Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStock pick for 2022: Roche

Pharmaceutical giant Roche is class act with an attractive investment case. It has sector leading margins and returns on capital as well as clear growth catalysts.

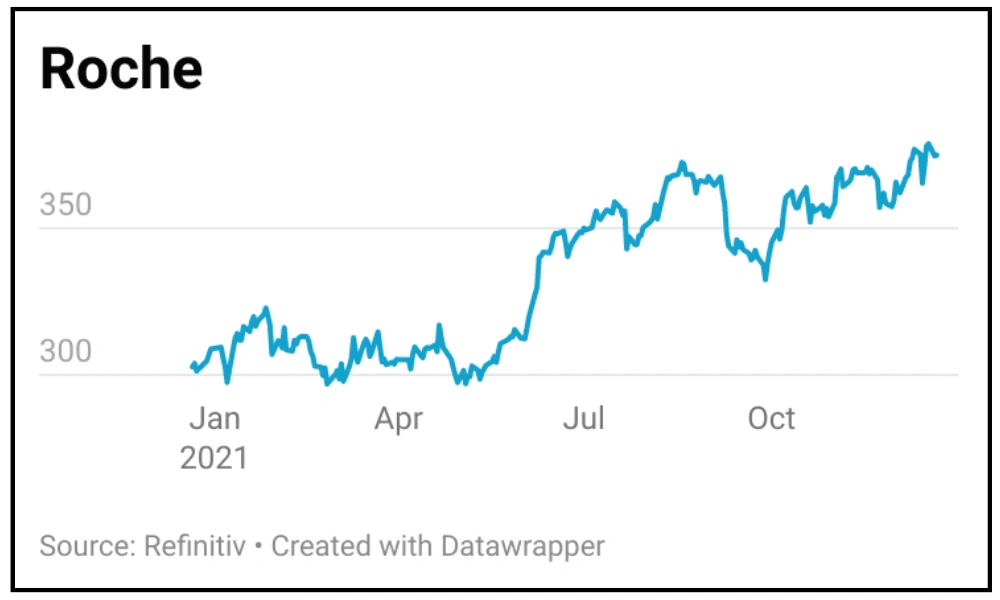

Roche has reached a turning point in the lifecycle of its drug pipeline where the growth in sales of new drugs is more than compensating for the loss of sales when patent protection expires, which leads rivals to sell copycat drugs more cheaply.

In October Roche increased full year guidance for revenues and profit to grow by a mid-single digit percentage, up from low single digit.

The company recently used its strong balance sheet to purchase Novartis’ 53.3 million shares in Roche for $20.7 billion with the intention of cancelling the shares. This will reduce the share count by around 5% and correspondingly increasing earnings per share.

In addition, Roche’s diagnostics division is seeing a tailwind from Covid-19 with increased PCR testing although this is a lower margin business.

Roche recently released detailed data of its Polivy drug in patients with previously untreated B-cell Lymphoma, a cancer of the lymphatic system, which means it could be on track for an additional approval in a potentially lucrative market forthe company.

Management believes approval of the drug for newly diagnosed patients could unlock a market worth $2 billion. Polivy generated sales of $178 million in the first nine months of 2021.

Roche’s Alzheimer’s drug Gantenerumab recently received FDA breakthrough therapy designation and stage three trial data is on track to be released in the second half of 2022.

The company’s eye disease drug Faricimab is expected to be approved in the first quarter of 2022 while its lung cancer drug Tiragolumab is expected in the final quarter.

It is worth noting that investing in pharmaceutical companies bears the risk of share price underperformance should drugs fail to gain regulatory approval.

Roche is composed of a pharmaceutical division which generates around 71% of total revenues and a diagnostics division. The latter owns the global marketing rights for the PCR (polymerase chain reaction) test, considered to be the gold standard for detecting genetic material.

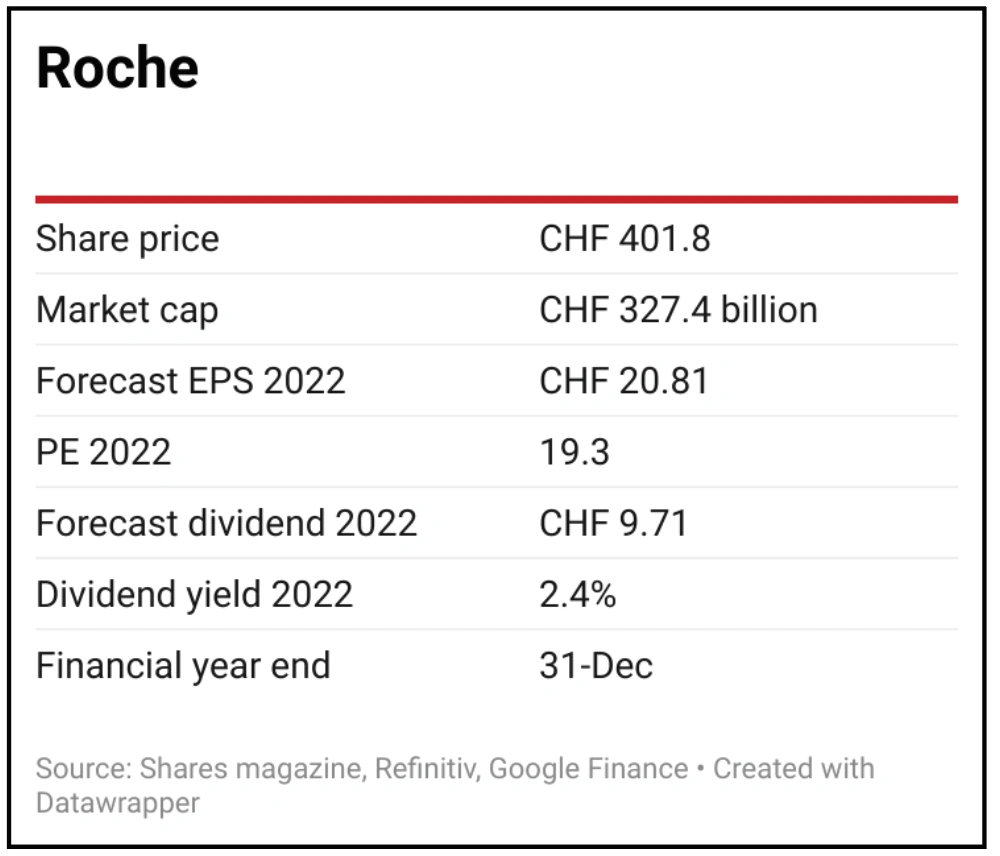

Investment Berenberg says: ‘Roche is successfully navigating a period of heavy erosion of its legacy drugs, with strong growth from its newer assets. We think there is scope for increased growth in the dividend once the legacy erosion has passed.’ The stock yields 2.4%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

- 10 great stocks: Our best ideas for the year ahead

- Stock pick for 2022: Jet2

- Stock pick for 2022: Alphabet

- Why Meta could produce a positive surprise in 2022

- Fund managers: stocks that let us down in 2021

- The best performing stocks of 2021: big and small

- Emerging markets: Views from the experts

- Key events to watch for emerging markets in 2022

Funds

Great Ideas

- Stock pick for 2022: Tate & Lyle

- Stock pick for 2022: Roche

- Stock tip for 2022: Loungers

- Stock pick for 2021: Schneider Electric

- Stock pick for 2022: London Stock Exchange

- Stock pick for 2022: Accsys Technologies

- 8.5% share price return from our 2021 stock picks

- Stock pick for 2022: Pets at Home

- Stock pick for 2022: IOG