Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Investing is not about selecting just any stock or fund at random in the hope of getting the best returns. You need to pick your investments wisely and consider how you might feel about losing money if something goes wrong.

It all comes down to making a plan that suits your temperament and lifestyle while giving yourself the best chance of staying the course and not panicking or swerving off course. If you are the type to get anxious and lose sleep after reading about negative market headlines hitting the value of your investments, you might be better off with a portfolio that moves around less and is more stable.

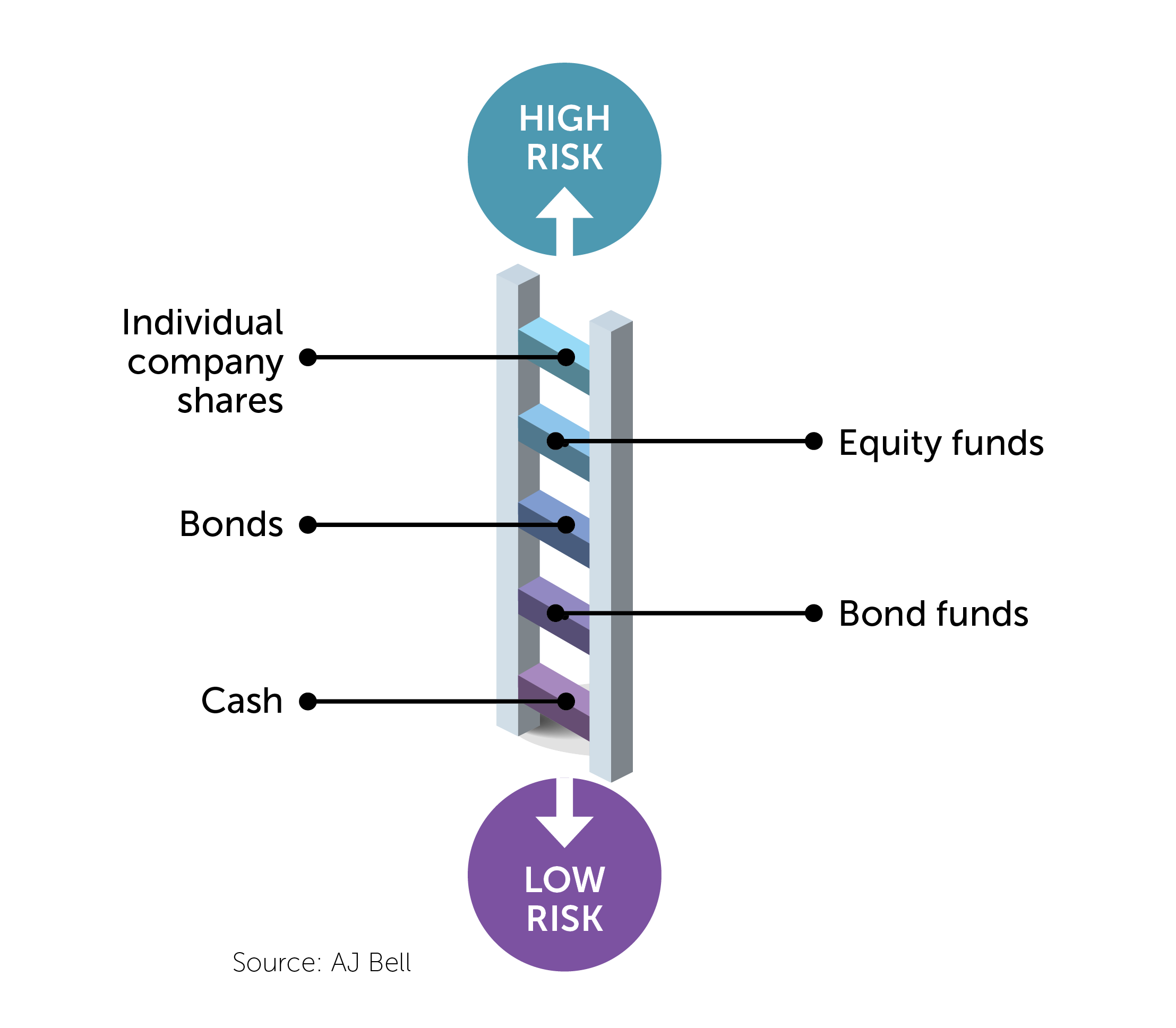

It’s worth thinking about different investment types as being rungs on a ladder. At the bottom end of the ladder is the lowest risk investment. The risks, but also potentially the returns, increase as you climb the ladder.

If you really can’t bear the thought of chalking up a loss, it might suggest that you don’t have a large appetite for risk. Therefore, you would need to consider investing in lower-risk areas. The downside of which is you might not meet your financial goals or will need to increase your future contributions to reflect the typically lower returns from less risky options. Our ISA calculator can help you work out these details out by factoring in your timeframe, expected return and the amount you expect to put in.

Using funds rather than investing in standalone investments can reduce risk because they allow you to diversify. By not putting all your eggs in one basket you are not as exposed to individual losses as you would be if you’re relying on just a handful of investments for your returns.

Read on and we’ll give you some examples of higher and lower risk fund options – all drawn either from AJ Bell’s own fund range or our expert-selected Favourite funds list.

What are the lower risk options?

The easiest way to achieve stable returns is to stay in cash. Cash deposits at UK banks are protected up to £120,000 per institution by the Financial Services Compensation Scheme, so effectively any cash you hold this way is guaranteed.

However, the downside is the historically lower rates of return on offer, which often fall short of inflation. This means that the purchasing power of your cash falls over time. For this reason, it’s unlikely that keeping all our money in cash will, for many of us, meet our long-term financial goals.

A money market fund is a lower-risk investment vehicle that holds short-term debt issued by governments and companies. These funds aim to create a slightly better return than you’d get on cash in the bank. BlackRock ICS Sterling Liquidity Premier Inc invests in short-term UK government debt, pays out income monthly and has an historic yield (based on what it paid out in the last year) of 4.15%. Ongoing charges on this fund are 0.1%.

Another way of reducing volatility but getting a better return than cash is to put some money into government bonds – known as gilts in the UK. This type of investment has returned more than cash over the long run but less than shares.

A bond is like an ‘IOU’ – a government or company borrows money from an investor by issuing bonds in exchange for cash. They then pay a fixed amount of interest over a specified period. At maturity the investor cashes in the bond for its original face value (also known as ‘par’). Corporate bonds are seen as higher risk than government bonds because, in most cases, there is a greater chance of a company defaulting on its debts.

You often see people discuss bonds in terms of their yields. This can be confusing given that stocks are discussed in terms of share prices. You just need to understand that bond yields move in the opposite direction to the price. So, when someone says a bond’s yield is falling, the price is rising. Bonds also generally do well when equities fall, because they are considered safer.

A relevant exchange-traded fund or ETF (a type of fund which trades on the stock market) is Amundi Core UK Government Bond ETF Dist which has ongoing charges of 0.05%. It is also possible to invest in gilts directly through an ISA.

Additionally, there are funds which prioritise preserving your money over other goals. An example is Trojan Fund X Acc which has been managed by Sebastian Lyon for nearly 25 years (he now co-manages the fund with Charlotte Yonge) and holds a mixture of stocks and bonds. It has ongoing charges of 0.86%.

Moving up the risk scale but retaining balance

For many people, having a mix of stocks, bonds and cash will be a sensible way of managing their finances over the long term. The precise mix will depend on individual financial circumstances, age and temperament.

As its name suggests AJ Bell Balanced I Acc takes a balanced approach with 55% of its investments in stocks and shares and 34% in bonds with the remainder in cash, property and other alternative asset classes.

As discussed corporate bonds are slightly further up the risk scale than government bonds but still seen as safer than shares. That’s because bondholders are ahead of shareholders in the list of creditors should a company go bust.

A diversified option which has the flexibility to invest in lots of different types of bonds with the aim of achieving the best possible return is Artemis Strategic Bond Acc, which has ongoing charges of 0.59%. There is also an ‘Inc’ version of this fund which pays out any income the fund receives from its holdings.

What about taking on greater risk with the aim of greater reward?

Investing all your money in shares is considered an ‘aggressive’ stance and is probably best suited to younger people with longer investment horizons to ride out ups and downs in the market.

Although the long-term return from UK shares has averaged around 8% a year, along the way there have been some prolonged periods of negative returns. That’s why it is advisable to invest for a minimum of five years. Another tip is that investing little and often can help smooth out volatility [link to regular investing here].

When it comes to investing in stocks you don’t need to restrict yourself to the UK market. Global funds can invest in what they perceive to be the most attractive opportunities around the world. Dodge & Cox Worldwide Global Stock Fund, for example, looks for companies with strong and sustainable earnings and cash generation with valuations lower than the wider market. Ongoing charges are 0.63%.

Alternatively, the AJ Bell Adventurous Fund has nearly 90% of its investments in shares from around the world with some modest exposure to bonds and cash. Its annual charge is 0.31%.

Tom Sieber: Content Editor

Tom Sieber is AJ Bell's Content Editor. He was previously the Editor of Shares Magazine. He has been with the business since 2012.

Tom is a regular contributor to the AJ Bell Money & Markets...