Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

The combination of Liberation Day’s tariffs, wars in the Middle East and Eastern Europe, worries over the long-term impact of Artificial Intelligence upon jobs, galloping government debts and stretched budgets, and active debate about stock market bubbles does not look like a favourable one for investors. However, many will look back upon 2025 with contentment.

Equities, bonds and commodities all provided positive returns, to varying degrees, and hopes for interest rate cuts, cooling inflation and steady economic growth give grounds for optimism in 2026, although ructions in the cryptocurrency arena and the ongoing surges in gold and silver may yet be harbingers of heightened volatility in the year ahead.

| Capital return in sterling terms | ||||

|---|---|---|---|---|

| 2024 | 2025* | |||

| Bitcoin | 125.9% | Silver | 89.6% | |

| Natural Gas | 47.1% | Gold | 52.5% | |

| Gold | 29.4% | Natural Gas | 27.3% | |

| Silver | 23.7% | Emerging Market equities | 20.2% | |

| Commodities | 20.5% | Global equities | 12.6% | |

| Global equities | 17.5% | Global corporate bonds | 4.1% | |

| Global high yield bonds | 10.4% | Global high yield bonds | 1.8% | |

| US dollar | 9.0% | Global government bonds | 1.3% | |

| Emerging market equities | 6.9% | Commodities | 0.2% | |

| Global corporate bonds | 2.6% | Bitcoin | (12.7%) | |

| Global government bonds | (1.1%) | US dollar | (13.4%) | |

| Brent crude oil | (2.1%) | Brent crude oil | (20.1%) | |

Source: LSEG Refinitiv data. *2025 to close on 1 December

The dollar suffered from Donald Trump’s tendency to announce policy on the hoof, and via social media, as investors looked to diversify their exposure after a barnstorming run in US equities valuations looking stretched by historic standards.

This desire to rebalance portfolios helped other arenas, where valuations were closer to past norms, notably Europe, Japan, emerging markets and even the UK.

European equities managed to turn the war in Ukraine into a positive story, as EU and NATO members focused afresh on national security, in the form of defence spending but also improved infrastructure and energy and mineral supply. Germany’s move to lift its self-imposed debt brake gave European equities a welcome boost.

Dollar weakness also boosted commodities, as well as emerging equities, but the strength in gold and silver, and year-end weakness in cryptocurrencies, struck a discordant note in some ways as 2025 concluded. Both trends suggested that someone, somewhere was expecting trouble in 2026.

| Capital return in sterling terms | ||||

|---|---|---|---|---|

| 2024 | 2025* | |||

| NASDAQ | 30.9% | KOSPI | 54.7% | |

| S&P 500 | 25.5% | Bovespa | 44.0% | |

| Hang Seng | 20.4% | DAX | 25.8% | |

| DAX | 13.4% | Hang Seng | 22.6% | |

| Shanghai Composite | 11.4% | Stoxx Europe 600 | 20.3% | |

| TSX 60 | 9.4% | TSX 60 | 19.8% | |

| Nikkei 225 | 8.9% | FTSE 100 | 18.7% | |

| BSE Sensex | 7.0% | Nikkei 225 | 18.3% | |

| FTSE 100 | 5.7% | SSMI | 18.2% | |

| Stoxx Europe 600 | 1.1% | CAC 40 | 16.4% | |

| SSMI | (1.5%) | NASDAQ | 13.9% | |

| CAC 40 | (6.6%) | Shanghai Composite | 13.4% | |

| KOSPI | (19.5%) | S&P 500 | 9.5% | |

| Bovespa | (28.3%) | BSE Sensex | (1.0%) | |

Source: LSEG Refinitiv data. *2025 to close on 1 December

Any desire for more defensive exposure could help demand for bonds. Fixed income rallied in 2025 after a poor 2024, in one of many examples where the dogs of one year became the darling of the next.

Over 120 global interest rate cuts helped the fixed income asset class, and hopes for cooling inflation and fears over global growth, should tariffs finally start to have an impact, could give sovereign bonds a lift in 2026, although large government deficits mean there will be no shortage of supply of fresh paper to buy in the coming year, especially in the UK, France, US and Japan.

Any worries over the economy could cool investors’ ardour for investment grade and high yield corporate bonds, where spreads over government issues are looking skinny compared to historic averages, to suggest portfolio builders may be receiving less compensation than is ideal in return for taking additional risk.

It is worth thinking about what happened in 2025 and why, and whether five trends can continue in 2026 and beyond.

1. Tariff and trade worries faded away

Donald Trump’s ‘Liberation Day’ announcement on 2 April caused panic, but not for long.

Global equity markets motored higher as the US president delayed the imposition of tariffs until August, struck individual deals with certain countries and then backed away further in the autumn with a series of agreements with Caribbean and Latin American food exporters, as American voters let him know what they thought of rising food prices and what the real rate of inflation might be for them.

As a result, equity investors seem comfortable with the view that the hit to growth, global trade flows and corporate margins will be modest at best, although it remains to be seen whether companies start to pass on any latent price increases in the coming year.

The assertions of Trump and Treasury Secretary Bessent that exporters, not importers and American consumers, will pay are still open to question, and the moves to reduce tariffs on foods where domestic production is insufficient, may be a bit of a giveaway.

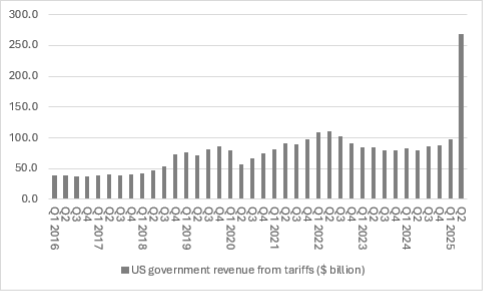

Even though the full range of tariffs did not come into force until summer, the Yale Budget Lab estimated that the effective tariff rate come November was 17.3%, the highest since 1934.

Government revenue from the levies jumped sharply enough to Trump to publicly ponder whether they could fund $2,000 tax cuts for many Americans, although the Supreme Court continues to debate whether the reciprocal tariffs imposed by Trump using the International Emergency Economic Powers Act (IEEPA) are legal or not. Their repeal would take the overall tariff burden down by some eight percentage points, according to the Yale Budget Lab.

If that court case fails to knock down the IEEPA tariffs, it’s still unclear what tariffs may mean for trade, corporate profits and prices in 2026, but markets seem convinced the worst is over. Any unexpected slowdown in growth, margin pressure or stickiness in inflation could therefore be a nasty surprise.

Source: FRED – St. Louis Federal Reserve database

2 Emerging markets roared back

The best individual performing stock markets to date in 2025 are South Korea, Greece, South Africa, Poland and Chile.

Thanks, in the main, to the influence of the US equity market, which now represents some two-thirds of global stock market value, developed markets have beaten their emerging counterparts for the thick end of two decades.

Taiwan and South Korea offer AI exposure through their specialist silicon chip makers, while other emerging arenas offer exposure to commodities, notably Chile and copper.

The prospect of a right-ward swing in Latin American politics is helping sentiment, while the lengthy period of underperformance offers more tempting valuations than those available in the US.

Add in hopes for ongoing fiscal and monetary stimulus in China and Hong Kong, as they fight to overcome the after-effects of a property bust, and emerging markets came roaring back in 2025.

Having come through their own debt crisis in the late 1990s, many emerging markets have lower debt-to-GDP ratios than their developed counterparts. They also, in many cases, acted more quickly to quell inflation at the turn of the decade and thus have more scope for monetary stimulus in the form of interest rate cuts.

Prolonged dollar weakness would be a further bonus, as a soft greenback would lessen the burden of dollar-denominated debt held by emerging nations.

Source: LSEG Refinitiv data

3 Fixed income asset class found itself back in favour

After a fallow 2024, the fixed-income asset class came back into fashion in 2025 as investors reacted to interest rate cuts from central banks and priced in further monetary easing in 2026 for good measure.

That monetary easing, coupled with the view that the peak in inflation was well behind us, prompted investors to reach for the yield on offer.

The absence of any global growth shocks, barring maybe one week in April, also raised the attractiveness of investment grade and high yield corporate bonds, although the dollar’s weakness against the pound chewed up a chunk of the total return offered to UK-based investors by the headline bond market indices.

Further rate cuts could help in 2026, but any unexpected stickiness in inflation would be potentially a challenge across sovereign, investment grade and corporate debt, and any growth shock could leave high yield spreads looking thinner than ideal.

Bond investors continue to watch absolute levels of government borrowing in the developed West with growing concern, and this could yet remain an issue for sovereign bonds, although the nagging suspicion that central bankers could yet reach for zero interest policies and quantitative easing in the event of any economic or financial market upset could counter such concerns.

4. Oil slid lower

Even war in Eastern Europe and the Middle East, sanctions against major producers and the absence of any economic shocks could not help the oil price catch a bid.

Brent crude peaked just north of $80 in January and then ground lower for the rest of the year, hampered by OPEC+ production increases.

Even a less bearish stance from the International Energy Administration did not help, as the IEA acknowledged its forecast of peak oil demand by 2030 could prove wrong if current consumption trends continued unabated and countries did not make greater efforts to meet their Paris commitments.

Oil’s slide left investors to address the question of whether hydrocarbon assets would be left as stranded assets, with a much-reduced value compared to current expectations. That persuaded investors to shun hydrocarbon producers, despite their generous dividends and share buybacks.

The stock market value of the S&P Global 1200 Energy sector is just 3.3% of that of the overall S&P Global 1200 index. That is not far from 2020’s Covid-and-lockdown-inspired low of 2.5% in 2020 and well below the long-term average of 7.7%, let alone 2007’s peak of 13.8%.

Source: LSEG Refinitiv data

This lack of interest reflects the view that renewables will take the lead in energy provision, and the risk that governments will continue to apply lofty tax rates if oil and gas producers’ profits stay higher for longer than expected.

The oil majors are getting the message, as they restrain capital expenditure budgets. Should oil demand surprise on the upside, as the IEA suggests it might, supply of hydrocarbons may only grow slowly, and that it will take time to bring on new fields, even if demand for energy worldwide continues to increase as the globe grapples with how best to manage the transition toward renewables.

This could yet lead to more interest in hydrocarbon assets, and higher commodity prices, especially if sticky inflation or ongoing debt accumulation by Western governments persuade investors to trust ‘hard’ assets more than ‘paper promises,’ such as cash and bonds.

5. Gold and silver shone

Certain investors may seek out precious metals as protection from inflation, thanks to how that strategy worked in the 1970s.

Some might look at gold and silver in fear of currency debasement, should central banks and governments rely on financial repression in the form of zero-interest-rate policies and quantitative easing as a way out of the debt tangle in which they find themselves.

Others may be seeking a haven during a time of geopolitical uncertainty, to which some might argue that the White House’s foreign policy is contributing, and after a big run in many financial asset classes, despite, or perhaps thanks to, the combination, in some cases, of leverage, complexity and opacity.

Interest in silver and gold could cool if equity markets’ dream scenario of cooler inflation, steady economic growth and lower interest rates pans out as hoped and central banks prove they are on top of the situation.

Equally, any diversion from that path, and any sense that central banks are not fully in control, or that they may chance their arm with inflation as they keep interest rates low to try and help governments manage their debts and interest bills, could yet give silver and gold a further boost.

Russ Mould: Investment Director

Russ Mould is AJ Bell's Investment Director. He has a Master's degree in Modern History from the University of Oxford and more than 30 years' experience of the capital markets.

He started out at Scottish...