The minimum SIPP pension age is currently 55, though the age when you can access your pensions is rising to 57 from 6 April 2028.

If you reach the minimum SIPP withdrawal age and don’t need to access it yet, you can leave your SIPP invested. That way it can keep growing free of tax.

But if you're looking to access your SIPP pension for the first time, SIPP withdrawal rules give you plenty of flexibility. You don’t have to use all your pension fund in one go, so you can choose one option for a SIPP withdrawal now and decide about the rest later.

How can I access my AJ Bell SIPP?

The main options include going into drawdown, or opting for a lump sum or an annuity, which we explain more about below.

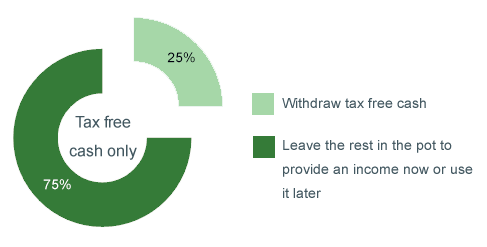

1. Tax-free cash and SIPP drawdown

Take up to 25% of your SIPP as a tax-free lump sum, and leave the rest invested in your SIPP as a drawdown fund. This can give you a flexible income regularly, or as and when you need it.

Example: let’s say you have a SIPP worth £200,000. You could take up to £50,000 tax-free, and move the rest to drawdown where it can stay invested in your SIPP.

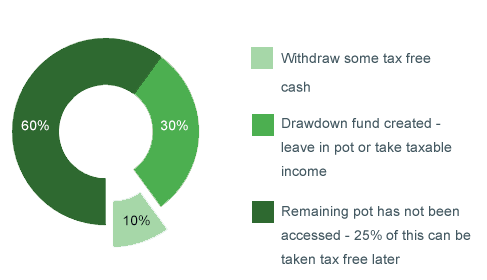

Or, you could convert your pension in stages. This could be a good option if you need some cash but not as much as 25% of the whole fund.

Each time you convert part of your SIPP, you withdraw up to 25% of that amount tax-free, with the other 75% staying invested and moving into drawdown. You can take 25% tax-free cash from what you don’t convert in the future.

Example: of your £200,000 SIPP, you convert £80,000 and withdraw £20,000 as tax-free cash. You create a drawdown fund for the other £60,000, from which you can take a taxable income at any time. The amount you don’t withdraw is also left in the pot to benefit from investment growth and income, and you can take 25% tax-free from it in the future.

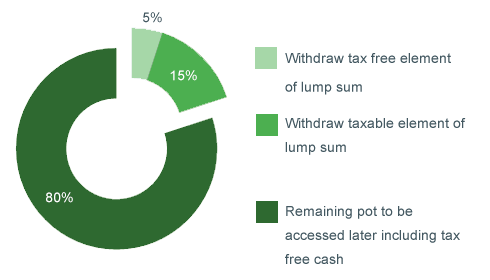

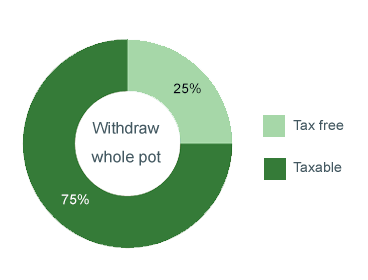

2. Pension lump sums

A single payment where 25% is tax free, and the remaining 75% is taxable. This option lets you take a series of smaller amounts, while leaving the rest invested to access more of in the future. Or you can even withdraw the whole pot.

Smaller amount

Whole pot

Guidance from Pension Wise

Pension Wise is a free, impartial government service that offers guidance to anyone approaching retirement.

If you want to better understand the retirement options available to you, Pension Wise can help.