Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDonald Trump is trying to reverse 48 years of economic history

When the latest meeting of the US Federal Open Markets Committee concludes on 18 September chair Jay Powell is widely expected to announce an interest rate cut, according to the CME Fedwatch tool.

The only debate concerns whether it will be a quarter-point or half-point reduction from the current level of 2.25%.

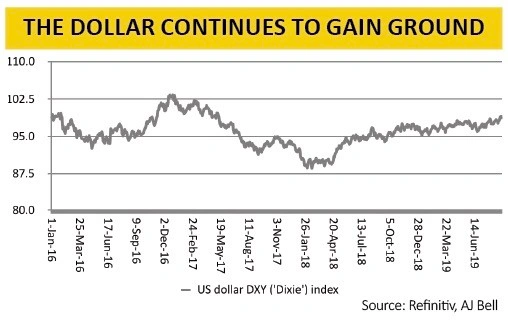

And yet the US dollar continues to rise despite the huge U-turn in Fed monetary policy and President Trump’s attempts to lean on the central bank for more action to talk the dollar down.

Using the trade-weighted DXY (or ‘Dixie’) index as a benchmark, the dollar stands at a 2.5 year high, around the 99 mark.

This takes us back to a topic called the Triffin dilemma, whose influence should be followed by investors in the coming months.

Triffin explained

When then-US President Richard Nixon took America off the gold standard in 1971 the dollar effectively became the world’s reserve currency. Yet Professor Robert Triffin had already seen the catch in a book he produced in 1960 called Gold and The Dollar Crisis: The Future of Convertibility. He argued that the greenback’s global reserve currency status would come at a cost – either to America or the world.

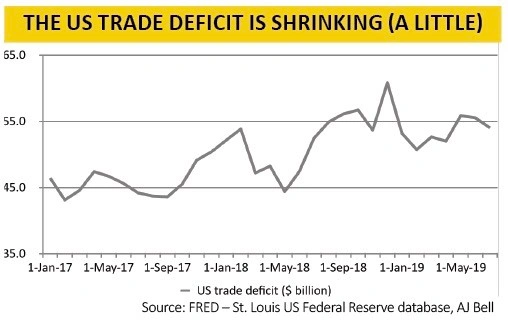

Triffin asserted that to provide the world with enough dollars, America would always have to run a trade deficit and import more than it exported, paying out more in dollars than it received, and run an ever-growing budget deficit for good measure.

This is all well and good while confidence in the dollar remains, lenders are happy to hold US Treasuries and the US is happy to run a trade deficit. But it becomes a problem if lenders lose faith (as they did briefly in 2008) or America’s trade policy is changed.

This is where President Trump enters the equation. While he is happy to run ever-bigger budget deficits his policy to put ‘America first’ means he is trying to reverse 48 years of economic history and reduce the US trade deficit.

If Trump succeeds, dollars would flow back to America and drain the global economy of the greenbacks upon which it is reliant.

The President has only made little, if any, progress with the US trade deficit so far but the dollar has gained during this period and the world’s economy and financial markets have already started to feel the effects.

Argentina cries again

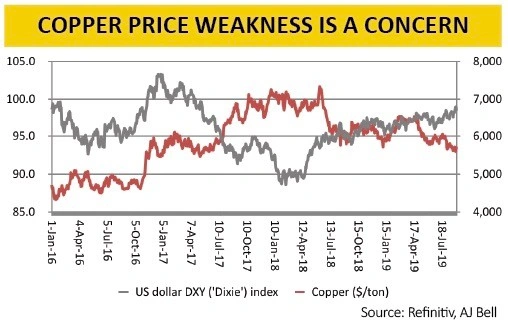

A strong buck is traditionally seen as deflationary – it increases both the costs of dollar-priced commodities and the interest costs of those nations who borrow in dollars and not their own currency, a particular facet of emerging markets.

Increased raw material costs eat into corporate profit margins and cash flows (and potentially dividends) while coupon payments to bondholders crimp governments’ scope to invest and potentially economic growth.

We are already seeing early signs of strain. First, the copper price, a traditional proxy for global economic health thanks to the industrial metal’s widespread use, is languishing at a 2.5-year low of around $5,500 a tonne.

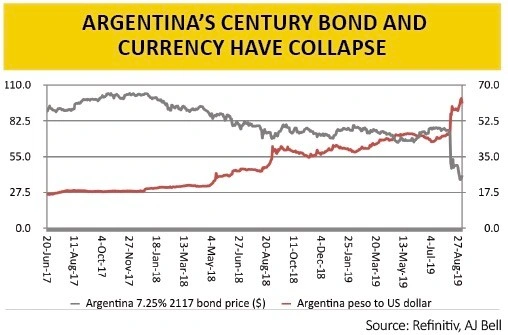

Second, Argentina, a huge borrower in dollars, is suffering a collapse in confidence and its currency after President Mauricio Macri’s unexpected defeat in an early poll ahead of October’s election.

That has forced him to postpone repayment of $7bn in debt, talk about ‘reprofiling’ the nation’s $101bn in liabilities and impose capital controls to support the peso.

Those brave souls who bought Argentina’s 100-year (or so-called ‘century’) bond in 2017 may now be feeling pretty sick, though they really should have known better given Buenos Aires’ history of eight defaults since the early 1800s.

Cracks in the wall

It remains to be seen whether these cracks become a major fissure in financial markets or whether central bank interest rate cuts can paper over them.

Currency controls have helped the Argentina peso to rally a little. But they did not work in Malaysia in 1997 and the ripple effects then were huge, even if it took until mid-1998 for them to knock global markets.

Investors are used to (relatively) easy access to markets and assets. Capital controls stop that, just like the gating of a fund – and we all know how badly that has gone down this year in the case of Woodford.

It is to be hoped that the Triffin dilemma does not become more acute and claim more victims and investors need to keep an eye on emerging markets to check for any more market stresses – Turkey, for one, may not be out of the woods yet.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.