Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineKitwave delivers major upgrades

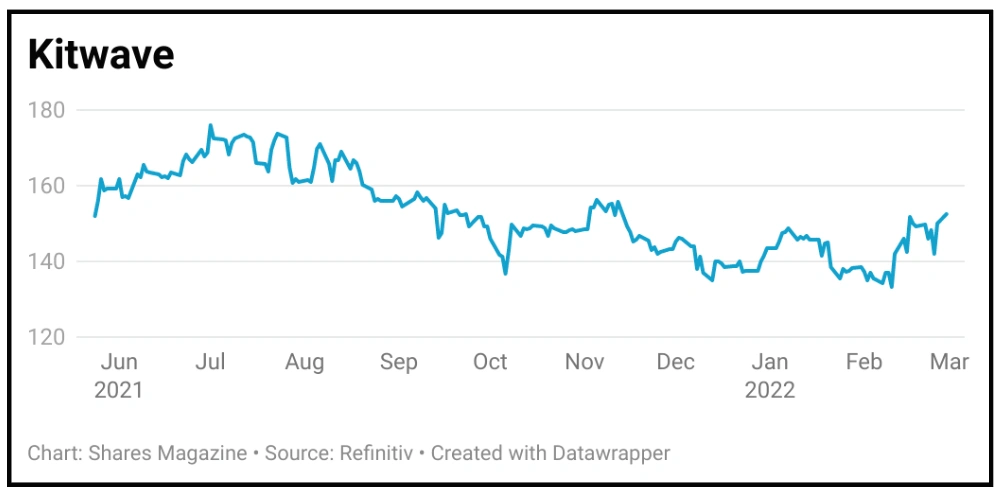

KITWAVE (KITW:AIM) 155p

Gain to date: 3.7%

Original entry point: Buy at 149.5p, 21 October 2021

Our ‘buy’ call on Kitwave (KITW:AIM) is now 3.7% in the money as the market responds to earnings upgrades from the food and drink wholesaler and we remain positive about the company’s organic and acquisitive growth prospects in the UK’s fragmented grocery and foodservice wholesale market.

Kitwave says current trading is slightly ahead of market expectations.

Revenue recovered strongly in the second half of the last financial year as Covid restrictions eased, enabling Kitwave to generate earnings of £15.1 million on turnover of £380.7 million. The company has navigated the pandemic, and supply chain and product availability issues, thanks to its in-house delivery fleet and strong relationships with suppliers.

With trading virtually back at pre-pandemic levels, Canaccord upgraded its 2022 revenue estimate by 2% to £462.5 million and its adjusted earnings estimate by 7% to £24.3m, implying growth of 61.7% year-on-year.

Kitwave trades on a price to earnings ratio of 9.9 with a 4.5% yield.

SHARES SAYS: Kitwave has plenty of room to grow as well as significant re-rating potential.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.