Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

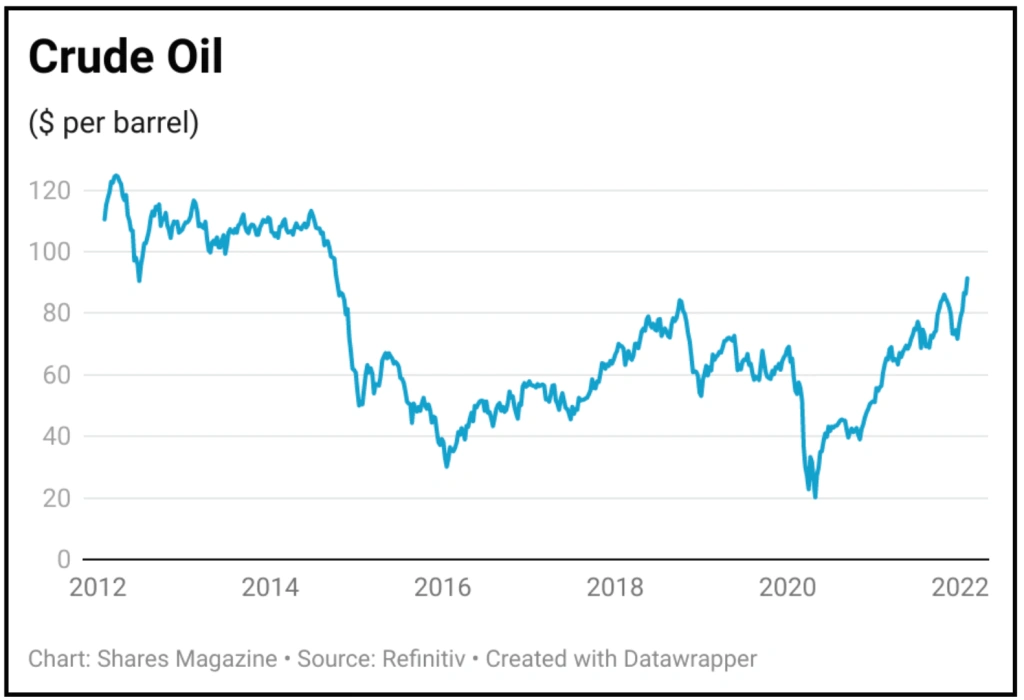

magazineOil services firms warn as crude hits $90 per barrel

The stresses and strains of oil market volatility and a Brent crude price at a multi-year high of $90 per barrel are becoming apparent.

With the potential for conflict in commodities-rich Ukraine involving major producer Russia, many observers are expecting oil prices to hit triple digits sooner rather than later.

While ostensibly this is good news for oil and gas companies, firms which offer services to the sector are under severe pressure with Italian group Saipem and seismic survey specialist PGS recently serving up major profit warnings.

The oil services sector is being affected by both global supply chain pressures and the typical lag between a recovery in the oil and gas market and an increase in spending by commodity producers.

While oil prices are high now, they hit rock bottom in the immediate aftermath of the pandemic, leading energy firms to slash their budgets. It takes time for that money to come back, and the picture is further complicated by the larger integrated players like the UK’s BP (BP.) and Shell (SHEL) shifting investment into renewables as part of the energy transition.

The surge in oil prices is likely to have a more immediate impact on the cost of fuel, with Air China warning on profit partially because of the rising price of jet fuel.

While many airlines hedge their exposure in this area, higher fuel costs could help dilute any summer recovery for the industry.

In this context it’s no surprise that a higher oil price is seen as a tax on global economic growth, with the surge higher in the market a key contributor to current inflationary pressures too.

Bank of America analysts think there could be a further spike higher in the near term before pressures on supply start to ease: ‘To get to where we are today, the market has drawn OPEC spare capacity down by 2.5 million barrels a day in the past year to just about 3 million barrels per day (excluding Iran).

‘As summer travel peaks, spare capacity could fall an additional one to two million barrels per day, causing oil prices to spike higher. However, rising GCC OPEC capacity, a potential return of Iranian barrels, and non-OPEC supply growth should help ease oil balances over the medium term.’

Once oil prices reach a certain level, demand starts to be eroded but Morgan Stanley now believes this threshold is higher than the $90 per barrel it previously estimated, and this informs its decision to follow other investment banks in lifting its forecast for oil to $100 per barrel.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

- Recovery or takeover likely to drive DotDigital shares higher

- Hipgnosis shares hit 11-month low on Neil Young / Spotify spat

- Revolution Beauty can still dazzle despite tough start on the market

- Play the momentum in high quality Bloomsbury Publishing

- Why Hargreaves is still a buy after rising 61% in less than a year

- Investors searching for real assets should snap up Industrials REIT

- A great way to play brighter prospects for Chinese shares