How fund managers have succeeded in beating the market again

Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

It looks like Donald Trump has done what years of toil and sweat have failed to achieve, namely some measure of outperformance from global active funds.

In the first half of 2025, 51% of active funds in the Global sector outperformed a passive alternative. That’s according to our latest Manager versus Machine report, which analyses over 1,000 funds across seven key Investment Association sectors. This is the first time since we launched the Manager versus Machine report in 2021 that global active managers have registered anywhere near a win rate above 50% against the passive machines, on any of the time frames we look at.

The previous high-water mark for global active fund managers to hang their rather battered hats on came in December 2021, when 40% of them beat a passive alternative over a five-year period.

The percent of active funds outperforming the average passive alternative

| IA Sector | First half of 2025 | 5-year outperformance | 10-year outperformance |

|---|---|---|---|

| Asia Pacific ex Japan | 11% | 19% | 31% |

| Europe ex UK | 31% | 38% | 39% |

| Global | 51% | 16% | 17% |

| Emerging Markets | 41% | 46% | 56% |

| Japan | 68% | 38% | 50% |

| North America | 44% | 20% | 15% |

| UK | 29% | 27% | 31% |

| Total | 42% | 26% | 30% |

Sources: AJ Bell, Morningstar total return in GBP to 30 June 2025

Trump has helped create the conditions for global active funds to outperform through policies which have weakened the dollar and dented confidence in US stocks, at least in the first half of the year. As a result, the US has uncharacteristically lagged other regional stock markets since the beginning of 2025, especially when performance is converted into pounds and pence.

Most global active fund managers are underweight the US compared to their tracker competitors, a position which has been a powerful headwind for many years, but which has put some wind in their sails so far in 2025.

How regional markets have performed in terms of sterling

| Regional Markets | Total return in first half of 2025, in GBP |

|---|---|

| MSCI Europe ex UK | 13.5% |

| FTSE All Share | 9.1% |

| MSCI Emerging Markets | 5.4% |

| TSE TOPIX | 2.9% |

| S&P 500 | -3.1% |

Sources: FE, total return in GBP to 30 June 2025

There has been a parallel disturbance within the US stock market itself, which has helped US equity fund managers outperform to a higher degree than we have seen in previous Manager versus Machine reports. Some of the Magnificent Seven have been a big drag on index fund performance so far this year, which has opened the door for active managers with broader portfolios to score some points against the passive machines. 44% of active US funds outperformed a comparable tracker in the first half of the year, again a record high for this sector since we started compiling the data in 2021.

Active management in the Global and US sectors may have perked up in 2025, but it’s been a dismal year so far for active managers investing in the UK stock market, where only 29% managed to beat the average index tracker. This poor performance can largely be laid at the door of mid and small caps lagging behind the big blue chips of the FTSE 100, combined with the fact active managers tend to be underweight large caps compared to a plain vanilla index tracking fund.

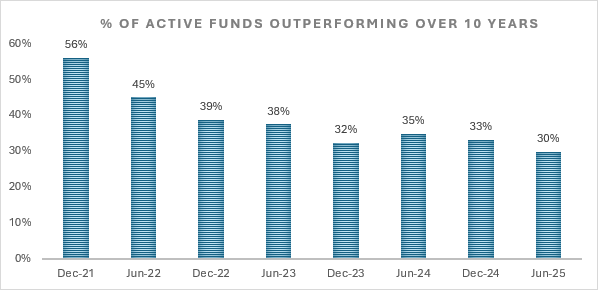

The really bad news for active managers

But here comes the really bad news for active managers: over the last ten years, just 30% of active funds across all seven equity sectors in our analysis have outperformed a passive alternative. This is the worst ten-year reading we have seen since we started compiling Manager versus Machine in 2021. The aggregate figure for all funds is heavily influenced by performance in the Global, North America, and UK fund sectors, as these segments make up almost two thirds of all the active funds analysed over a ten year period. Conditions over the last decade have been bleak in these sectors for active managers, with only 31% outperforming in the UK, 17% in the Global sector and 15% in the US.

It’s unfair to describe this latest low water mark plumbed by active funds as a step change in long term performance, given it’s only a few percentage points shy of what we’ve seen in recent years. However, there’s no doubt that such sustained underperformance, combined with a number of structural fund buying trends, is driving large herds of investors towards the comforting, low-cost simplicity of passive funds.

Source: AJ Bell Manager versus Machine reports 2021 through to 2025

A glimpse into the future of managers versus machines

The poor long-term performance of active funds in the North America and Global sectors sits at odds with their surprisingly perky demeanour so far in 2025. This demonstrates that even if active managers start to turn things around, it’s going to take a considerable period of widespread outperformance to overturn the dominance of index trackers in the long-term numbers.

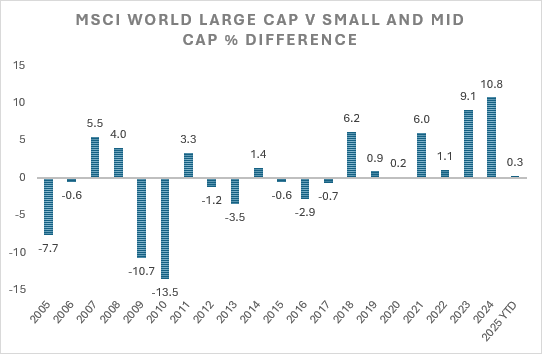

One of the things we have continually highlighted in this report is the impact of large, mid and small cap performance on the fortunes of active managers. Tracker funds will usually be more heavily weighted to large cap stocks than the typical active fund, and active funds will tend to be more overweight medium and smaller companies. When big companies do well compared to their more modestly sized peers, active funds tend to fare poorly, and index trackers rule the roost.

Unfortunately for active managers, in the last twenty years we’ve witnessed small and midcap outperformance give way to the dominance of the big blue chips and that’s particularly the case in the last five years. In the chart below, positive bars signify outperformance of large caps, while bars below the x axis show years of outperformance for small and mid-cap companies.

Sources: AJ Bell, Morningstar, total return to 30th June 2025

A similar trend can be seen in the UK and US stock market. The upshot is it’s still a long uphill battle for active managers to fight back against the passives in terms of ten-year performance, unless we get a spell when mid and small caps post some powerful outperformance of big blue chip companies.

Ultimately this dynamic may well catch up with the passive machines in due course, as the recent market leadership of the biggest stocks in the index falls out of the equation. But for ten year performance figures, that won’t be until the mid 2030s. Given current fund flows into trackers and out of active strategies, the battle between active and passive funds may well have been largely settled by then, in practical terms at least.

Laith Khalaf: Head of Investment Analysis

Laith Khalaf is AJ Bell's Head of Investment Analysis. He joined the company in 2020 and continues to explore the world of personal investing, providing research and analysis to both AJ Bell customers and the...