How the UK’s stock and bond markets react to mid-term prime ministers

Keir Starmer's resignation as leader of the Labour Party and UK prime minister is the latest in a series of events which could see the country welcome its eighth unelected, mid-term prime minister since the launch of the FTSE All-Share in 1962.

After winning the Makerfield by-election Andy Burnham is currently the frontrunner to take on the Number 10 residency, assuming a specific sequence of events take place.

Without the aid of a crystal ball we have no way of knowing for certain who the new UK prime minister will be. But one thing we do have is hindsight and retrospect, in particular, how markets have reacted to this type of passing of the political guard.

Lessons of history

While the news and political chatter around a change of leader is always loud and chaotic, markets have have tended to approach such episodes with a fair degree of indifference, although with some biases.

Stock markets’ preference for a Conservative government still seems clear enough, even if psephologists and historians may both be inclined to argue that investors could have to wait a bit to get another one of those.

Even a cursory glance at British political history suggests that voters do not warm to political parties or governments which seem to put their own internal disputes and self-interest above those of the nation.

Internal division and wrangling wrecked the Tory Party under Peel in the 1840s; the Conservatives at the turn of the 20th century; the Liberals amid Asquith and Lloyd-George’s power struggle of the 1910s; Labour after MacDonald’s National Government of the 1930s; Labour (again) after the Social Democratic Party breakaway of 1981; and the Conservatives (again) in the late 2010s and early 2020s as Brexit and then Covid-19 tested the patience of backbenchers, loyalists and the electorate.

The electorate may give internal politicking the cold shoulder when the ballot box gives them the chance, so financial markets tend to take a more detached view of proceedings. This is primarily because their focus remains on pounds and pence, in the shape of corporate profits, cash flows and dividends, rather than opinion polls.

How the stock and bond markets react to a mid-term prime minister

Since the inception of the FTSE All-Share in 1962, seven prime ministers have taken office mid-way during a parliament, following the departure of their predecessor – James Callaghan and Gordon Brown for Labour, in 1976 and 2007, and John Major, Theresa May, Boris Johnson, Liz Truss and Rishi Sunak for the Conservatives in 1990, 2016, 2019, and 2022 respectively. Only Major and Johnson went on to win an election and thus gain public, rather than just party approval, the former in 1992 and the latter in 2019.

On average, the FTSE All-Share made no immediate progress under the septet during their first 12 months in the hot-seat, rising 3.5% over the first three months of the new PM’s tenure, gaining 3.3% over six months and coming in almost flat over a year (although Liz Truss did not manage to last that long).

On the face of it the gilt market, as benchmarked by the 10-year issue, is more sanguine still. Across those terms in office for which there is data available, the average movement in gilt yields is down, not up.

However, the averages are flattered by the sharp declines seen during Major’s term in office, which encompassed sterling’s ejection from the Exchange Rate Mechanism in autumn 1992. Freed of the obligation to defend the pound, Major, and his appointed chancellor Norman Lamont, were able to slash interest rates, which in turn helped to drag down the benchmark 10-year gilt yield.

This suggests that while political stability is welcome, there are many other factors at work when it comes to how the stock market performs. Over their full term in office all seven encountered hugely different economic circumstances, with the result that the FTSE All-Share provided very different returns.

Callaghan was battling inflation (which drove investors to real assets and equities as it galloped higher) and Major had to confront a recession and the workings of the Exchange Rate Mechanism (where sterling’s departure turned out to be a bit of a blessing). In some ways, Brown got the worst hand of the lot, in the form of the Great Financial Crisis, although Johnson may dispute that, as his administration had to handle Covid-19 and try to finalise the terms of Brexit, something which had confounded his predecessor, May.

Truss is widely seen as being responsible for her own swift demise, thanks to a poorly communicated and potentially unfunded package of tax cuts and deregulation, while Sunak was left to pick up the pieces as the nation’s finances were in absolute tatters by the time he took office.

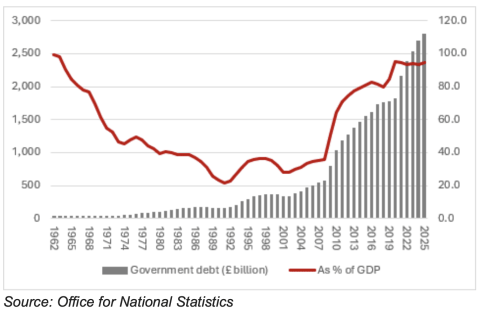

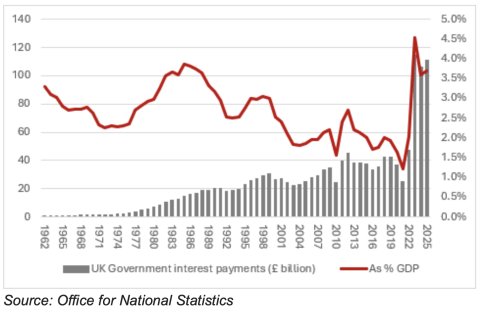

That is an issue that is yet to go away, either, given how the total sovereign debt continues to grow and the interest bill gobbles up more than the annual defence budget.

The economy is therefore one factor – and a successor to Starmer could have an impact here, depending upon their policies for taxation, investment, and regulation – while others are corporate profits and cash flows and the price (or valuation) investors are prepared to pay to access them.

How the stock market reacts to Labour governments

For whatever reason, the UK stock market has tended to do better under Conservative governments than Labour ones since the launch of the FTSE All-Share in 1962. The perception that they are more pro-business, pro-enterprise and anti-state intervention is as good an explanation as any, although it should be noted that equities have still tended to advance under Labour – they have just done so by less, on average.

This can be seen by looking at FTSE All-Share performance data across the 17 general elections and 14 prime ministers seen since 1962.

First, over the full term of the seven governments which followed a Labour election victory the All-Share has risen by an average of 27%, compared to 43% under the eight Conservative administrations.

Second, of the 14 prime ministers to lead the country since the 1964 ballot, four of the best five FTSE All-Share performances by government have come under the Conservatives and four of the five worst under Labour.

Ironically, the FTSE All-Share’s 22.5% gain to date under Starmer ranks him fifth.

That said, the past is no guarantee for the future and even the longest-serving prime ministers of modern times have a relatively limited shelf life compared to many companies.

With a dividend yield of around 3.1%, the FTSE All-Share can be seen as a 28-year duration bond (as this is how long it would take investors to get their money back, assuming no change in dividends or share prices). This shows exactly why shares should be treated as a (very) long-term investment and why the role of short-term politics should not be over-emphasised.

Very few prime ministers have lasted for much more than one full term of office, at least since the inception of the FTSE All-Share in 1962 and even Starmer’s enormous parliamentary majority proved of little use when it comes to implementing his preferred policies and keeping backbenchers sweet.

Russ Mould: Investment Director

Russ Mould is AJ Bell's Investment Director. He has a Master's degree in Modern History from the University of Oxford and more than 30 years' experience of the capital markets.

He started out at Scottish...