Approaching or in retirement; here’s your Budget breakdown

Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Related

news

15 December 2025

The best way to get the UK investing is education not Cash ISA cuts3 min readAuthor

Shares Magazine

Rachel Reeves has now delivered her second Budget, but as I’m writing this column, most of the headlines seem more concerned with the lead up to the speech – government leaks and the future of the Office of Budget Responsibility (OBR) – rather than the smorgasbord of policies announced.

So, what changed for people who are approaching or already in retirement? Taken at face value, not a great deal but, as ever, the devil is in the detail.

The main takeaway is that making the most of tax allowances on offer and blending withdrawals in retirement from different tax wrappers will still prove a good strategy for those who want to stay invested. Those who didn’t make decisions based on rumours before the Budget will have reaped the rewards of not reacting to noise.

Here’s a summary of what was (and wasn’t) announced, with retirement in focus.

What happened to pension allowances?

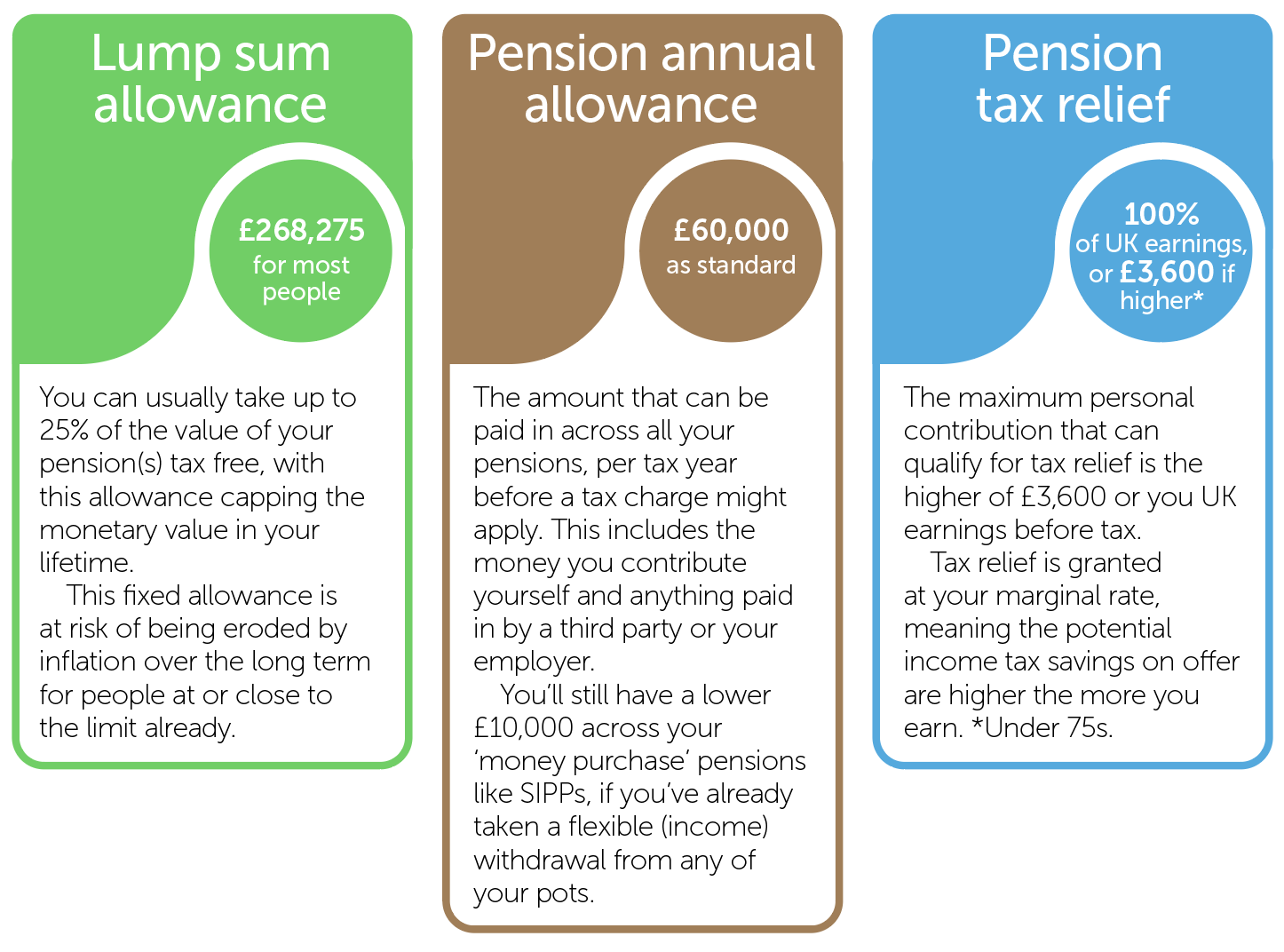

Let’s start with the good news, we didn’t see any changes to the main pension allowances and reliefs, which are summarised on the next page.

A £2,000 cap on the amount of pay that can be exchanged for pension contributions without being subject to National Insurance (NI) is on the cards, but not until April 2029. According to the Society of Pension Professionals, around one in three private sector workers is in a salary sacrifice scheme, but only around one in 10 in the public sector. Some workers and employers might look to make the most of the NI perks on offer while stocks last, and much depends on individual circumstances, but the key point is that the income tax relief rules have not changed.

Will I end up paying income tax in retirement?

Thanks to the triple lock, it was confirmed the full new state pension will rise by 4.8% in April 2026, to around £12,548 a year and set to breach the tax-free personal allowance by April 2027. If your only source of income is the state pension, and you’re pushed over the £12,570 limit, the government has announced that you will not have to pay any income tax that would otherwise be due.

But millions of pensioners already pay income tax with more than one million already caught in the higher rate band of 40%.

Freezing personal tax allowances and thresholds for another three years until April 2031 will inevitably drag more people into paying more tax as incomes and asset values rise over time, including for those close to or in retirement.

What about income tax rates for savings and investments?

Higher income tax rates on savings and investment income will make ISA and pension wrappers look even more attractive as they shield your returns from taxes.

Savings income tax is due to rise by two percentage points from April 2027 across all bands, and the same two percentage point increase will apply to the ordinary and higher rates of dividend income from April 2026.

Those relying on property income will also see a two percentage point increase in tax rates, again from April 2027.

Will I be affected by Cash ISA cuts?

There is a potential sting in the tail for people under age 65 looking to shield higher amounts of cash in ISAs, potentially as part of a cash funnel strategy in the run up to retirement or to drip feed in some of their tax-free cash withdrawals. The annual subscription limit for a Cash ISA will be set at £12,000 for investors under the age of 65 from April 2027, but for those 65 and over, the annual limit for a Cash ISA will remain at £20,000.

Were there any changes to inheritance tax on pensions?

The draft legislation is due any day now, and it’s unlikely that we’ll see any major changes to the proposals to include unused pension funds in the value of someone’s estate for deaths after 6 April 2027. But the budget documents did confirm a small tweak to the administration process to ease some of the burden on the personal representative of the pension holder after death.

It’s been announced that they’ll also be able to ask the pension scheme to retain funds to meet the IHT bill in certain circumstances. Until now, the proposals only gave this power to beneficiaries themselves, potentially creating issues if money then had to be reclaimed by an estate.

The amount everyone can pass on before IHT applies, known as the nil rate band, will remain frozen at £325,000 until 2031.

Who will the ‘mansion tax’ affect?

An extra tax for properties valued over £2 million will be introduced from April 2028. This will start at £2,500 a year for properties in the £2-£2.5million band, stepping up to £7,500 for those worth over £5 million.

Although this won’t affect everyone, those who have lived in the same place for decades and seen house prices soar over that period might review their plans to stay put in retirement. It could even cause people to shift focus from options like equity release towards considering downsizing as an alternative.

Charlene Young: Senior Pensions and Savings Expert

Charlene Young is AJ Bell’s Senior Pensions and Savings Expert. She joined AJ Bell in 2014 from a wealth management firm where she worked with private clients and small businesses as a financial planner.

Charlene...