Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBuy Marlowe for stable and growing earnings

Safety, testing and compliance company Marlowe (MRL:AIM) has an attractive business offering an unusual combination of defensiveness and profitable growth. The ‘buy-and-build’ strategy has been executed superbly, yielding impressive results.

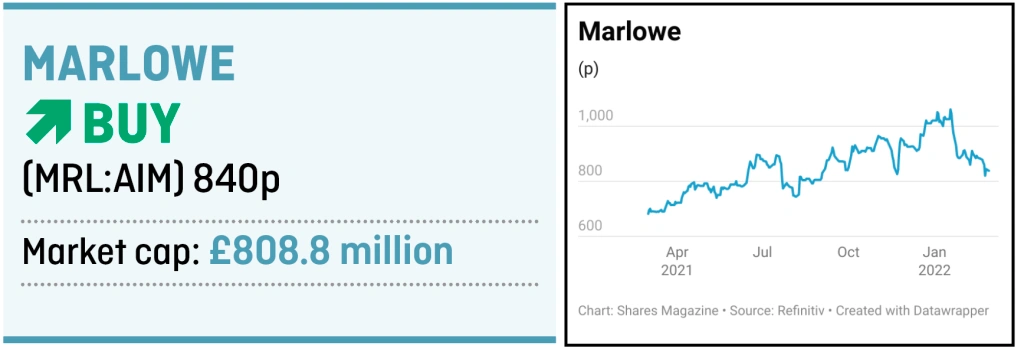

The shares have dropped around 20% from the recent highs in mid-January despite the company acquiring Optima Health for £135 million.

The transformational deal positions Marlowe as the leading player in the UK occupational health market.

And given the company is relatively insulated from inflationary pressures and geo-political ructions, in part due to the non-discretionary nature of its services, this represents a compelling buying opportunity. The shares are trading on 17 times consensus forecast earnings for the 12 months to 31 March 2023.

In the wake of the Optima deal, investment bank Berenberg upped its 2023 and 2024 earnings forecasts and now forecasts 19% compound annual earnings growth over the next three years.

That’s partly because the acquisition shifts group revenue and profit towards faster growth and higher margin end markets.

The enlarged Governance, Risk and Compliance division now represents 60% of profit and 40% of revenues.

Marlowe explained

Founded in 2015 by chief executive Alex Dacre and backed by businessman and political figure Michael Ashcroft, Marlowe has become a leader in specialist business-to-business services.

The strategy is to acquire and develop businesses that provide regulatory testing, inspection and compliance services.

The mission-critical nature of its services and high client switching costs means stickier customers and more stable revenue.

Services range from health and safety, human relations and employment law, fire safety, compliance, water treatment and air quality testing.

Marlowe targets sectors which are fragmented, offering it the opportunity to act as consolidator and build greater scale. This in turn drives operational efficiencies and higher margins.

A big market opportunity

The firm believes its total addressable market in the UK alone is worth £6.8 billion. The fire and safety sector is estimated at £1.7 billion but is growing slowly.

Services in this area come under the Testing, Inspection and Certification division.

However, of more interest are the employment law, HR and occupational health sectors, which are worth a combined £4.9 billion and are growing at around 6% per year.

These services come under the Governance, Risk and Compliance division.

Developing a strong track record

Marlowe started out as a cash shell (a stock market listed entity with no assets other than cash) called Shellshock. Since the name change six years ago the share price is up 808%.

While impressive, the performance has been supported by an increase in the fundamentals. For instance, cash generated from operations has grown from £600,000 in 2015 to £20.4 million in 2021, or around 3,300%.

Analysts have had a hard time keeping up with recent growth delivered by Marlowe.

Earnings revisions over the last 12 months have increased by 17% and 40% respectively for the 2022 and 2023 financial years, according to Stockopedia data.

Earnings per share estimates for the year ending 31 March 2022 are expected to be 36.75p while a year ago the estimate was 31.6p.

Rising earnings revisions tend to be a positive indicator for share price performance.

Growth ahead of target

At a February 2021 capital markets day, the company set out three-year plans to achieve £500 million of revenue and £100 million of EBITDA (earnings before interest, tax, depreciation and amortisation).

Achieving these goals implies EBITDA margins increasing from 16% to 20%, enabling greater cash generation and more ammunition for further acquisitions.

The Optima acquisition has propelled the company closer to achieving its targets. It also increases the potential for organic growth. Between 2019 and 2021 Optima grew at 12% a year.

Taking account of the Optima acquisition, annual revenue is running at around £400 million while EBITDA is running around £79 million. This implies a margin close to the group’s internal target at 19.6%.

As well as providing greater scale Optima pushes the company towards its goal of creating a ‘one-stop-shop’ addressing the full spectrum of business compliance needs.

Marlowe recently (10 Feb) enlarged its debt facilities from £130 million to £180 million, in addition to a further £60 million unused facility.

Securing greater debt capacity complements the support provided by long-term shareholders. It positions the business for further growth as it consolidates a fragmented marketplace.

Marlowe is an interesting company with an excellent track record of executing on its strategy and increasing shareholder value. Shares expects more of the same.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.