Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe FTSE 100 firms which have delivered a decade of negative returns

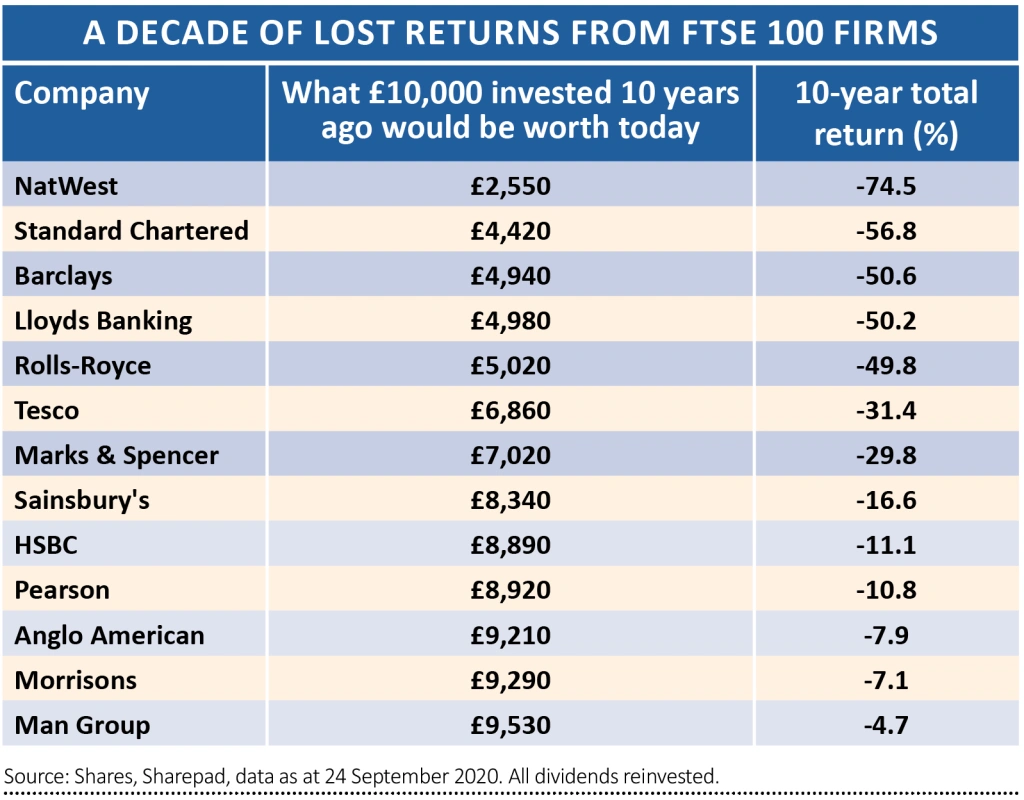

Thirteen companies in the FTSE 100 have lost money for investors who have held the shares over the past decade, based on share price performance and dividends reinvested for the 10 years to 24 September 2020.

In comparison over the same timeframe, the 10-year total return for the index stands at 52% and the top performer is tool hire firm Ashtead (AHT) which has delivered a total return of 2,750%.

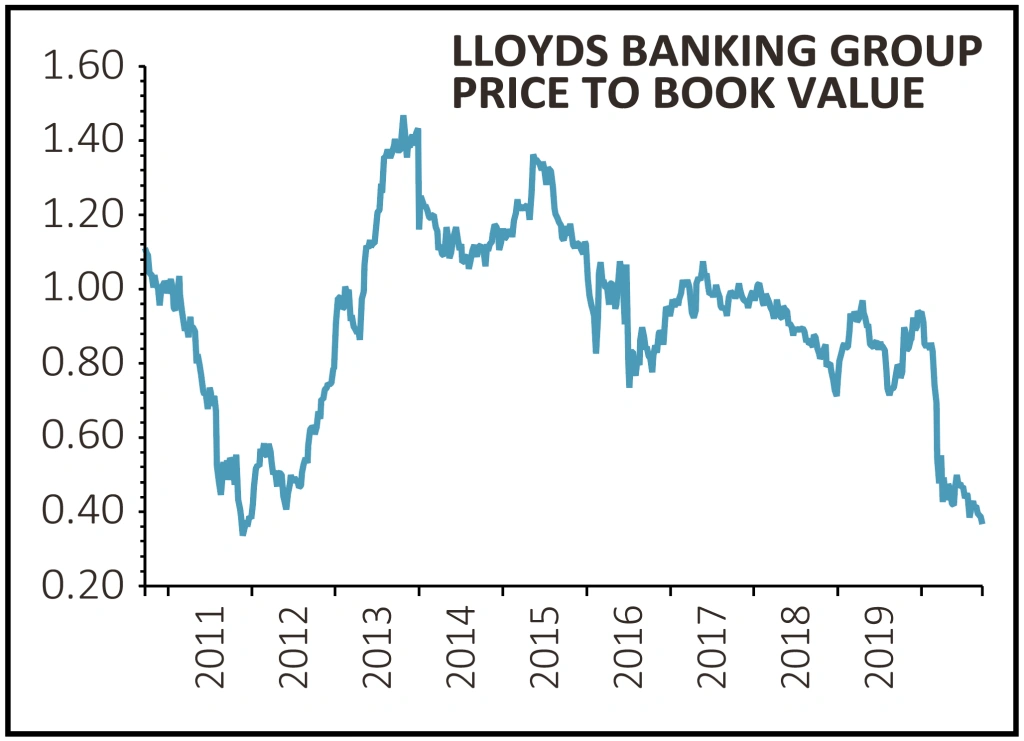

Stocks on the ‘losers list’ like Lloyds (LLOY) and Tesco (TSCO) are widely held by retail investors. A hypothetical investment of £10,000 a decade ago in the worst offender NatWest (NWG) would be worth less than £3,000 today and that’s without even accounting for the impact of inflation.

WHY HAVE SOME SHAREHOLDERS BEEN PATIENT?

Such poor returns raise the question of why people are putting up with such lousy performance for so long and whether they will continue to demonstrate such high levels of patience.

While several of these stocks will have paid dividends at a fairly generous yield over the period, perhaps in part explaining their appeal to investors, if held for the full 10 years this income would have been swallowed up by capital losses – to a significant extent in some cases.

Looking at the list, it is clearly dominated by banks and supermarkets. It is a little over 13 years since the run on Northern Rock which demonstrated for Britons the seriousness of the credit crunch. There would have been hopes that the banks could have repaired the damage from that crash by now but despite considerable effort and resources they have been unable to enjoy a sustained recovery.

This is linked to several factors: the persistence of ultra-low interest rates as central banks have looked to prop up the economy, scandals of their own making like the PPI debacle, an uneven political and economic backdrop, and most recently the impact of Covid-19.

The latter saw the regulator step in to prevent the banks from doing one of the things that probably helped them hang on to any long-suffering fans – pay dividends.

The financial crisis revealed just how central the banks were to the entire underpinning of the economy and society so this almost guarantees they will face particularly tough regulation.

BANKS ARE CHEAP

Given all of this, why would you even consider investing in a bank? The main answer is that they are cheap.

Berenberg analyst Peter Richardson says: ‘Low levels of default and delinquency, due to government support schemes and forbearance, mean that uncertainty about how the current economic stress will translate into realised losses remains high.’

If the banks’ performance is easy to understand then the not-quite-so terrible but still fairly awful returns on offer from the groceries sector are more of a puzzle.

It tells a story of individual failings, notably Tesco’s (TSCO) damaging accounting scandal and arguable move away from the basics in the early 2010s, and strategic setbacks for Sainsbury’s (SBRY) including the collapse of a merger with Asda thanks to the intervention of the competition authorities.

The established supermarkets have also faced disruption in several key areas – the rise of the German discounters Aldi and Lidl, a shift away from big superstores towards convenience outlets and the shift of the weekly shop online, which has brought with it opportunities but also considerable costs.

IMPROVED PROSPECTS FOR SUPERMARKETS

Shore Capital analyst Clive Black is optimistic on the prospects for the sector. He says: ‘There is greater scope for positive operational gearing, to help fund pricing activity, other drags on earnings are easing, such as the online channel turning positive from a profit perspective...

‘More structurally, the annual rate of industry space growth is easing whilst the annual value of industry sales grows, so building sales and cash flow densities per square foot.

‘Therefore, after a sustained period to 2016 of declining sales densities, capital returns and asset impairments, we see an industry with rising densities, building returns and greater investor interest in supermarket assets.’

WHAT ABOUT THE OTHERS?

The remaining four names on our list which fall into neither the bank or supermarket category have endured a mix of internal issues and external factors.

While some people, including fund manager Nick Train, think publishing group Pearson (PSON) can be an eventual beneficiary of a shift to digital learning, to date this has been bad news for the business as it has seen high margin sales of expensive academic textbooks collapse.

Miner Anglo American (AAL) has been a victim of commodity price volatility and its own operational mistakes, while aircraft engine maker Rolls-Royce (RR.) has endured problems with its kit, poor cash flow performance and more recently the devastating hit to its key customer base in the aviation sector from Covid-19. Asset manager Man Group (EMG) hasn’t been helped by patchy performance for its funds.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.