Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTeam17 could be a superb way to play soaring demand for video games

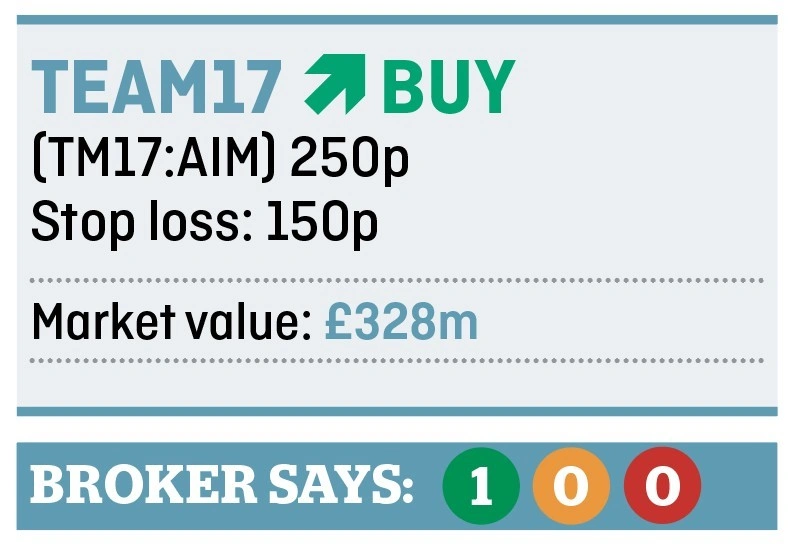

With the initial hype surrounding Team17’s (TM17:AIM) stock market flotation dying down, now is a good time to take a position in the video games outfit.

The stock rocketed on the 165p issue price in May to hit a high of 270p but has now settled at the 250p mark. In Shares’ experience of previous successful IPOs (initial public offerings), the share price tends to fall back after an initial surge and then moves higher again as short term traders are replaced by longer term investors.

The launch of Team17’s next title Overcooked 2 will happen in August, and with significant potential upside to forecasts from new releases and penetration of the Chinese market, we think this looks an exciting story.

WHY IS IT ATTRACTIVE?

Independent developers like Team17 are enjoying a purple patch, with many more titles coming to market thanks to greater availability of game engine software and the digital distribution of games.

According to house broker Berenberg, the company has delivered growth four-and-a-half times faster than the global video games market and more than three times that of large publishers between 2015 and 2017.

It also enjoys better earnings before interest and tax (EBIT) margins than much of its peer group at around 37%.

These qualities come at a cost, with the shares trading at 28.7 times Berenberg’s forecast 2019 earnings per share. We’re happy to pay this premium rating given the growth on offer and the scope for positive surprises with forecasts pitched at a conservative level.

WHAT DOES IT DO?

Long-time gamers may be familiar with Team17 thanks to its successful Worms franchise in the 1990s which remains popular today. The company is also one of the most well-established industry names.

In 2011 it reached an important point in its development as chief executive Debbie Bestwick and finance chief Paul Bray completed a management buyout around the launch of its Team17 Games Label.

This is essentially a platform which allows independent developers to bring their games to market under a revenue sharing model. The company is selective about the games which it promotes with only 1.5% of prospective games reviewed making it on to the Games Label.

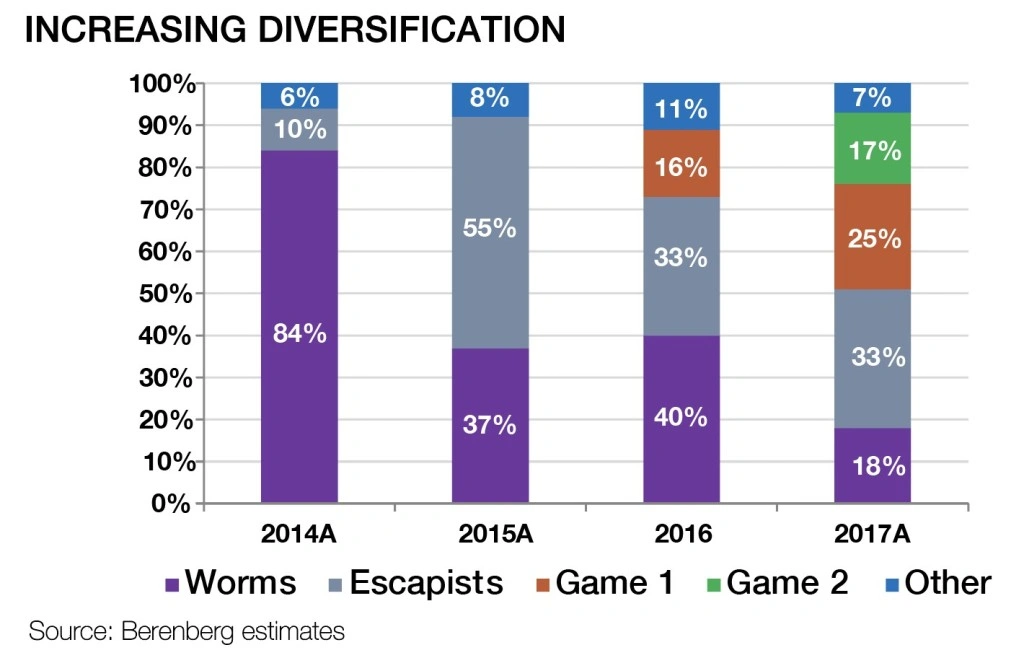

This incubator model has helped diversify the portfolio of games such that the Worms franchise has gone from accounting for 80% of group revenue in 2014 to just 18% by 2017.

Around half of its revenue comes from its back catalogue of purchase-to-play games and its titles typically require limited development and marketing spend. Games are released online and are often marketed through social media rather than more expensive routes like TV.

In addition there are opportunities to launch sequels as well as to release them on new platforms like smartphones or different games consoles, for example.

INFLECTION POINT IN ITS GROWTH

Berenberg comments: ‘With a back catalogue of successful titles to provide a supportive platform, new titles from previous franchises and newly signed Games Label titles coming to market in 2018 and 2019, Team17 has entered an inflection point in growth, profitability and market presence.’

The company has a strong balance sheet and is forecast to end 2018 with net cash of £15m. The IPO saw it raise £45m in new money via a heavily oversubscribed placing. Existing shareholders also sold circa £62m of stock as part of the listing.

The directors believe the listing will help Team17 to invest in future expansion, retain its independence, enhance its profile and provide the ability to incentivise existing and future staff.

Among the risks associated with investing in the business is the reliance on CEO Bestwick who is closely involved in the decision to green-light games. She may not have as much time to devote to this process as she has historically enjoyed and there is always a chance that she might leave the business.

Mitigating this, the company has a lot of experienced people involved in this selection process.

Demand for games could also be affected by any weakening in the economy, however many of Team17’s games are available at relatively low price points compared with blockbuster titles and often benefit from a cult or niche audience.

Earnings profile

Fundamentally this looks like a great business which should appeal to investors who like fast growing small caps. Adjusted pre-tax profit is forecast to triple between 2016 and 2018, from £4.1m to an estimated £12.5m. This figure is then expected to hit £13.8m in 2019.

Berenberg believes there is scope for Team17 to materially beat current earnings estimates if it achieves success in Asia and gets a higher return on its new label titles.

‘By partnering with the highest-quality developers and titles on a revenue share arrangement, its model can scale more quickly than traditional game publishers,’ says the investment bank. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.