Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

There is a growing debate as to whether the traditional 60% shares and 40% bonds strategy is outdated. There is a suggestion that gold, property and private equity also deserve a place in an investors’ portfolio, to provide more balance.

A key reason why investment experts are reappraising portfolio construction is the failure for bonds to behave as they used to.

For years, many investors chose a combination of 60% equities and 40% bonds as an effective way to invest, often called the 60/40 portfolio. This method was widely adopted on the basis that equities often performed strongly and when they didn’t, bonds would step in and provide support.

While investors who plan to keep their investments in the market for a long time may be comfortable holding just equities, as they have more time to ride out market turbulence, those who were starting to derisk their holdings often favoured a 60/40 mix, which was meant to offer more stability.

In recent years, bonds have not provided the required cushion during equity market selloffs, leaving investors wondering why their portfolios were moving around more than expected.

Some industry experts suggest there needs to be a new balance that includes investments like alternatives, a term that encapsulates investments outside of stocks, bonds and cash. It can include physical assets like gold or property, or less common investment methods, like private markets.

Asset manager BlackRock found that between 2022 to 2024, 60/40 portfolios had a smaller average return and a larger amount of volatility than the decade before, which can explain the unease many investors are feeling.

While this is a relatively short amount of time to make a judgement, BlackRock claims that larger degrees of market and macroeconomic uncertainty mean it could be a new era for financial assets.

Why is 60/40 struggling?

The issues around the 60/40 method are mostly linked to interest rates and inflation.

Central banks typically increase interest rates when inflation shoots above their target. Currently, the UK has an interest rate of 4.25%, while inflation sits at 3.6%, which is far above the Bank of England's goal of 2%. In this case, both numbers are higher than what is ideal for investors and the central bank, creating a quandary.

The Bank of England would normally put up rates if inflation is high, yet it is expected to cut rates to help stimulate a stagnant economy.

This makes for a strange scenario for markets, and particularly long-term bonds, as yields are heavily impacted by these movements.

However, this isn’t to say that 60/40 portfolios won’t work again in the future. If there are changes in the macroeconomic environment, and specifically lower inflation rates, this balance of equities and bonds may start to suit investors again. But for the moment, there is a higher degree of correlation than some investors are comfortable with.

Thoughts from AJ Bell’s investment experts

The AJ Bell investments team runs a set of portfolios that balance holdings across many asset classes. They keep a close eye on where the markets are moving, and how different asset classes work together.

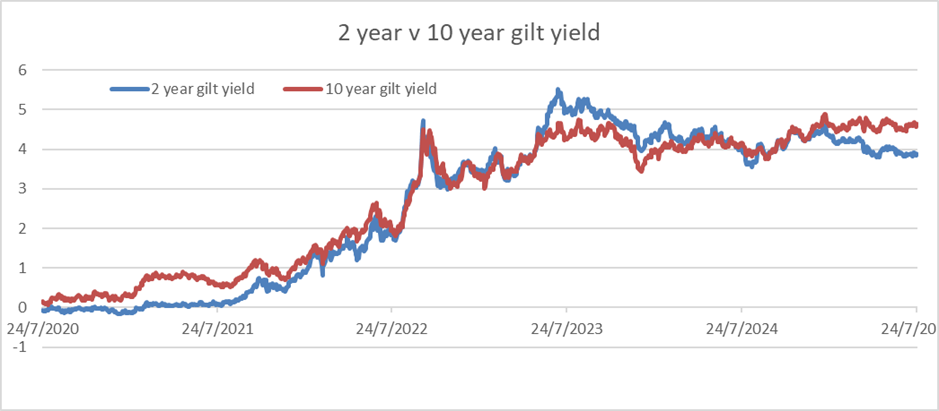

To head of investment solutions James Flintoft, the key has been what kind of bonds people are invested in. People often think of the bonds in a 60/40 holding being made up of long duration bonds. This means bonds that will be re-paid over a period that's usually 10 years or longer. But many bonds are repaid in a shorter time frame than that. And these shorter duration bonds might now offer a better balance with equity holdings.

“Traditionally, when people think about the relationship between equities and bonds, they are thinking of long duration, or at least mid-duration bonds. I think that’s where there are questions over whether equities and bonds can still balance each other out, and whether we’ve now gone into a different regime where that relationship doesn’t exist,” Flintoft says.

“Historically, there have been times where bond prices go up and down at the same time as equities, particularly in the 70s. The key is considering what part of the bond market we are thinking about.”

Short-term bonds react differently to inflation and interest rate changes, because they will often reach maturity before any long-term expectations for the interest rate or inflation environment would come to fruition. However, they may be more influenced by any short-term changes that the market does not see as part of a bigger pattern. This means that they can perform differently to longer-dated bonds.

“We’re trying to use short duration bonds to make sure that the bond part of our portfolio does what it’s meant to when we need it. Basically, it protects us in the bad times,” Flintoft said.

“That doesn’t mean that longer-dated bonds will always do badly. If you look at (the market tumble in) April, they did their job. So, maybe that’s a useful marker for some people, but we’re much more concerned about the inflation piece, and changing that correlation for the future.”

Often, having less sensitivity has meant that short-term bonds have a much lower yield. But by the end of 2024, the difference between the yield on short-term bonds and long-term bonds was very small, making short-term bonds more appealing.

Source: Refinitiv

How else can you diversify a portfolio?

There are many ways to be diversified, and what suits you is largely dependent on the amount of risk you are comfortable taking.

Risk-averse investors may choose to diversify with cash. Now, cash interest rates can be above 4.5%, which is a relatively attractive yield, especially among low-risk holdings. Those that want to keep their assets in the same portfolio may choose to invest through money market funds, so they do not need to open a separate cash savings account and can usually get slightly higher returns.

BlackRock’s CEO, Larry Fink, has previously suggested the 60/40 portfolio structure could be replaced in the modern world by one that contains 50% equities, 30% bonds and 20% private markets.

There are numerous investment trusts on the UK stock market that invest in private assets such as companies or infrastructure projects. Most of these trusts trade at a discount to their value of their assets because the market is concerned about liquidity – namely their ability to sell assets quickly. They are also marked down because there is often limited information on private assets compared to publicly listed companies.

Can gold help?

For those keen to think further outside the box, areas like gold have been popular investors this year, with the metal hitting record price highs. But over the years, it has proved to be a volatile asset class.

In addition, UK investors need to bear in mind that gold is often denominated in US dollars, versus sterling. As the US dollar has been weakening against the sterling, that means any assets that UK investors hold in the dollar will show weaker returns than they would in the local currency.

Flintoft points out that in the case of gold, it can also be hard to determine what is driving the price. For example, this year saw a large uptick after investors felt the US had become a riskier place to invest. They demanded a higher return for owning US government bonds, which saw prices fall and yields rise. That wobble in the bond drove certain investors to look at gold to diversify their assets as it has historically done well in times of uncertainty.

“Gold is a volatile asset class, and it is difficult to know how it’s going to perform,” Flintoft says.

If you don’t feel comfortable structuring your portfolio by yourself, another option is to invest through a multi asset fund, where investment professionals structure a portfolio with a variety of asset classes. These funds are available from many different providers, including AJ Bell.

Hannah Williford: Investment Writer

Hannah joined AJ Bell in 2025 as an investment writer. She was previously a journalist at Portfolio Adviser Magazine, reporting on multi-asset, fixed income and equity funds, as well as macroeconomic impacts and regulatory changes...