Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Dividends might be classed as income, but if you reinvest them, they can make a valuable contribution to your overall investment growth over the long term. This article looks at the impact of dividend reinvestment and what you might need to watch out for.

The main potential benefit is that you can harness the power of compounding returns. Put simply, compounding is where any returns are applied not just to your original investment, but also to the returns you’ve already earned. This can multiply your investment over time, assuming returns are positive.

For example, let’s assume you bought shares in ABC plc for £100, and you received a dividend of £5 in year one, along with a 6% increase in the share price. In year two, the share price jumps by 8% and the dividend is £5 again. At the end of year one, your investment could be worth £111 if you reinvested the dividend. That’s growth of 6% on the £100 plus the £5 dividend. This full £111 could then grow by 8% in the second year, meaning you earnt growth on your original £100, but also the reinvested dividend.

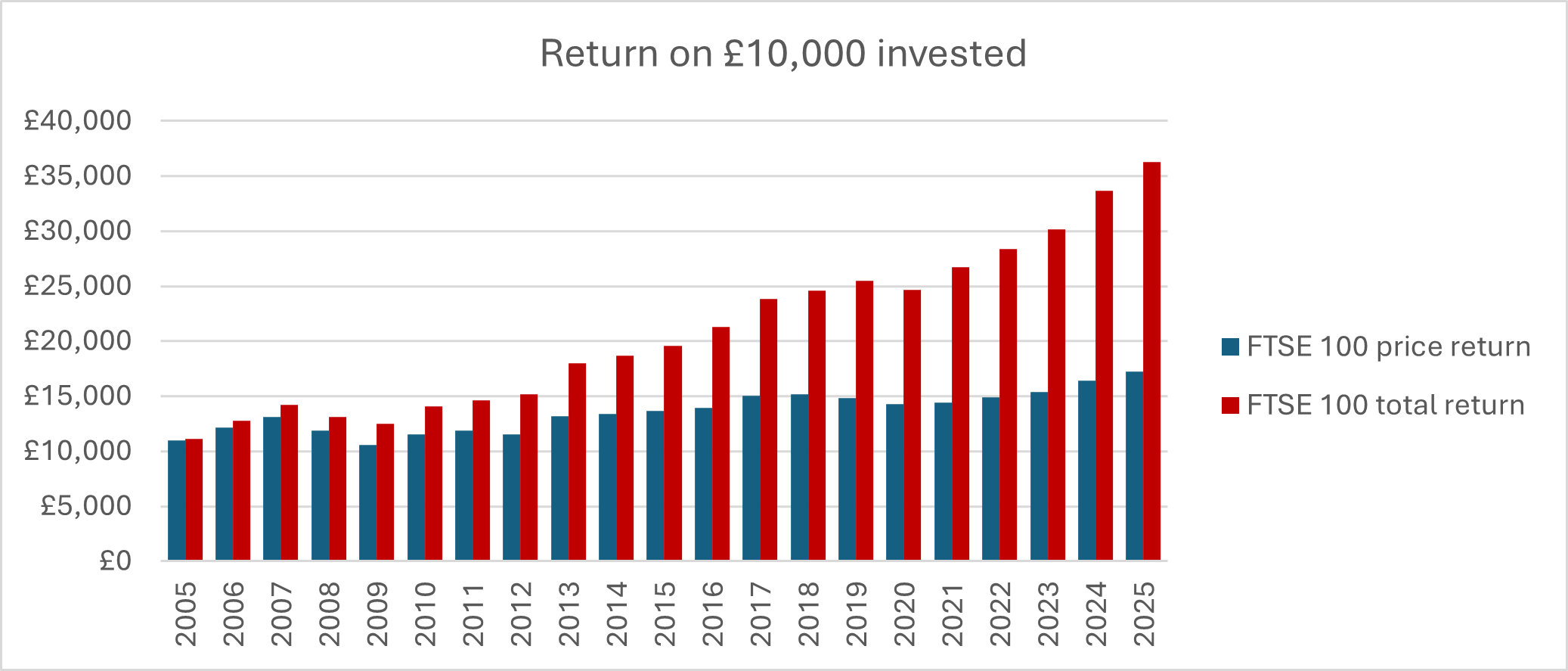

We can also look at how this could have played out for equity investors over the last 20 years. Using the FTSE 100 share index, the graph below shows the difference in the price return – the change in the value of the index each year – versus the total return, including dividends.

Source: Morningstar to 30 June 2025

If you’d invested £10,000 on 30 June 2005 and left it alone, the investment would have grown to £17,134 twenty years later – an annualised return of 2.73%. You’d have received cash payouts along the way too, but if these dividends had been reinvested, you’d expect to be sitting on £38,079 – an annualised return of 6.65%, more than double the performance of the price return alone. We’ve not factored in inflation or charges to this comparison, but it clearly shows the power of compound returns over the long term.

How to reinvest your dividends

Like the sound of compounding returns? If you don’t need the cash payouts, then you can arrange for them to reinvested without you having to lift a finger.

- Shares

Most providers offer the option to automatically reinvest the dividends from your investments. At AJ Bell our dividend reinvestment service applies to UK listed shares (including ETFs and investment trusts) that are quoted in pounds. It costs 1% of the value of the dividend reinvested, subject to a minimum of £1.50 and a maximum cap of £5 per trade.

Keep in mind that this process happens automatically if selected – you won’t be able to choose the purchase price for the extra shares bought with the dividend reinvestment.

- Funds

Most investment funds usually have at least two types of shares or units that you buy – accumulation (Acc) or income (Inc). Accumulation units or shares reinvest the fund’s income generated by its portfolio, while income units pay it out as cash. This usually means that the price of accumulation units or shares will rise over time as more income is received and reinvested. If you’re looking to reinvest any income the fund receives, you should consider choosing accumulation units.

What else do I need to consider?

As well as keeping an eye on reinvesting costs, you’ll need to consider tax on investments you hold outside of an ISA or pension, for example in a Dealing account. Income and gains are still taxable – this will include payments received and reinvested by accumulation funds – even though you’re not receiving them as cash.

Providers like AJ Bell will send you a tax summary of the income and gains you’ve received from non-ISA or pension each year, to help you check whether you’ve got tax to declare and pay to HMRC.

Charlene Young: Senior Pensions and Savings Expert

Charlene Young is AJ Bell’s Senior Pensions and Savings Expert. She joined AJ Bell in 2014 from a wealth management firm where she worked with private clients and small businesses as a financial planner.

Charlene...