Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHigh active share: What is it and can it help you pick the best funds?

Fund selectors have a number of tools at their disposal to help them pick the best funds from a vast universe, one of which is the concept of active share.

Active share is a meaasure of how different a fund’s holdings are from its benchmark – being the index against which it measures its performance.

So if a fund had no holdings at all in common with its benchmark, it would have an active share of 100%, and if all its holdings were the same as the benchmark, its active share would be 0%. High active share is considered roughly 80% or more.

Investors can check fund factsheets to fund out active share, but bear in mind not all providers disclose it so you may need to ask.

Can active share help you spot good funds?

A famous piece of academic research from 2009 by Martijn Cremers and Antti Petajisto found that high active share funds were more likely to ‘significantly outperform’ their benchmarks.

But investment management company Vanguard later conducted its own research into active share and found no relationship between high active share and strong performance.

The group’s senior investment planner James Norton says there is a strong correlation between high active share and dispersion of fund returns, but returns could be positive or negative.

‘If active share is how your holdings differ from the benchmark, it means either your performance will be better, worse, or the same. There are more potential different outcomes but not necessarily in one direction or another.’

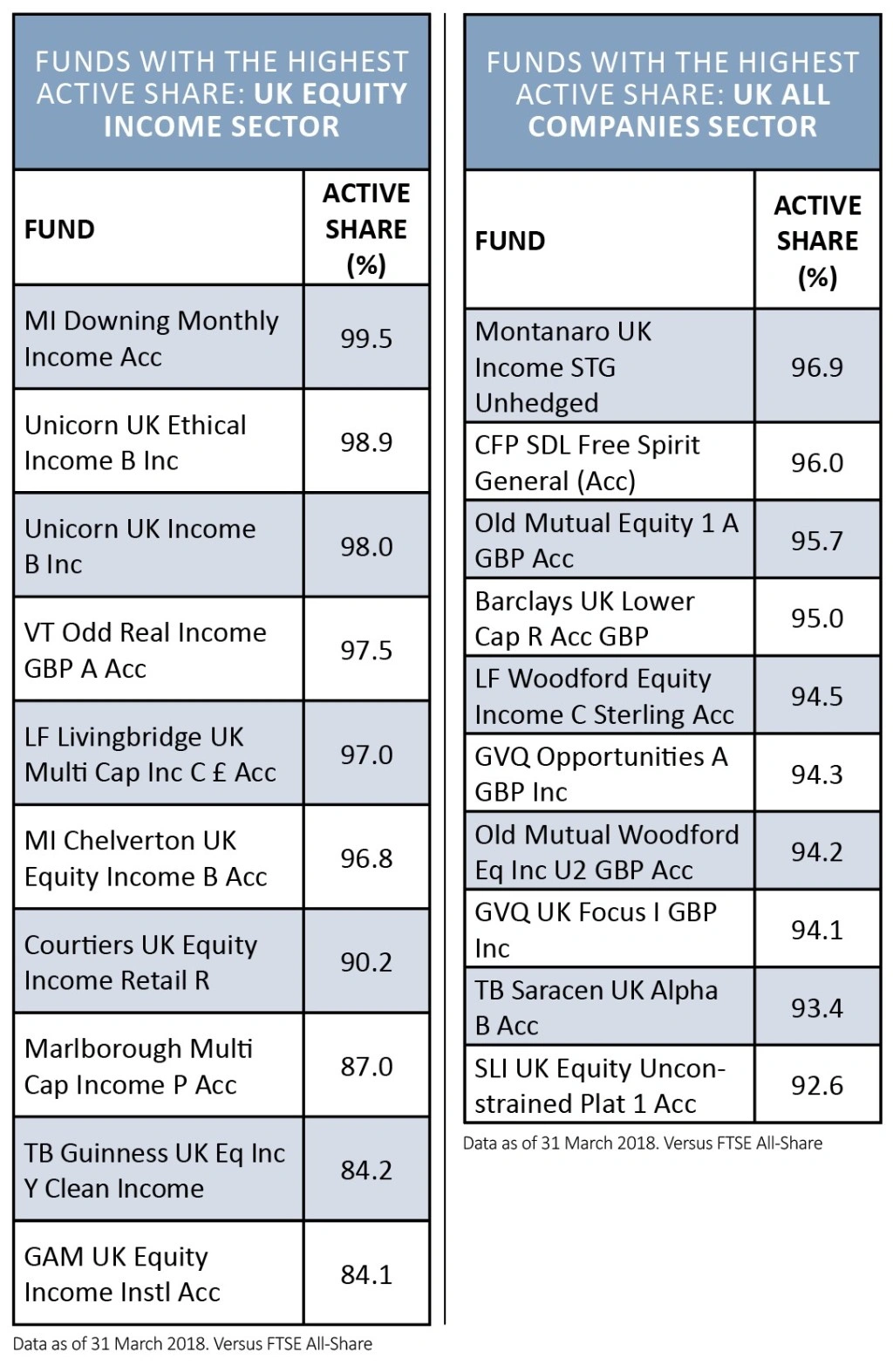

Current examples of active share

Shares analysed the Investment Association UK All Companies and UK Equity Income sectors and ranked them by active share versus the FTSE All-Share.

Top of UK All Companies was Montanaro UK Income (IE00B1FZRT49) with 96.9% active share. The fund used to be in the UK Equity Income sector but was kicked out in 2016 for breaching the yield requirements.

It no longer has an official benchmark, but still compares itself to the UK Equity Income sector on its factsheet.

Head of business development Tom Norman-Butler says the fund has a high active share because of its focus on small and mid-caps. It is also a concentrated 50-stock portfolio with a ‘one in, one out’ rule so it always remains at 50, and this too adds to its high active share.

In the UK Equity Income sector, Downing Monthly Income (GB00B61JRG28) comes top for active share at 99.5%. Manager James Lynch says: ‘The fund’s high active share is a result of our ability to exploit overlooked pricing inefficiencies by taking high conviction positions in UK smaller companies.’ He

invests exclusively outside the FTSE 100 with a focus on businesses below £500m market cap.

In fact, the top three funds by active share in the Equity Income sector are focused on small caps. These funds have a high active share because they are not invested in the big, blue-chip, dividend-paying companies that are the bread and butter of more traditional income funds.

Don't use active share in isolation when picking funds

Simon Evan-Cook, senior investment manager on Premier’s multi-asset range, says small cap funds will typically have a higher active share, but fund pickers still need to select the ones that will perform.

‘Small cap funds will naturally have higher active share than you would get from large cap funds. The trick for us comes in finding the good ones. We would only invest in funds with high active share, but we wouldn’t invest in funds just because they have high active share. It’s just one factor to be used alongside other analysis.’

Daniel Pereira, investment research analyst at Square Mile Investment Consulting and Research, says he does not believe high active share is better for returns, despite what the studies say. He points to Liontrust UK Smaller Companies Fund (GB00B57TMD12), which has a high active share but has not necessarily outperformed for this reason.

‘The Liontrust fund has outperformed because of the managers picking the right stocks over time, and their process of identifying intangible strengths in companies over the long term.

‘You also have to look at the stock selection effect, the holding period and timing of purchases and sales. If active share is incredibly high, you have to assess why you should have that particular benchmark if you differ from the index so much.’

He also highlights Old Mutual North American Equity (GB00B1XG9G04) as a fund which has outperformed despite its low active share, because of its focus on momentum.

Low active share isn't always bad

AJ Bell’s head of active portfolios Ryan Hughes singles out Man GLG Undervalued Assets (GB00BFH3NC99), run by Henry Dixon, a highly active manager who invests across the market-cap spectrum but has a relatively low active share of about 71%. Despite this, his fund is top quartile over one and three years.

‘If you look at Henry’s portfolio, his biggest holding is in Royal Dutch Shell and he’s also got BHP Billiton, HSBC, Lloyds, and British American Tobacco in his top 10, but he is definitely running a very active portfolio and is significantly underweight the FTSE 100 with only 36% exposure at the moment so, intuitively, you would expect him to have a higher active share. It just shows that interpreting one number doesn’t tell you the full story.’

In contrast, the fifth highest active share in UK All Companies is Woodford Equity Income (GB00BLRZQ737) at 94.5%, because of its long tail of small cap off-benchmark and privately listed stocks. But the fund has been underperforming because of stock selection mistakes.

This demonstrates that active share is not a straightforward predictor of performance, says Hughes. ‘It’s not as simple as “I am invested in a high active share fund therefore I am likely to outperform”. All you know if you invest in a fund with high active share is that you’ve got a greater chance of getting a return different to the benchmark.’

Helps you avoid closet trackers

Although high active share is no guarantee of better performance, it can help you get better value for money by weeding out ‘closet trackers’. These are funds which stay close to the benchmark like a passive product would (such as a tracker fund or exchange-traded fund) and perform in a similar way, but still charge the higher fees of an actively-managed fund.

‘For me, the main benefit of looking at a fund’s active share is to identify if active share is too low. If it’s too low, then you may be better off in a cheaper passive product that tracks the benchmark,’ said Pereira at Square Mile.

Hughes expands on this point with an example from the UK All Companies sector. JPM UK Equity Core (GB00B55QSH09) is among the lowest for active share in the UK All Companies sector at 20.2%, but has an ongoing charges figure of 40 basis points. A FTSE All Share tracker can be bought for as little as 10 basis points.

‘If we look at the discrete returns, it outperformed in

2016 but it underperformed in 2017 and is underperforming this year, so would you be better off in a tracker versus that fund? It’s hard to say, but what you do know is you’re getting a portfolio that looks very similar to the market and you know you are paying a higher price than you can get for a passive.’

JPMorgan argues that its JPM UK Equity Core fund is designed to stick closely to the index but, unlike a tracker, it aims to deliver small incremental excess returns that add up over time.

‘It does this by taking small overweight positions in attractively valued, high quality stocks with positive momentum, and small underweight positions in stocks that are expensive, low quality and have weak momentum,’ says JPMorgan.

‘As a result, at the sector level, weightings will be closely aligned to the index. The 40 basis points ongoing charges figure is less expensive than the average active equities OEIC. The fund’s long-term investment performance is strong, including 75 consecutive months of outperforming on a rolling three-year basis net of fees.’ (HS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.