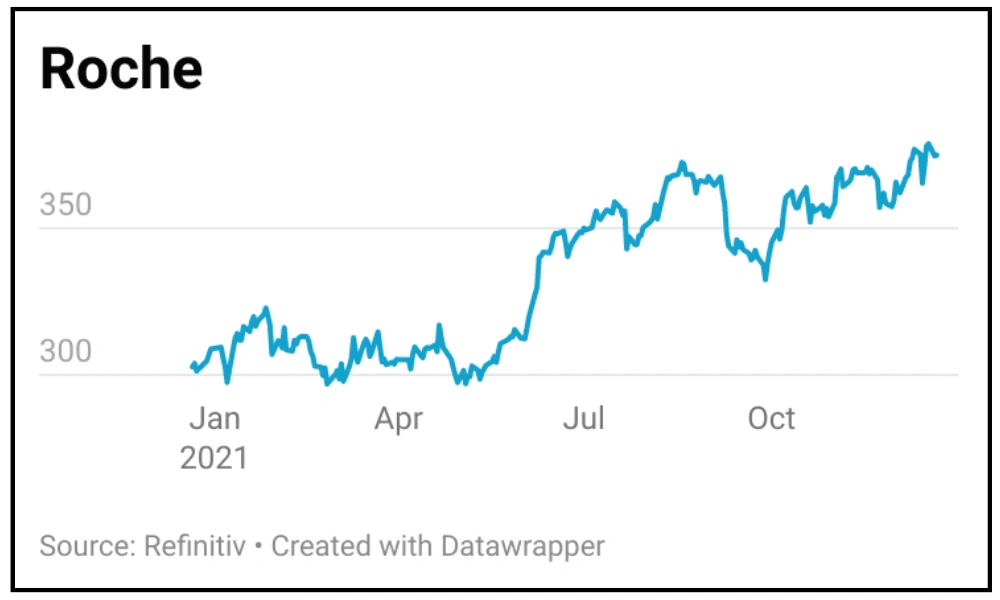

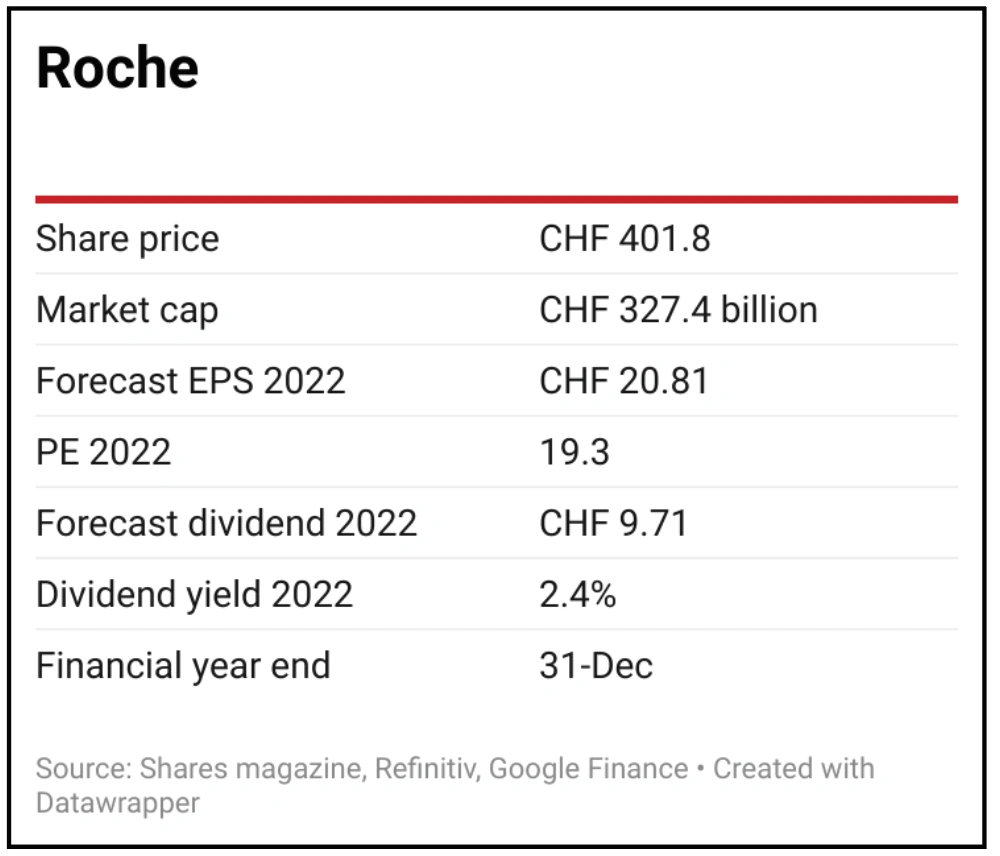

Roche

Pharmaceutical giant Roche is class act with an attractive investment case. It has sector leading margins and returns on capital as well as clear growth catalysts.

Roche has reached a turning point in the lifecycle of its drug pipeline where the growth in sales of new drugs is more than compensating for the loss of sales when patent protection expires, which leads rivals to sell copycat drugs more cheaply.

In October Roche increased full year guidance for revenues and profit to grow by a mid-single digit percentage, up from low single digit.

The company recently used its strong balance sheet to purchase Novartis’ 53.3 million shares in Roche for $20.7 billion with the intention of cancelling the shares. This will reduce the share count by around 5% and correspondingly increasing earnings per share.

In addition, Roche’s diagnostics division is seeing a tailwind from Covid-19 with increased PCR testing although this is a lower margin business.

Roche recently released detailed data of its Polivy drug in patients with previously untreated B-cell Lymphoma, a cancer of the lymphatic system, which means it could be on track for an additional approval in a potentially lucrative market forthe company.

Management believes approval of the drug for newly diagnosed patients could unlock a market worth $2 billion. Polivy generated sales of $178 million in the first nine months of 2021.

Roche’s Alzheimer’s drug Gantenerumab recently received FDA breakthrough therapy designation and stage three trial data is on track to be released in the second half of 2022.

The company’s eye disease drug Faricimab is expected to be approved in the first quarter of 2022 while its lung cancer drug Tiragolumab is expected in the final quarter.

It is worth noting that investing in pharmaceutical companies bears the risk of share price underperformance should drugs fail to gain regulatory approval.

Roche is composed of a pharmaceutical division which generates around 71% of total revenues and a diagnostics division. The latter owns the global marketing rights for the PCR (polymerase chain reaction) test, considered to be the gold standard for detecting genetic material.

Investment Berenberg says: ‘Roche is successfully navigating a period of heavy erosion of its legacy drugs, with strong growth from its newer assets. We think there is scope for increased growth in the dividend once the legacy erosion has passed.’ The stock yields 2.4%.

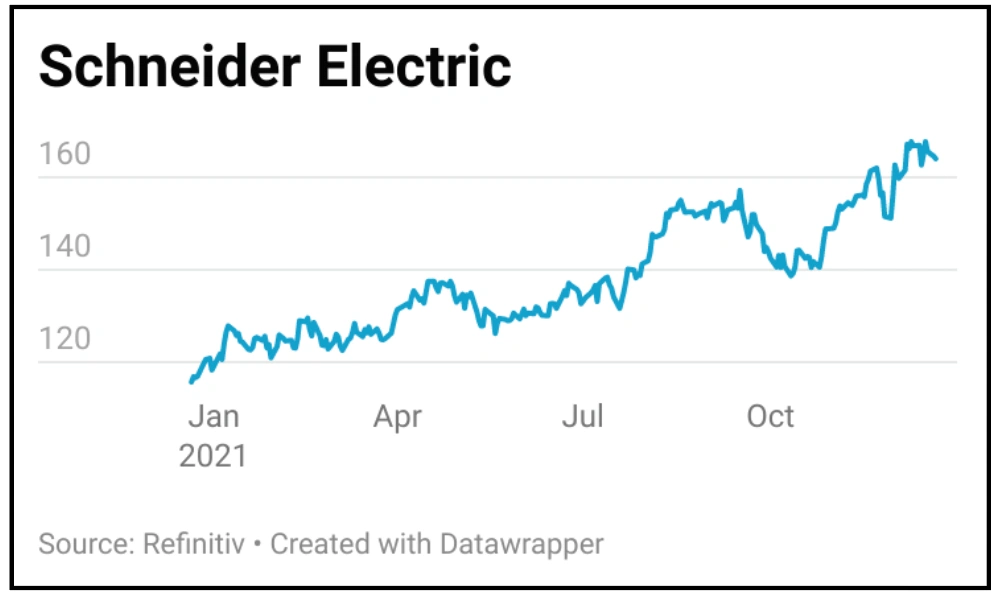

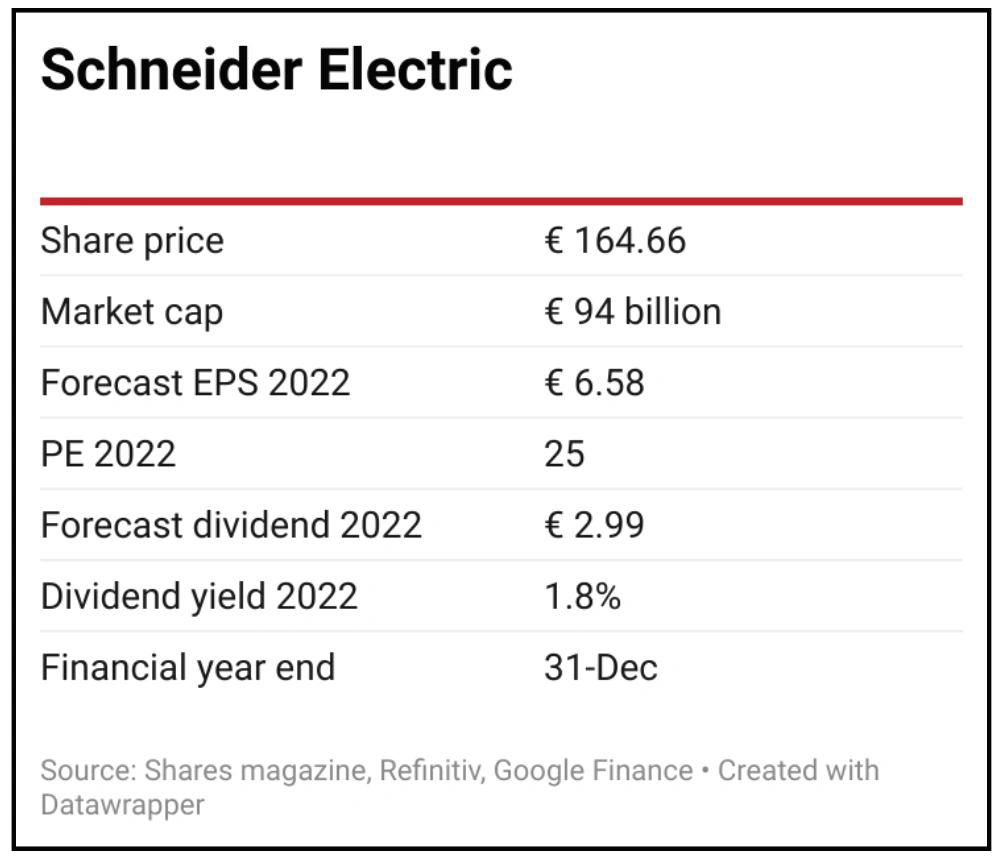

Schneider Electric

In the drive to digitalise the economy and in the process reduce energy consumption, Paris-listed electrical systems and automation and control firm Schneider Electric is a world leader.

Its products range from simple residential kit like light switches, sockets and electric vehicle charging points, all the way up to building control systems and industrial automation software.

It employs 135,000 people in 115 countries across the globe and last year it turned over more than €25 billion or £21.5 billion in revenues, split roughly one third in the US, one third in Asia and the balance in Europe and the rest of the world.

Over 90% of its sales are on the energy demand side, serving the residential, industrial, infrastructure and technology sectors, with less than 10% in its legacy business of high-voltage electricity transmission and distribution.

Through its Internet of Things platform, the firm aims to help its customers save 800 million tons of CO2 emissions and provide green electricity to 50 million people by 2025.

Around 70% of its revenues derive from sustainable solutions, which also account for 73% of its investments, with a focus on data centers, storage and other distributed energy resources and smart solutions that advance electrification, energy efficiency and renewability.

For decades the firm has innovated in power distribution, working with software firms to tailor its products to its customers’ needs.

Two of its latest initiatives are bi-directional or ‘future’ electricity grids and a framework for environmentally sustainable data centres, which are notorious for consuming vast amounts of energy.

Future grids are designed to help reduce emissions by allowing multiple sources of decentralised, locally generated renewable energy to contribute to the electricity network safely, reliably and efficiently while reducing energy loss through transmission and distribution.

Meanwhile, data centres – which create up to 2% of the world’s carbon emissions, the same as the airline industry – need to become much more sustainable while at the same time offering greater capacity, so Schneider has set up a framework for companies to systematically measure their impact on the environment.

Pre-tax profit is forecast to have increased by 14% in 2021 to €4.16 billion, rising to €4.68 billion in 2022 and €5.19 billion in 2023, according to consensus estimates published by Refinitiv.

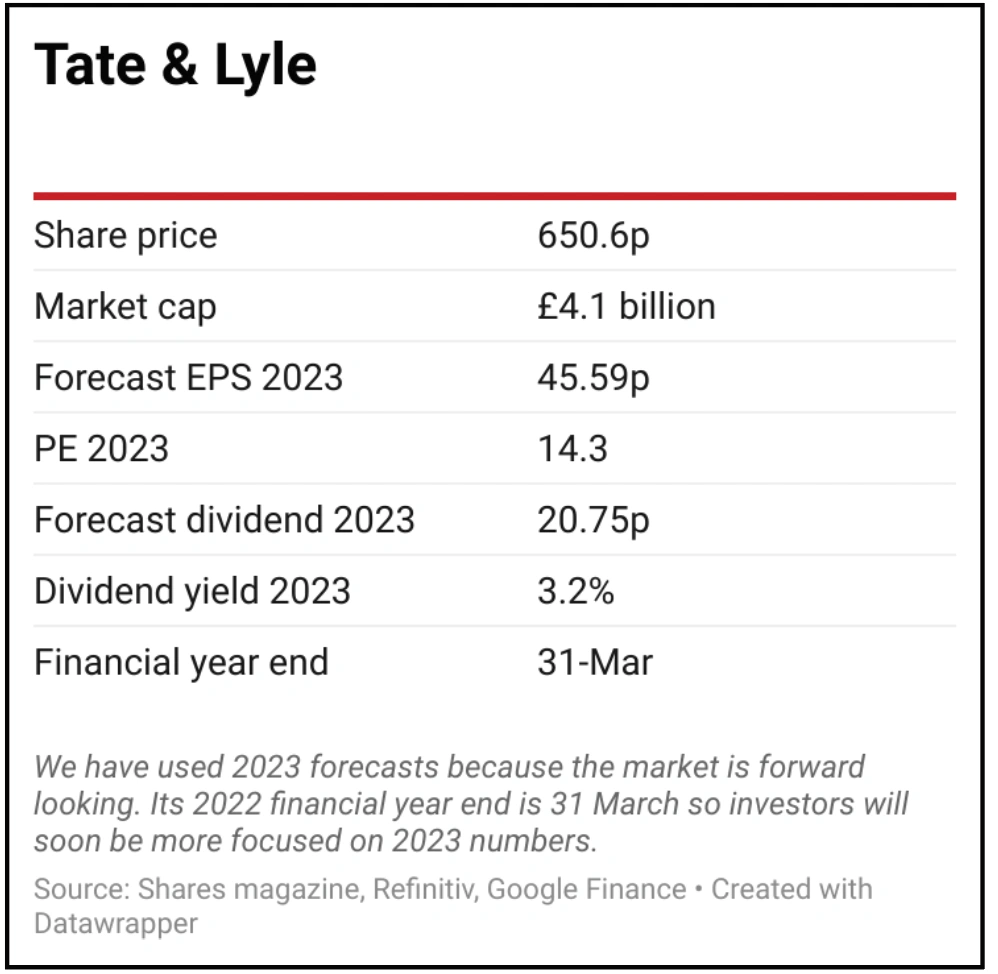

Tate & Lyle

Investors have an opportunity to buy Tate & Lyle (TATE) at an approximate 50% discount to ingredients peers. The FTSE 250 constituent’s imminent sale of a controlling stake in its North American Primary Products business will create a higher quality, ‘new’ Tate & Lyle with superior growth prospects which should drive a material rerating of a misunderstood stock.

Tate & Lyle is a global provider of corn-based sweeteners, starch ingredients and sucralose zero-calorie sweetener. The core business going forward is its specialty ingredients arm, Food & Beverage Solutions, which produces sweeteners, texturisers, fibres and stabilisers for beverages and dairy products, soups, sauces and dressings.

Concerns over cost inflation and the complexity of the business separation have weighed on sentiment towards Tate & Lyle, but the split will result in a sharper focus on fast growing, higher margin operations and allow Tate & Lyle to accelerate investment in innovation.

The company will split into two during the first quarter of calendar 2022, then pay a special dividend of around £500 million. Although the refocused, new-look Tate & Lyle plans to reduce the dividend to reflect the reduced earnings base, the payout ratio and progressive dividend policy will be maintained.

Robust first half results (4 Nov) for new Tate showed adjusted pre-tax profit up 20% to £85 million. Food & Beverage Solutions delivered double-digit organic growth across all regions, while revenue from new products rose by almost 50%. The results also confirmed that Tate & Lyle is managing cost pressures through price increases and productivity measures.

The trends driving Food & Beverage Solutions’ growth should continue, principally consumers’ demand for healthier foods and drinks that are lower in sugar and calories, with cleaner labels and added fibre. Acquisitions, notably the Sweet Green Fields stevia business, are also helping to accelerate new product revenue growth.

Risks to consider include new Covid variants, which could halt the recovery in out-of-home consumption, as well as dollar weakness, as the bulk of the group’s revenues are generated in the greenback and it reports in sterling.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

- 10 great stocks: Our best ideas for the year ahead

- Stock pick for 2022: Jet2

- Stock pick for 2022: Alphabet

- Why Meta could produce a positive surprise in 2022

- Fund managers: stocks that let us down in 2021

- The best performing stocks of 2021: big and small

- Emerging markets: Views from the experts

- Key events to watch for emerging markets in 2022

Funds

Great Ideas

- Stock pick for 2022: Tate & Lyle

- Stock pick for 2022: Roche

- Stock tip for 2022: Loungers

- Stock pick for 2021: Schneider Electric

- Stock pick for 2022: London Stock Exchange

- Stock pick for 2022: Accsys Technologies

- 8.5% share price return from our 2021 stock picks

- Stock pick for 2022: Pets at Home

- Stock pick for 2022: IOG