Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Related

news

Ask the experts. Russ Mould is on hand to answer your queries about the financial markets. If you'd like a question considered for a future edition, send it in now.

I notice Japanese stocks have been trading at record levels recently. What does the new prime minister Sanae Takaichi mean for the markets and will there be a repeat of Abenomics which I remember being talked about a lot a few years ago?

David

Russ Mould, AJ Bell Investment Director, says:

Japan’s Nikkei 225 stock index is indeed closing down on new all-time highs following the appointment of Sanae Takaichi as leader of the Liberal Democratic Party (LDP) and prime minister and her selection, in turn, of finance minister, Satsuki Katayama.

The top two posts in Japanese politics will be held by women for the first time, but investors seem even more interested in comparisons between Takaichi and Shinzō Abe, given the similarities in their policy proposals and political preferences. Abe’s reform programme, dubbed ‘Abenomics,’ is widely credited with dragging the Japanese economy out of a 20-year deflationary funk and boosting the Nikkei at the same time, so it is easy to understand why equity investors may be getting excited.

What did Abenomics involve?

Abe’s failed first stab as prime minister in 2006-07 quickly became a distant memory after he swept back into power in December 2012 and immediately announced his so-called ‘Three Arrows, programme, which targeted:

- Huge fiscal stimulus and infrastructure spending programmes

- Huge monetary stimulus, initiated with the relaunch of quantitative easing by the Bank of Japan five months later

- Structural reform across areas such as employment law, agriculture, tax, energy and foreign direct investment

The goal was to get Japan’s economy back on a consistent growth path, after the quarter-century of stagnation that followed the bursting of the 1980s’ debt-fuelled property and equity bubble, and drive inflation toward the Bank of Japan’s 2% target.

Abe largely succeeded, with the result that he became Japan’s longest-serving prime minister, as he added general election victories in 2014 and 2017 to that of 2012. The Nikkei also took flight as it surged from just under 10,000 when Abe took office to more than 22,000 by the time he stepped down owing to illness in summer 2020.

Will we see more of the same under the new PM?

Takaichi won control of the LDP and then the role of prime minister, following the resignation of her predecessor Shigeru Ishiba, by calling for more fiscal stimulus, loose monetary policy from the Bank of Japan and the wider restart of Japan’s fleet of nuclear power plants, where only a handful of 54 reactors are operating some 14 years after the accident at Fukushima.

In a further nod to Abe and his programme, the PM is focusing on energy security, as well as national security, since she also wishes to change to Article Nine of the (pacifist) Japanese constitution, whereby Japan can strengthen its military capability. Takaichi is already proposing an increase in defence spending to 2% of GDP.

However, there are some key differences between now and the situation that Abe inherited, even if the desired direction of travel is the same.

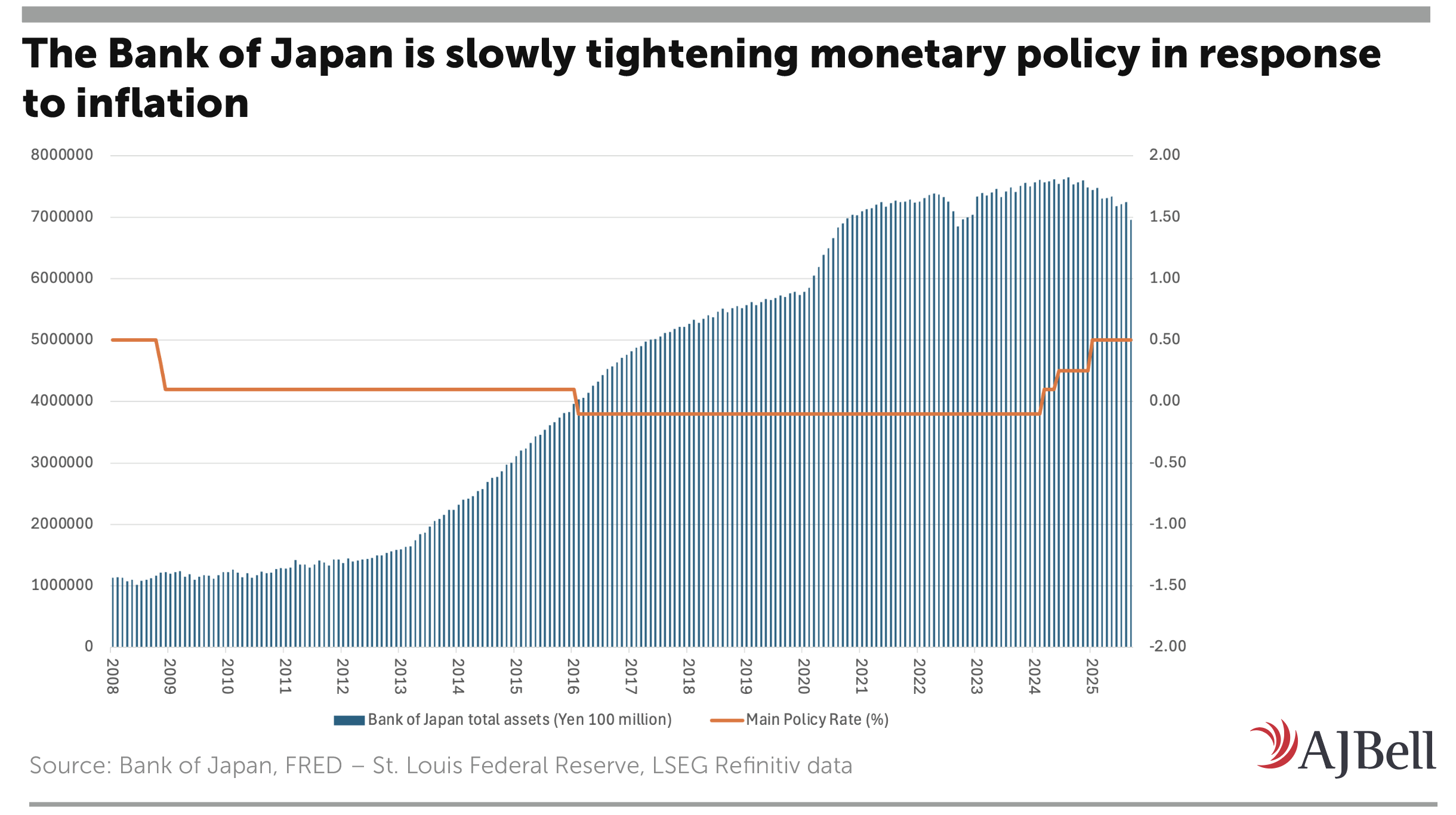

At 2.9% in September, inflation is running above target, not below it. The price of rice is a big cause of this, after a series of poor crops, but it is not the only one and the last print below the Bank of Japan’s 2% target dates back to March 2022.

As a result, the Bank of Japan is tightening monetary policy, rather than loosening it, as it did during Abenomics. Governor Kazuo Ueda has sanctioned three interest rate increases since May 2024, to take the Main Policy Rate to 0.5% from minus 0.1%. The Bank of Japan has also started to shrink its balance sheet by reducing its holdings of Japanese government bonds (JGBs), Japanese equity exchange-traded funds (ETFs) and Japanese real estate investment trusts (REITs). Ueda is proceeding slowly, and how successfully Takaichi can push back on even that remains to be seen.

This is particularly the case given the yen is weakening again, to possibly increase imported inflation, and 10- and 30-year JGB yields sit at multi-year, if not all-time, highs, as bond vigilantes stalk Japanese sovereign debt markets as actively they are now policing British, American and European ones.

Takaichi must contend with Donald Trump’s tariff policies, which now extend beyond China to include Japan. In theory, Tokyo and Washington have an accord here, with Japan promising to invest $550 billion in the US in return for a flat 15% levy, but the details still seem blurry at best.

Why there is a big difference now

There is one final key difference: the Nikkei is now nearly five times higher than when Abe returned to office nearly 13 years ago. Japanese equities are not as cheap as they were. However, the Nikkei still stands on 1.6 times book value, compared to the 2.4 times peak reached in the late 1980s and the early 2000s trough of just 0.8 times, so bulls of the market may argue there is still upside potential, especially given the improvements in Japanese corporate governance, shareholder relations and returns on equity seen over the past decade.

Russ Mould: Investment Director

Russ Mould is AJ Bell's Investment Director. He has a Master's degree in Modern History from the University of Oxford and more than 30 years' experience of the capital markets.

He started out at Scottish...