Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStill waiting for the big airline comeback

There’s little doubt that investors see 2022 as being the year that travel gets its mojo back, at least when it comes to Europe.

While US airlines made decent headway in 2021 largely thanks to continued demand for domestic flights, European airlines have been hampered by complex travel restrictions which seemed to chop and change with little rhyme or reason.

Omicron’s later arrival to US shores coupled with investors’ general yips over impending fiscal tightening have sent US airline stocks into retreat at a time when European Airlines are beginning to look a lot more attractive.

European airline bosses have been falling over themselves to shout about the increase in demand, particularly from UK consumers desperate for a little summer sun to soak away the stress of the last couple of years.

Capacity has been upped for those peak holiday months to those popular destinations that offer cheap and cheerful options for consumers still feeling a little cautious about jetting off anywhere too exotic.

Price will be the X-factor and there’s uncertainty about exactly how that will play out. In its latest update Ryanair said it expects its pricing power to increase eventually as capacity on sought-after destinations is stretched, but Wizz Air (WIZZ) boss József Váradi isn’t so sure. He thinks there will be a glut of provision to popular resorts which will force rivals to keep pricing keen.

And that’s where the skies look a little less blue. Airlines have high fixed costs and although most have continued to hedge their fuel costs each empty seat weighs on profitability.

It doesn’t matter how many bookings are made, how many flights take off or to how many destinations, it matters how full those planes are and how much each passenger was prepared to fork out for their seat.

Looking at EasyJet’s (EZJ) latest trading update the carrier had been making pretty good headway until Omicron dented confidence just as the Christmas holiday rush should have got underway.

While the load factor (percentage of available seating that has been filled with passengers) had tipped over the 80% mark in both October and November it plummeted to 67% in December. As revenue rose so did costs and the load factor meant the sums still didn’t add up to a profit.

Getting bums on seats will be crucial for all carriers and already the ticket offers are circling. With consumers booking later than they habitually would there is a question as to who will blink

first. Are the deals now the best they’re going to be or will those risking a last-minute break emerge the victor?

For the low-cost summer sun providers 2022 does look set to deliver some better memories than the last couple of years did, indeed TUI’s (TUI) UK managing director Andrew Flintham has said that he expects summer bookings to be back to pre-pandemic levels.

Going forward, if variants don’t cause any more upset and inflation doesn’t keep too tight a grip on the consumer purse then businesses like Jet2 (JET2:AIM) and EasyJet are in decent fettle, the latter has just begun hunting for 1,000 new pilots to bolster its roster as normal service is resumed.

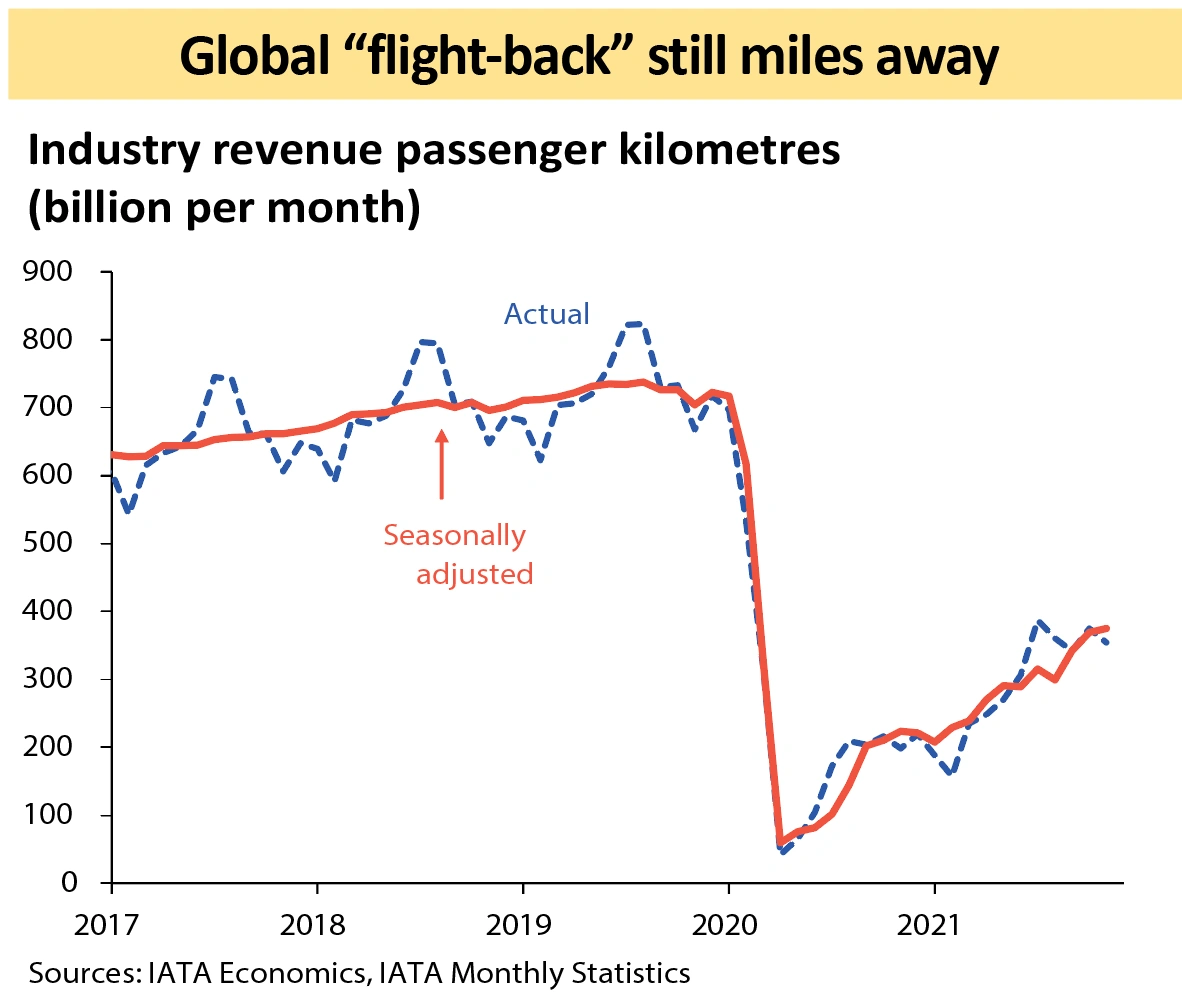

But what of those long-haul carriers like British Airways? Globally, air travel is a very long way off the levels seen in 2019 and with many countries still requiring testing, confidence will be slower to return.

Add in the expectation that business travel will never get back to where it was because of environmental targets and the surge in the popularity of video conferencing, and there’s a fare bit of turbulence ahead. To that end International Consolidated Airlines (IAG) has already begun plotting. Not only is the British Airways owner embarking on a return trip into low-cost territory but it’s boosting its transatlantic credentials too.

A tie-up with American Airlines to co-locate at a new, improved JFK Terminal 8 from next December will help create onward opportunities as well as making the Big Apple a more enjoyable stop. Making those premium journeys worth the price tag shows that International Consolidated Airlines understands its true unique selling points but giving everyone a smoother experience through those airport checks will be a big lure.

Planning and development can’t be put on hold. It’s no accident many carriers have been on an aircraft shopping spree, scenting opportunity to grow. As carriers recover, aircraft manufacturers and the myriad other connected businesses will recover too.

The fact the aviation sector remains one of the few industries still to bounce back from Covid makes it interesting from an investment perspective. At some point, earnings are going to improve. It’s a question of when, not if.

Unfortunately, the industry continues to be tested to its limits, and high oil prices and a highly competitive market mean the return to profit is not going to be a smooth ride for the sector.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

- Recovery or takeover likely to drive DotDigital shares higher

- Hipgnosis shares hit 11-month low on Neil Young / Spotify spat

- Revolution Beauty can still dazzle despite tough start on the market

- Play the momentum in high quality Bloomsbury Publishing

- Why Hargreaves is still a buy after rising 61% in less than a year

- Investors searching for real assets should snap up Industrials REIT

- A great way to play brighter prospects for Chinese shares