Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHousebuilders: farewell mega profits?

All economies experience recurring and fluctuating levels of economic activity over time, with the five main stages of the business cycle running as follows: growth, peak, recession, trough and recovery.

The business cycle is usually replicated in the stock market with the market going up when the economy is growing and going down when it is contracting.

Different types of stocks tend to perform well at different points in this cycle so having an awareness of where we are in the cycle could give you a material advantage as an investor.

We can see a number of signs that housebuilders are at the top of their cycle and earnings growth will be much harder to achieve from now on.

There is also an argument to suggest that engineers and electronic companies are trading on too rich an equity rating against their near-term outlook, earnings strength and position in their business cycle.

We will now explore the broader topic of cycles and look at various industries in more detail including a large section on housebuilders at the end of this article.

UNDERSTANDING CYCLES

Not all stocks are highly correlated to a cycle; defensive or non-cyclical stocks should experience steady demand regardless, while some firms benefit from a structural change unrelated to fluctuations in the economy.

Online retailer ASOS (ASC:AIM), for example, continued rising through the last major recession 10 years ago as it benefited from an increasing shift for people to buy clothes over the internet.

Nonetheless, a lot of businesses have at least some exposure to what is happening in the wider economy. And investors should take particular note to where a particular company may be in the cycle as that can have an influence on the direction of a share price.

For example, a company experiencing earnings pressure could see its shares trade on a lower rating if analysts expect lower profits in the near future – something that is very relevant to the housebuilding sector at present.

LEADING INDICATORS

Calling where we are in the cycle is no easy task. Most measures of economic growth, including GDP, are lagging indicators so we can only identify the point at which the economy peaked in hindsight.

However, there are leading indicators which can at least help us make an educated guess. The stock market itself is a leading indicator as it reflects the expectations of lots of individual investors. Other closely followed yardsticks include purchasing managers’ index data and surveys on consumer sentiment.

Most observers put us somewhere between the growth and peak phase. The current stock market cycle started at the beginning of 2009 as the global economy began to emerge from the most significant financial crisis since the 1930s.

Since the beginning of March 2009, the FTSE 100 has nearly doubled in market value and in the US the S&P 500 is up by nearly 300%.

There have been periods of volatility along the way, notably around the sovereign debt crisis in Europe in 2011 and 2012 and fears of a hard landing for the Chinese economy in 2015 and early 2016, but for the most part equities have enjoyed an upwards trajectory.

By some people’s estimation, the bull market in the US is approaching a new record in terms of duration and seemingly stretched valuations are understandably making investors nervous, but some experts think it is premature to call an end to the growth phase.

THERE ARE STILL BELIEVERS IN GROWTH

Investment bank Jefferies produces a monthly ‘Short Cycle Monitor’ report focused on US industrial companies.

In the May edition it commented: ‘Our analysts believe concerns around reaching cycle peaks are overblown and they believe there’s further runway for growth and highlighted continued strength in underlying fundamentals, tight supply/demand dynamics, and management teams’ confidence in recovering cost inflation with price.’

The follow-up report in June reiterated this belief and noted several of the leading indicators it followed had improved.

A key risk which could accelerate us towards a peak and ultimately recession is an escalating trade war provoked by more protectionist policies in the US. Understandably this issue is dominating the short-term direction of markets at present.

Investors should keep in mind that downturns can often be a lot briefer than rallies and it is important not to over-react when the cycle turns, or you could crystallise substantial losses before stocks have had an opportunity to bounce back.

And don’t forget that different industries can perform in different ways at various points in the cycle so they all won’t move in tandem.

British engineering appears to be in rude health. Spin through the latest updates on trading prospects for most companies and you’ll read upbeat, if not positively glowing, assessments.

Before you get carried away, take some time to look at the sector’s position in the cycle. We think shares have got ahead of themselves and many engineers’ valuations are too rich.

‘We have seen robust growth in the first four months of the year in spite of the foreign currency headwind... the board now expects full year revenue to be higher than previously expected,’ said Bodycote (BOY) at the end of May.

‘Trading performance has exceeded expectations in the first quarter,’ confirmed Vesuvius (VSVS) just a few weeks earlier, also taking the opportunity to upgrade full year 2018 guidance.

Forecasts for Bodycote, the heating and thermal systems engineer, have been upgraded at least twice this calendar year thanks to robust end market demand.

STRONG EARNINGS MOMENTUM

Analysts have been getting increasingly confident of earnings outperformance potential across the engineering sector since late last year.

In November investment bank UBS picked up on the trend, pointing out that eight out of 13 UK engineers had beat expectations on organic top line growth in the third quarter of 2017 (July to September). At the time they calculated average organic growth was running at 7%.

Unsurprisingly, this optimism has percolated from equity researchers to investors who have chased sector share prices higher. Both Bodycote and Vesuvius are currently trading at, or very close to, five year share price highs.

They are joined in hitting multi-year highs of late by actuators and flow controls manufacturer Rotork (ROR), and values and pumps business Spirax-Sarco (SPX); both of whom are enjoying renewed interest from the oil industry.

This is having the effect of stretching sector price-to-earnings multiples beyond the low to mid-teens averages you might expect for these typically cyclical businesses. Shares in Spirax-Sarco and Rotork are currently changing hands at 25 times forecasts earnings, according to Reuters data.

ENTERING LATE CYCLE TERRITORY

There is presently little hint that demand is drying up for most UK engineers, while analysts at JP Morgan, Jefferies and others believe there could be another year or two of economic expansion growth to come.

Joachim Fels, global economic advisor at Pacific Investment Management (commonly called PIMCO) feels similarly. But he does believe we are entering into late-cycle territory, a period when industrial companies often start to struggle.

‘Industrials have historically been weakest very late-cycle when the ISM Manufacturing Index was under 55 and falling,’ says asset manager Invesco.

The ISM is the US version of the UK’s manufacturing PMI, or Purchasing Managers’ Index. June’s PMI came in below May at 54.0, versus 54.4, and the trend has been down since peaking in November last year at 58.3.

In May’s update Bodycote management made the point that the business ‘has limited forward visibility’.

Against investor expectations that are already high, there may be little scope for engineers’ earnings outperformance to drive further share price gains, while a fall in demand could sharply slam the brakes on new contracts and hit market sentiment towards the sector.

VALUATIONS ARE LOOKING TOO HIGH

Share price re-ratings running ahead of earnings upgrades is becoming an issue for electronics hardware manufacturers too.

This was the bedrock of Goldman Sach’s thesis in cutting its recommendation from ‘buy’ to ‘neutral’ on precision engineer Renishaw (RSW).

Its products are used widely in aerospace, automotive, healthcare and other industrial markets.

‘While the longevity of growth is still an open debate, we see limited scope for further outperformance,’ said Goldman Sachs. Its analysts also turned neutral on industrial controls group Spectris (SXS) for the same reasons.

‘Since adding them [Renishaw and Spectris] to the buy list on 12 December 2017, and 3 April 2018, respectively, the shares are up 14% and 25%,’ the Goldman analyst explained. That compares with a -2% and 4% performance respectively for the FTSE World Europe index.

FEROCIOUS APPETITE FOR TAKEOVERS… TOP OF THE CYCLE BEHAVIOUR?

A final point to consider is a relative boom in mergers and acquisitions, and what that might tell us about a sector and valuations. The UK packaging sector’s biggest player Smurfit Kappa (SKG) shot into the headlines recently after twice rebuffing takeover approaches from International Paper of the US, the world’s largest paper and packaging supplier.

Packaging group DS Smith (SMDS) has also been getting increasingly active lately, including a recent €1.9bn deal to buy Europac and several other smaller deals over the last year or so.

‘Record merger and acquisition activity is all well and good but they tend to occur near the top of stock market cycles, when animal spirits are running,’ says AJ Bell’s investment director Russ Mould.

The housebuilders have so far this year endured mixed fortunes in terms of share price performance and things got worse on 21 June when Berkeley’s (BKG) influential chairman Tony Pidgley repeated a warning first given in December 2017 that profits at his company had peaked.

This was a significant moment for the housebuilding sector. ‘History shows that when Pidgley acts, markets should listen,’ says Mould

at AJ Bell.

‘Berkeley sold land and houses in the late 1980s in the view that the housing market had overheated and it was vindicated by the vicious downturn of 1990-92. The company began to build up its land bank once more, to the benefit of its balance sheet and shareholders alike. Berkeley isn’t selling now but it is not seen to be a huge net buyer either.’

As companies rebuilt following the 2007 to 2009 crash, the performance of the housebuilding sector began to take off in the latter half of 2012. This chimed with their traditionally strong performance at the start of a cycle.

Arguably this outperformance has been extended through the cycle by low interest rates driving mortgage availability, a robust housing market, and Government support in the form of the Help to Buy scheme.

There are also undoubtedly strong dynamics behind the UK housing sector with the supply of new homes still failing to keep up with demand.

For this reason, the volume of houses built is unlikely to fall off a cliff. What is in question is how profitably these houses can be built.

Berkeley’s pre-tax profit is forecast to fall by 32% in the year to April 2019 to £639m, before declining further to £505.5m in 2020 and £498.3m in 2021. That’s quite a depressing earnings outlook.

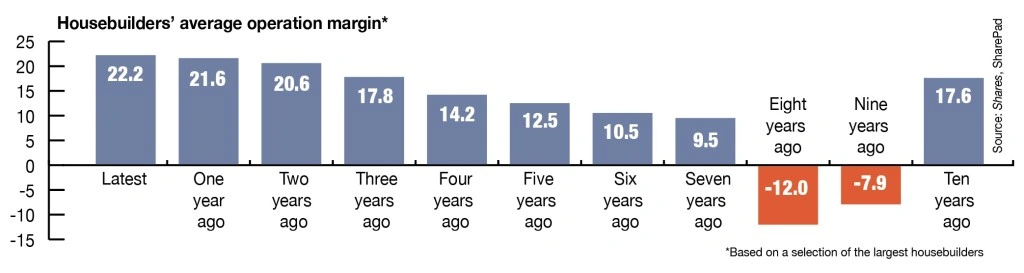

HAS PROFIT NOW PEAKED?

The bar chart below shows the average margin performance for the sector’s heavyweights between 2007 and 2017.

Margins are now substantially higher than they were in 2007 at the peak of the previous cycle.

The negative operating margin for the years immediately after this point reflects the fact many housebuilders racked up losses in the wake of the financial crisis.

But having bought land cheaply in the recession and then found support from aforementioned factors, profit, cash flow and dividends have all soared.

There have recently been signs that this positive picture is clouding over as house price growth stalls and costs begin to creep up.

Crest Nicholson (CRST), which operates at the high end of the market, warned on margins on 12 June and the same day Bellway (BWY) said it was offering incentives to help shift premium-priced properties.

The housing market is interconnected and margin issues at the top end could start to filter down the property chain.

IS A MORE NEGATIVE OUTLOOK ALREADY BEING FACTORED IN?

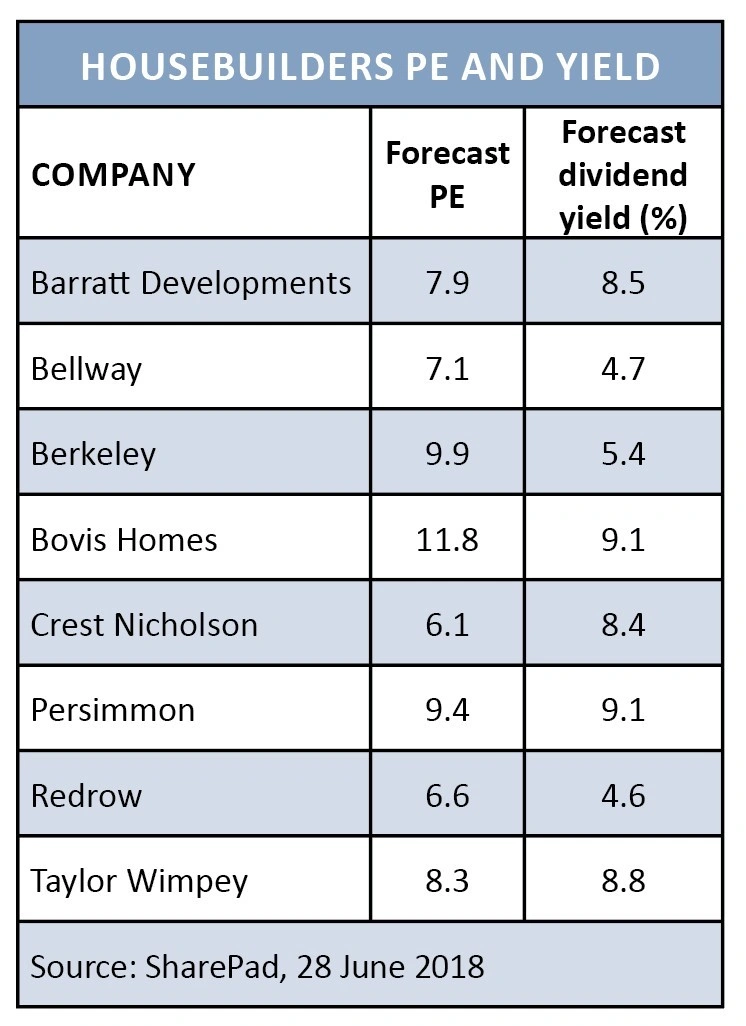

Investors will want to know if this negative situation is already being priced in by the market. Looking simply at price-to-earnings (PE) ratios and dividend yields, you could be forgiven for thinking this to be the case.

The accompanying table shows the PE and dividend yield for the sector’s main constituents. An average yield of 6.8% compares with around 4% for the FTSE 100.

However, on a price-to-net asset value (NAV) basis, typically a more reliable measure of value for housebuilders, sector constituents are trading roughly where they were in 2006 according to data from SharePad.

At that point Redrow (RDW), for example, traded on a trailing price to NAV of 1.5-times compared with 1.6-times today.

Berkeley’s 2006 price-to-NAV was 2.27 times and is now 1.9 times; and Barratt Development’s (BDEV) was 1.25 times against 1.2 times now.

However, even if housebuilders are cheap on certain metrics, weak sentiment could prevent this value being unlocked in the short-term. You have to remember that decent companies will struggle if their sector is out of favour. Likewise, bad companies can do well on the stock market if their sector is in favour.

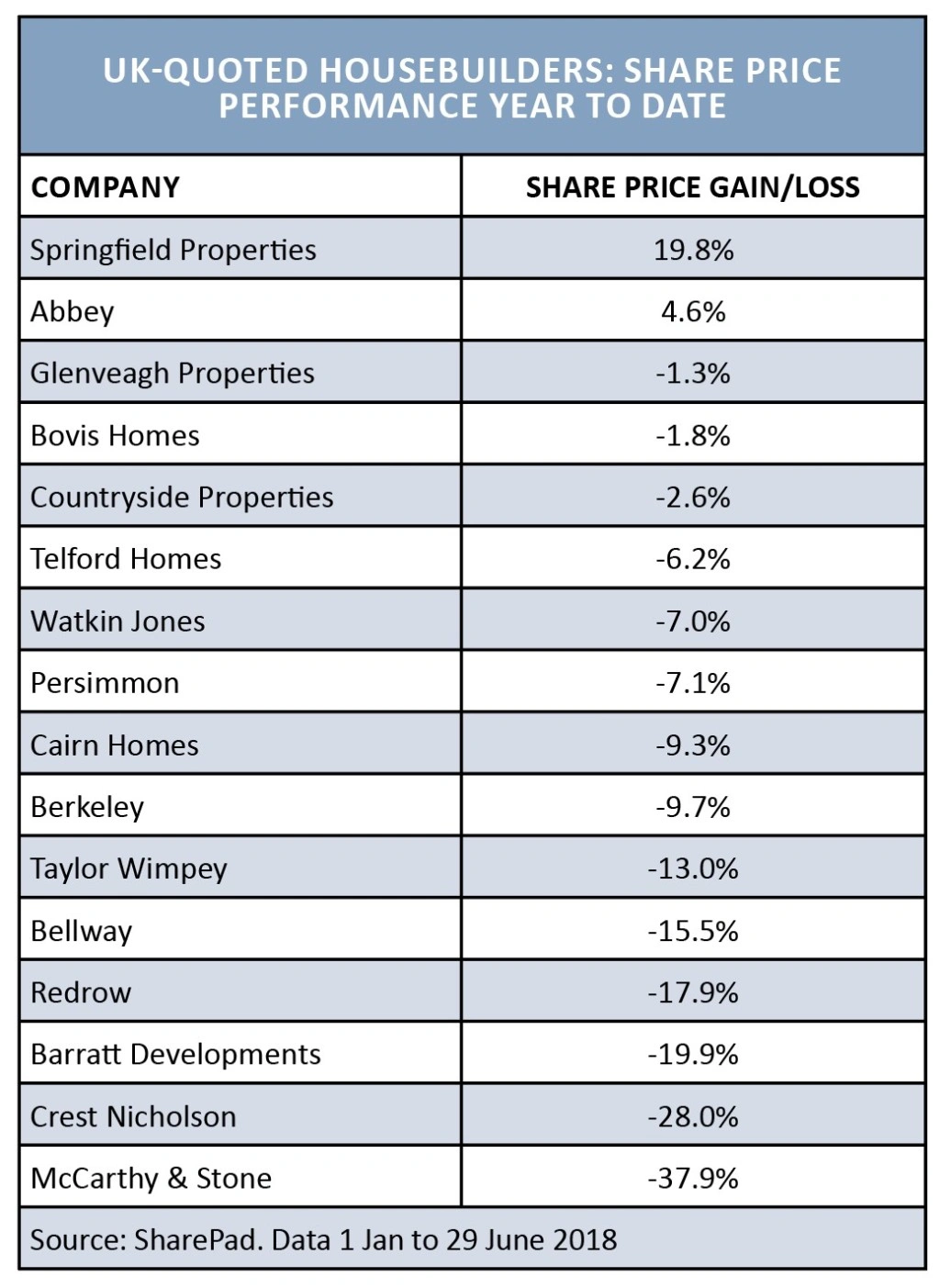

Most housebuilders have struggled on the stock market this year with only two companies producing a positive share price return, being Abbey (ABBY:AIM), up 4.7%; and Springfield Properties (SPR:AIM), up 19.8%.

The rest have seen share price declines upwards of 38% in the case of McCarthy & Stone (MCS) due to a profit warning, or roughly 10% to 20% decline for most of the big names on the market.

The sector is struggling which suggests investors are starting to get nervous about housebuilders’ prospects. We’re very cautious about the sector and believe you should think seriously about taking profit.

Yes, these companies could still generate decent dividends in the near term and still make a profit – but the potential for a significant drop in profit makes us feel this is not a sector to own at present. Negative sentiment could be the overriding force and drag everyone down.

Get out, wait until the market has had time to price in lower earnings and there has been a natural rotation for investors out of the sector;

and only then potentially consider buying back if valuations have dropped to really attractive levels. (TS/SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.