Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWeighing up the future for Centrica

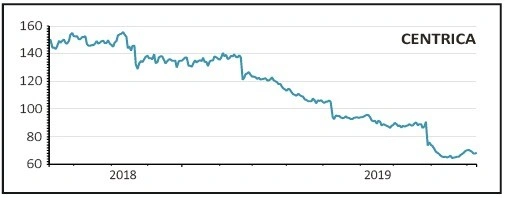

Britain’s biggest energy company Centrica (CNA) has been through a rough few years, culminating on 30 July when it reported a 49% fall in operating profit, slashed its dividend by more than half, announced plans to exit its oil and gas business and said that chief executive Iain Conn would leave the business.

The focus now shifts to the potential shape and size of Centrica going forward – and whether it could be bought by someone else given its shares are cheap and it is about to become a more streamlined business.

In the UK, Centrica will further reduce its cost base and improve its proposition centred on home energy management.

The company is targeting £1bn of annualised efficiencies over the 2019 to 2022 period, a third higher than its prior target. It estimates these savings will cost £1.25bn to deliver.

The aim is to become the most competitive provider in all markets where the company operates, with hopes to reignite customer growth and rebuild margins.

The planned disposals of oil and gas business Spirit Energy and an interest in nuclear generation – expected to happen by the end of 2020 – could net the company around £2.7bn according to analysts at Berenberg. This would slash net debt by close to 80% from £3.37bn to £0.67bn.

The analysts are sceptical of the cost cutting efforts, especially given past experience where the original £1.1bn of savings envisaged over the 2015 to 2018 period were overwhelmed by pricing pressures in the retail business, effectively being nullified.

However, the current plans build on pervious improvement and according to management the new initiatives should deliver around £20 of savings per dual fuel customer, in real terms, which would propel Centrica into a top quartile cost position.

There is a chance that the customer base will stabilise and, combined with a strong brand, may even see some growth.

Having rebased the dividend to 5p per share, the plan is to progressively grow it in line with the long-term growth in earnings and cash flow, targeting a dividend cover of 1.5 to 2-times.

The company is targeting a strong investment grade credit rating and anticipates retaining asset divestment proceeds to reduce debts.

Centrica shares currently offer a dividend yield of 7.6%, and trade on eight times forecast December 2020 earnings per share. It is the cheapest company in the sector, looking at enterprise value-to-revenue and enterprise value-to-earnings before interest, tax, depreciation and amortisation.

Berenberg believes Centrica could be a future takeover target for oil majors pursuing climate change goals. The idea is that big oil and gas companies could see M&A as a way to ‘dilute’ their carbon footprints by increasing their exposure to low-carbon energy.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.