Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Related

news

Shares Magazine

Ask the experts. Russ Mould is on hand to answer your queries about the financial markets. If you'd like a question considered for a future edition, send it in now.

Amid all the talk about Trump it feels like emerging markets are being ignored, what is their outlook like in the current market environment?

Michael

Russ Mould, AJ Bell Investment Director, says:

This column cannot pretend it knows what America’s President, Donald J. Trump, is going to say, or do, next, or what the full implications of his policies on issues such as Greenland, interest rates and the US Federal Reserve and tariffs and trade could be. But it does know that US equities are trading in the top 10% of valuation ranges on any metric you care to mention, relative to their history.

As such, US stock markets are not priced for any sustained bout of turbulence, be it geopolitical, economic or financial. It would be logical to expect any investors who are of a nervous disposition, and fear further policy, and financial market, volatility to consider doing one of two things:

Apply a higher equity risk premium and demand a higher return from equities relative to the risk-free rate, for which the local 10-year government bond yield is a good proxy. In plain English, this means paying a lower valuation for assets, as this increases the potential for positive returns.

Diversify, and look for markets whose valuations are more attractive than the multiples currently afforded to American stocks, in absolute terms, and also relative to both their own history and the US.

Intriguingly, US assets have gently underperformed since December 2024, when the S&P 500’s market capitalisation peaked at 64.3% of that of the FTSE All-World index. That weighting now stands at 61.5%, so perhaps markets are already subtly sending the message that the era of US exceptionalism is fully priced in, and there may be better value to be had elsewhere, especially as the S&P 500 topped out at 59.2% of the All-World benchmark in early 2002, by which time the technology, media and telecoms (TMT) bubble had already started to burst.

Emerging option

One area which may be worthy of further research, at least for risk-tolerant contrarians, is emerging markets. This column is not a specialist in the field of technical research, and the taking of signals from price charts, but two things jump out from the next one to even the most casual observer.

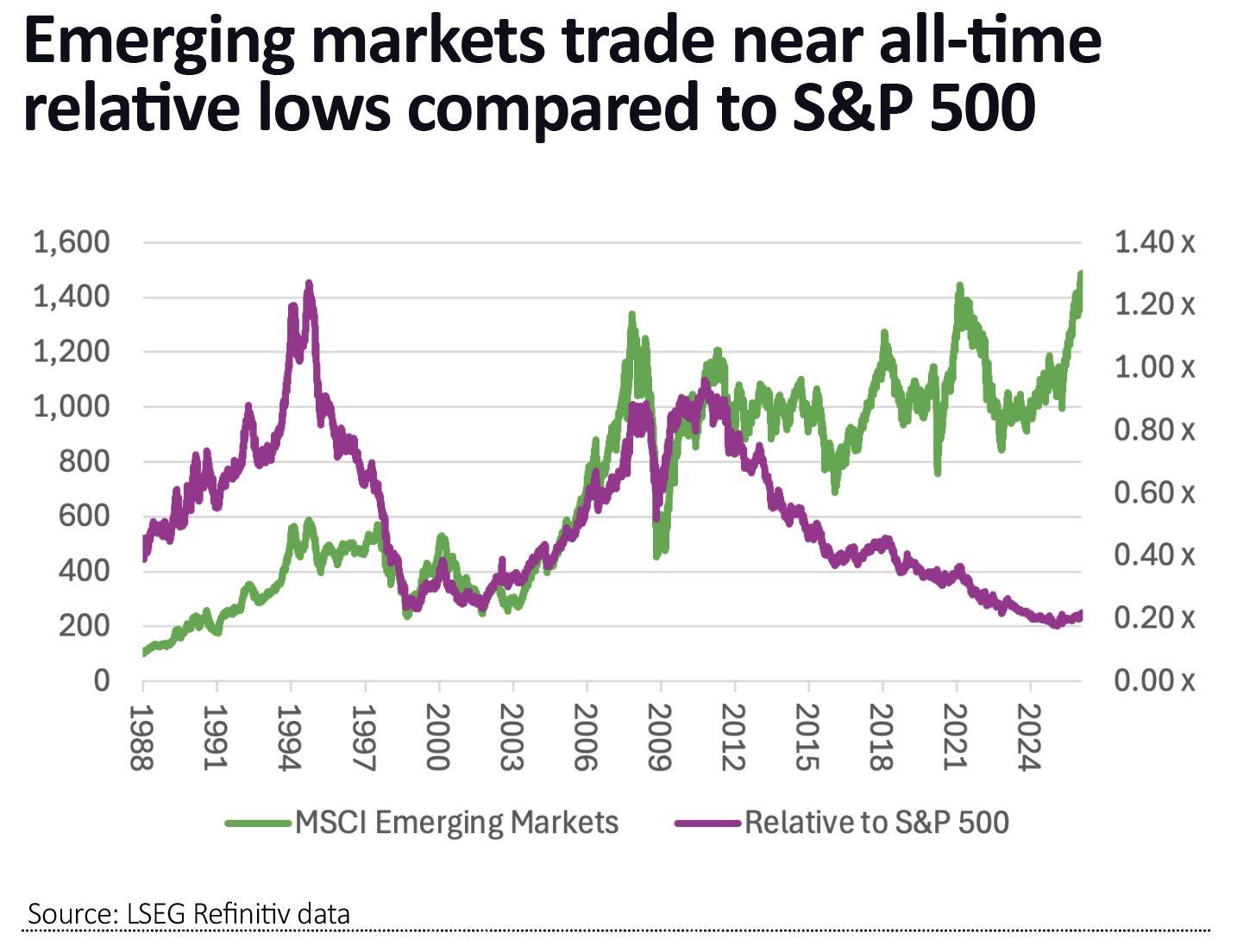

First, the MSCI Emerging Markets (EM) index looks to be breaking out above its former all-time high. Chartists often say that this can signal further strong momentum to come, if the move away from prior peaks proves decisive.

Second, the emerging markets benchmark trades near all-time relative lows compared to the S&P 500.

None of this guarantees further upside in the MSCI EM benchmark. But a weaker dollar is traditionally seen as a boost for emerging markets, as it makes it easier for those nations who borrow in dollars to service their debts, and rising commodity prices can be a tailwind for them, too, as many developing nations are major producers of precious and industrial metals, as well as oil and gas and agricultural crops. And, right now, the dollar is weakening, and many commodities are surging to all-time, or at least multi-year highs, most notably gold, silver, copper and platinum.

Range of options

Careful research is still required, as emerging markets are not homogenous by any means, and they come with a range of risks, including politics, currency movements, corporate governance and how easy it is (or otherwise) to buy and sell on local exchanges. Investors could be forgiven for seeking broad-brush exposure via actively or passively managed funds, which will provide access to a basket of countries and industry sectors in either equities or bonds, or both, rather than tackling the nitty-gritty of individual stock selection.

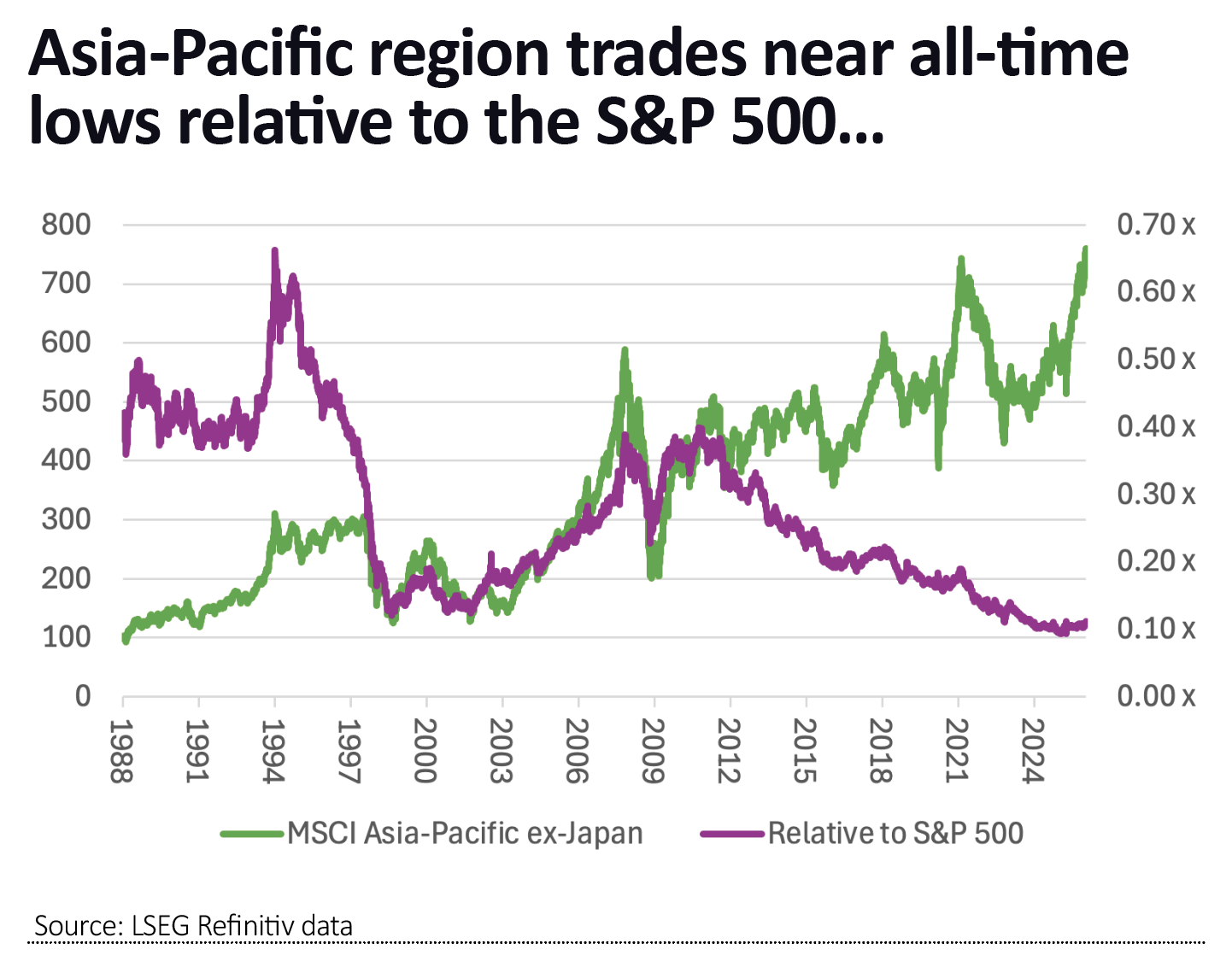

But it is possible that at least some of those not-so-hidden dangers are already factored into EM valuations. The MSCI Asia-Pacific ex-Japan index is currently benefiting from the technology exposure provided by Taiwan’s TSMC, Korea’s Samsung Electronics and SK Hynix and the AI magic dust associated with Chinese internet giants Alibaba and Tencent. The index is hitting new all-time highs, but the index’s relative rating compared to the S&P 500 is near historic lows.

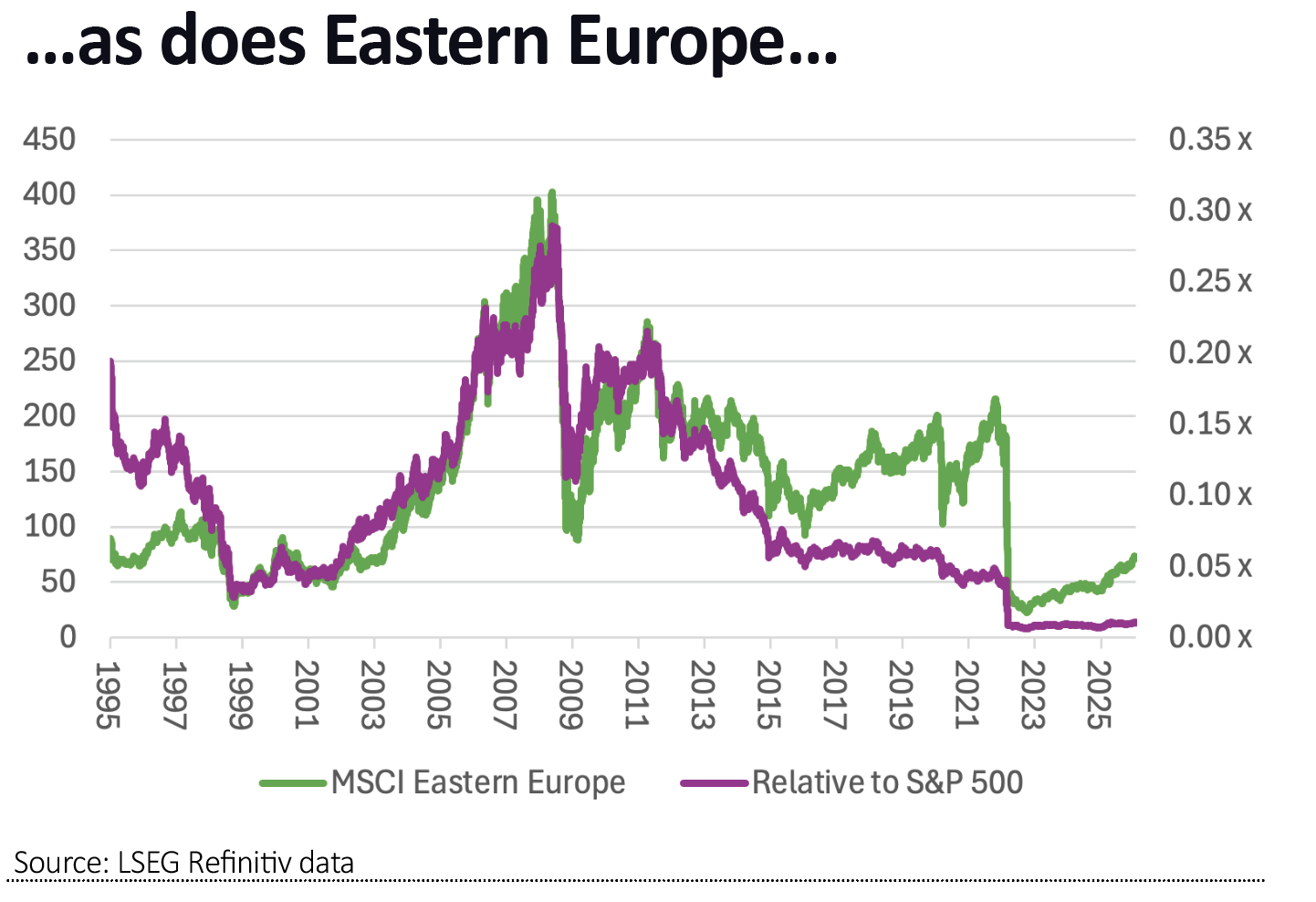

Eastern Europe may just be too tricky for some, given the proximity of the war in Ukraine and Russia’s fall from grace in 2022 when it sanctioned the invasion of its neighbour.

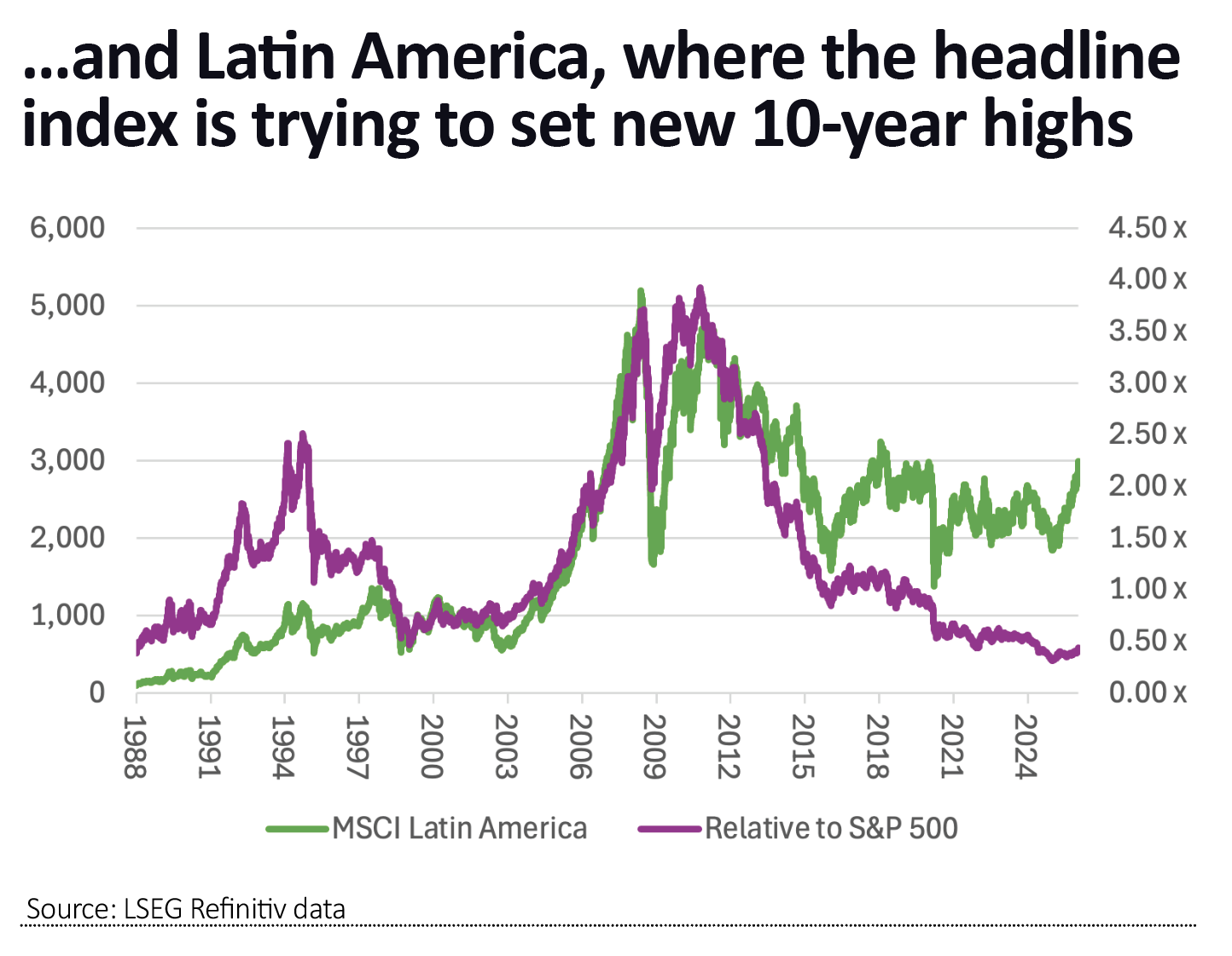

Latin America has a tiny weighting in the All-World indices, with Brazil, Chile, Colombia and Mexico chipping in barely 1% of the benchmark’s capitalisation. But the MSCI index is rallying, helped by a rightward shift in politics in Argentina, Peru and Bolivia, scope or interest cuts as reforms put a lid on inflation and strong industrial and precious metal prices.

Russ Mould: Investment Director

Russ Mould is AJ Bell's Investment Director. He has a Master's degree in Modern History from the University of Oxford and more than 30 years' experience of the capital markets.

He started out at Scottish...