Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePlotting our position in the market cycle and what comes next

It is tempting to say the recent tumultuous sell-off in global markets is different to previous pullbacks.

This is on the basis it was triggered by investors reacting to the risk of the US Federal Reserve and other central banks raising interest rates, rather than a global pandemic or fundamental problem in the banking system or the housing market as in previous market downturns.

John Templeton, founder of the asset management group of the same name and a master investor who had the ability to judge market sentiment better than most, would probably argue it’s never different.

The fact is the bull market in global asset prices from the post-financial crisis low was already long in the tooth when the pandemic struck, and due to its specific nature the pandemic actually reinforced the upside momentum in a select group of stocks propelling indices such as the Nasdaq into ‘bubble’ territory.

How the stock market relates to the economic cycle

Both stock markets and the wider economy fluctuate between peaks and troughs. Economies will see periods of both growth in GDP and contraction (recessions). It’s a similar story in the stock market but, because investors are forward looking with valuations reflecting expected future earnings, the market cycle is often ahead of the economic cycle. As a consequence stock markets often turn upwards when economies are still mired in recession.

BUBBLE OR SUPERBUBBLE?

In his recent letter to investors, Jeremy Grantham, co-founder of Boston-based asset manager GMO, described US stocks as having entered a ‘superbubble’ comparable only to those of 1929 and 2000.

Grantham argues that two of the defining features of superbubbles are an acceleration in the rate of price increases to two or three times the average speed of the preceding bull market, together with a narrowing of market leadership which coincides with big drops in speculative stocks, both of which are consistent with what we have seen of late.

Historically, he concludes, superbubbles eventually correct ‘all the way back to trend with much greater and longer pain than average’. GMO is advising its clients to avoid US equities and buy international value stocks with a particular focus on Japan.

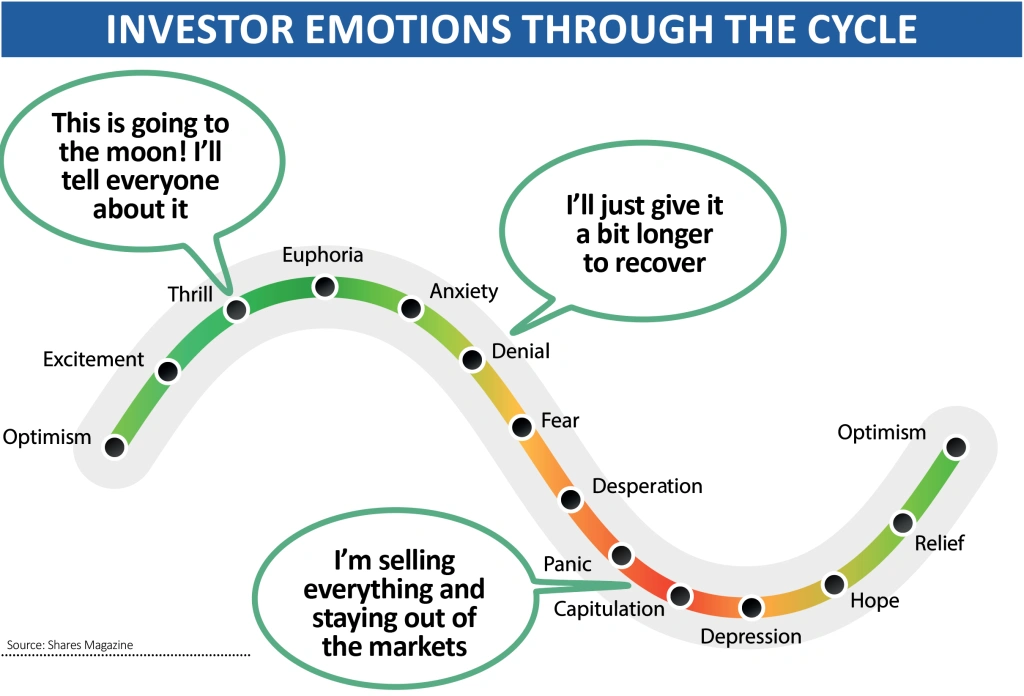

THE SENTIMENT CURVE

It was Templeton who famously coined the phrase ‘bull markets are born on pessimism, grow on scepticism, mature on optimism and die on euphoria’. We have expanded on Templeton’s basic sentiment ‘curve’ with our own version in this article.

In attempting to judge where we are in the cycle, it would seem a fair bet that we are past the period of euphoria for stocks or any other risk asset for that matter.

It seems highly unlikely from where we are standing that markets will rush back to their old highs, or even dawdle their way back there over the course of 2022.

However, neither does it feel as though we are anywhere near entering the fear or panic stages. The working assumption seems to be that the Federal Reserve just wants to tame inflation rather than kill it altogether, so markets should be able to live with a brief period of rising rates.

A ‘NEW NORMAL’

If the Fed were to tighten monetary conditions too quickly or by too much it would risk a US – and by extension a global – slowdown, which is not its aim.

Moreover, most of the debt built up over the period of easy monetary conditions is in the hands of governments, not individuals or companies, and the Fed, like every other central bank, needs a degree of inflation in order to erode the value of its debt.

Also, central banks don’t want to have to pay sky-high interest on any new debt they may need to issue so they need to perform a fine balancing act to convince markets they are being tough on inflation, on the one hand, while on the other hand not being so tough as to derail the economy.

Potentially the best outcome would be for markets to trade in a range until investors have lowered their expectations and the froth has been blown off share prices, dampening speculation and what are sometimes described ‘animal spirits’.

This would certainly be preferable to more sharp falls in asset prices, which in turn risk creating a negative feedback loop with consumer confidence and resulting in a pronounced economic downturn.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

- Recovery or takeover likely to drive DotDigital shares higher

- Hipgnosis shares hit 11-month low on Neil Young / Spotify spat

- Revolution Beauty can still dazzle despite tough start on the market

- Play the momentum in high quality Bloomsbury Publishing

- Why Hargreaves is still a buy after rising 61% in less than a year

- Investors searching for real assets should snap up Industrials REIT

- A great way to play brighter prospects for Chinese shares