How I invest: The personal finance geek chasing a comfortable early retirement

Related

news

Shares Magazine

The phrase ‘it’s a marathon not a sprint’ was put to the test at this year’s London Marathon when two runners smashed the sub-two-hour barrier, with Kenya’s Sabastian Sawe taking home the ultimate prize. The 1:59:30 finishing time has changed expectations around the world of running forever and while his 4.33 per mile pace might challenge this slow and steady truism, the feat was achieved over years of dedicated focus, objectivity and hours of work.

This same long-term mindset is often applied to investing and just like taking on the immense task of taking part in a marathon, having a goal in mind when you start is key and planning for the long-term is crucial.

For Rayhan, his investment goals are simple: He wants to become ‘work optional’ before the state retirement age at which point he wants to be mortgage free and be able to use the 4% drawdown rule to affordably cover his family’s living expenses and enjoy at least a couple of UK holidays a year.

In monetary terms, this looks like around £1 million invested in his Stocks and shares ISA which “isn’t mega lavish, but it’s not a beans on toast lifestyle of scrapping by,” Rayhan says.

With roughly £128,000 in his ‘core’ Stocks and shares ISA today he has some way to go but, he also has a clear vision on how he’ll achieve his goal.

From premium bonds to investing in tech stocks

Growing up with three older siblings in Edinburgh, carving out any space for himself was appealing and Rayhan “definitely too young to be working” began to build up his financial independence at an early age working a paper round and cash-in-hand pot wash jobs as a young teen.

“I’ve always been attracted to having my own money and being independent,” he says. “I’ve also always been a bit of a personal finance geek.”

This hard-working mindset was inherited from his parents who moved over to the UK from Pakistan before he and his brothers were born. “I saw the work ethic of my parents, and I found it really important to be able to have a bit of money in my own back pocket,” he says.

His first foray out of just holding cash savings came in 2012 while he was studying at Edinburgh University and was introduced to premium bonds by one of his older brothers and a close friend, the latter he stills “geeks out” with about investing today.

The £25-£150 prizes he was ‘winning’ led Rayhan down a different monetary path to the one his dad had taken, largely investing in property and being “a big saver”, and he became immersed in the personal finance world and in particular, the FIRE movement.

An acronym for ‘Financial Independence, Retire Early’, FIRE is a financial movement defined by frugality, extreme savings, and investments. The idea gained traction among retail investors in the US from Vicki Robin and Joe Dominguez’s 1992 book Your Money or Your Life and took off more internationally after 2010 when Jacob Lund Fisker’s Early Retirement Extreme came out.

The central idea is determining when you want to stop working and doing the sums on what you realistically need to save to achieve one of three ‘ideal’ lifestyles

Rayhan sits somewhere between wanting more than the bare bones just paying the bills level but isn’t seeking to have “an absolutely luxurious life”.

The influences

Having made this first step into investing, Rayhan’s interest grew and he began to absorb more and more investment content through podcasts and books including Mad Fientist, BiggerPockets, The Simple Path to Wealth and Robert T Kiyosaki’s Rich Dad, Poor Dad was especially impactful on him. But while he understood the concepts, the practical steps of actually getting into the market felt elusive to him.

“I probably spent a bit too long learning about index funds...there was a confidence issue on pulling the trigger,” he says.

That gap was filled after graduation when a financial adviser came to his parent’s house to have a free 30-minute session with him, during which he was given the ‘how to’ knowledge and was told who the major platforms were and what products were most appropriate for him.

But even then it took another couple of years and it wasn’t until 2018 when he was 26 that he opened a Stocks and shares ISA and purchased his first global tracker fund – the Legal & General International Index trust and e-learning firm Learning Technologies Group based on the idea that it was “a hot and a booming sector”.

The stock pick made a £1,500 return in one year, up 42%, “not a huge amount of money but it was a four-figure amount, and I remember thinking ‘woah ok this is good, this is making me more money than the premium bonds I had been in’”.

Getting over that initial hurdle was a big mental win, and once he’d pushed open that door, Rayhan was prepared to fully commit.

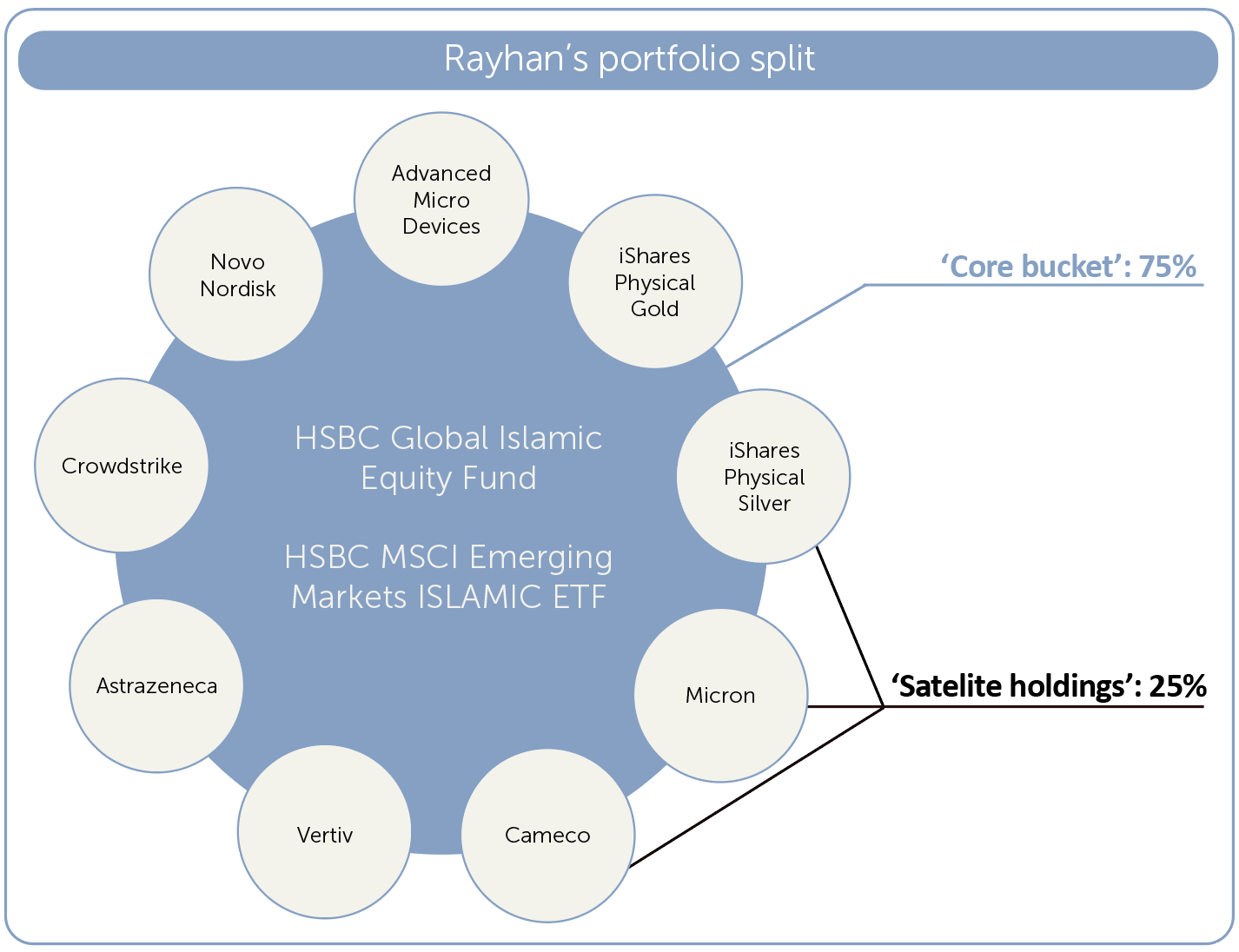

Taking the advice that his young age meant he could tolerate a more “aggressive” portfolio with a large allocation to stocks as he had time to “ride out the waves” Rayhan split his portfolio into 75% ‘core’ and 25% diversifying ‘satellite’ holdings.

The latter is made up of induvial stocks and precious metals like gold and silver through iShares trackers alongside some crypto “for a bit of excitement”.

Of the individual stock names, he currently owns: Advanced Micro Devices, Micron, Cameco, Vertiv, AstraZeneca and CrowdStrike are all up between 11% and 77% since he started holding them, while Novo Nordisk is down 70%.

His ‘core’ bucket is two global ETF trackers and arguably reveals one of the more integral parts of Rayhan’s investment philosophy. His faith.

Rayhan invests in Sharia-compliant assets, holding the HSBC Islamic Global Equity Index fund and HSBC MSCI Emerging Markets Islamic Screened Capped ETF, up 43% and 20% respectively.

The idea of choosing investments based on ethics and not just their potential for a financial return was formalised into the ‘environmental, social, and governance’ (ESG) investing during the pandemic, but many concepts within it already had decades of case study, including Sharia investing.

Pioneered back in the 1960s and 70s when the first modern Islamic bank was founded - the Mit-Ghamr Islamic Saving Associations (MGISA) – offering depositors a share of its profits instead of interest, otherwise known as riba and strictly prohibited in Islam.

While still regarded as a relatively niche sector, Islamic finance assets were estimated at $4.5 trillion in 2022, according to research by HSBC while the London Stock Exchange estimates that the global Islamic finance industry will reach $6.7 trillion in assets by 2027, citing strong demand from Muslim and non-Muslim investors.

When he made his pioneer investments Rayhan “didn’t know it was an option” to invest that way but since learning has made it a hard and fast investment rule.

When the time comes to put the theory into action

While his confidence has grown Rayhan has had to learn some market truisms the hard way, in particular, don’t try and time the market.

“You tell yourself you’ll be levelheaded, but when you’ve made your first four figure profit you start thinking you’re Warren Buffett, that you’re the next guy.”

When the Covid sell-off happened, Rayhan was two years into his ‘proper’ investment journey and in the throes of his first bout of market volatility.

“I’m proud to say I didn’t panic sell when things first plummeted; I stayed invested. But I was hearing so much noise that everyone was predicting this W shaped double bounce so when it went back up after March, I cashed out, at a profit, but with the intention of buying back in when the second dip came.” In the end that didn’t happen, and equity markets rocketed to new record highs.

“It just kept going up and eventually I just accepted that I had missed out on some gains and jumped back in six months later in 2021,” Rayhan recalls.

“It was a lesson I had to go through that you just have to keep in it,” which he did during his second big market test after the announcement of Donald Trump’s Liberation Day tariffs in April 2025.

Paying it forward

While still a way off his financial goals, Rayhan is enjoying the process of building a financial future for his wife and kids in a way that hadn’t felt accessible to his parents.

“My dad is proud of me, he doesn’t really care for the details so much but he’s happy I’m in a good position with my money,” he says.

Now aged 33 working in tech sales, Rayhan has become a bit of a financial guru within his extended family, with his siblings and nieces and nephews often coming to him with questions about how to be more financially educated and literate “and I love it”.

Not so far from the investment influencers he still follows, Rayhan has himself dabbled with the idea of creating investment content, especially around Sharia compliant content.

“I love talking about it and learning about it... I think that’s definitely a niche that can be further educated,” he says.

Eve Maddock-Jones: Funds and Investment Trust Writer

Eve joined AJ Bell in 2026 as a funds and investment trust writer. She was previously editor at Investment Week, reporting on all major retail investor news, covering funds and investment trusts, ETFs and regulation...