Want to improve your investing skills? Don’t make these three common mistakes

Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Getting ahead with investing isn’t simply down to picking the best stocks, funds or bonds. It’s also about not falling into various traps that catch out individuals time and time again.

Here are three mistakes that all kinds of investors make. If you’re aware of them, and understand why they should be avoided, it can help to keep you on the right path.

1. Putting all your eggs in one basket

One of investors’ biggest mistakes is to be too reliant on one or two stocks in their portfolio. They allocate the bulk of their funds to these names and often get caught out because they lack diversification. You'll feel the pain in your portfolio if these names experience share price decline.

If you invested £1,000 into semiconductor group Nvidia five years ago, your investment would now be worth £14,100 before fees. It’s a mouth-watering statistic to most investors. And for many, it makes a convincing argument to put your money into a company that you believe is about to take off.

The problem? It’s impossible to know what stock is going to have those kinds of returns. And even with a stock-picking strategy, there’s a lot of luck that comes into play.

For example, what if in 2020, you had chosen an investment in Zoom instead, which led the way for keeping people in touch during the pandemic? At first, you would have wallowed in gains, as the stock’s share price leapt 117% in just over three months. But five years on, the share price has fallen over 72%.

Out of the current S&P 500, 325 companies would have given you a worse return than simply investing that money in a fund tracking the S&P 500 index over the past five years. Further, putting money into near 100 of those companies would have resulted in a loss.

It’s not just a struggle that DIY investors face: even professional investors have a difficult time picking stocks correctly.

The good news is investors who spread out their returns among many different stocks have also been able to make attractive gains in the past few years. In sterling, the S&P 500 has gained 92.5% in the past five years. That means £1,000 invested in the index would have turned into £1,925 before fees.

This is not as exciting as the return from Nvidia, but it’s important to consider what you’re planning to use this investment for. If you are aiming to buy a home, is the risk of having your money in just a handful of stocks one you’re willing to take?

Some investors decide that they still would like to invest in a few single stocks but put the bulk of their investments in a fund, which holds a more diverse group of companies. This allows them to have a lower risk level for most of their savings but still pick a few favourite companies to see how the investments play out.

2. Timing the market

When the price of a market drops, it’s natural to want to stop your own wealth declining. This leads many to pull their investments out of the market.

But markets are not linear. They can turn up or down within a day, and if you take your money out of the market when prices are dropping, and then wait to put your money back into the market when prices start to rise, it means you might miss out on some of those gains in the turnaround.

For example, if you invested £1,000 in a fund tracking the FTSE 100 at the start of 2025, you would have made a total return (including dividends) of 6.75% by 1 April. But the announcement of tariff policies from the US made markets take a turn for the worse. By 4 April, the market had slumped and lost all its gains year-to-date. At this point, you decided to cash out. Nervous about another potential fall, you kept your money out of the market for a little bit longer.

By 15 April, you decided you were ready to dive back into the market. You took your £1,000 and put it back in the FTSE 100 tracker fund. By 14 July, you would have enjoyed a 9.4% return including dividend, turning your £1,000 into £1,094.

But what if, instead, you rode out the drop in the market? You would have had to weather the worst day of the FTSE 100 so far this year, but then you would have enjoyed the market climbing back up. Your investment would have returned 11.8%, turning your £1,000 into £1,118. All the calculations in these examples exclude charges.

Investing requires patience and history suggests that markets eventually recover from a selloff. Some recoveries happen quickly; others take longer. None are guaranteed to happen, yet pulling money out at the first sign of a market wobble may not necessarily be the best thing to do.

3. Forgetting fees

Past performance is the first thing most investors check when choosing a fund.

How a fund has performed previously does not necessarily have any bearing on how it will perform in the future. But it can be a helpful indication of what to expect.

For example, if you are investing in an emerging markets fund, you may see that some years have a lot of growth, and in other years, the market falls. This can prepare you for what your journey may be like as an investor.

But what can also have a significant impact on your return is the fees of a fund. And unlike returns, those often come at a set rate.

Generally, passive funds (which track an index) have smaller fees than active funds (where stocks are chosen by an investment professional). For passive funds, these fees can often be under 0.5% and closer to 0.1%. However, an active fund may charge somewhere closer to the 0.5% to 1% range. You can check these fees by looking at the AJ Bell fund screener. When choosing a fund, this ongoing charge fee will be factored into the fund’s performance.

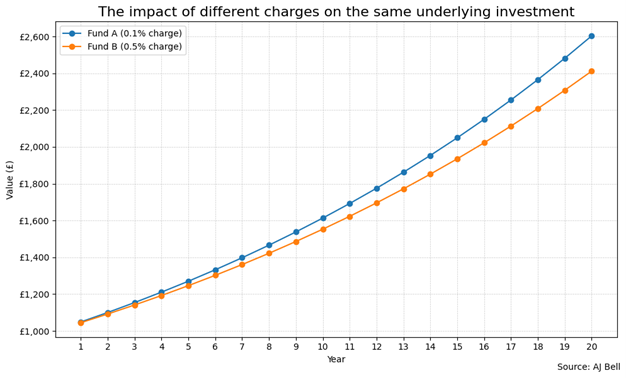

How much does this really affect your investment? Let’s say you invest £1,000 in two funds. Fund A, with a charge of 0.1% and Fund B with a charge of 0.5% that track the same index, so will have a similar level of return. Without factoring in fees, let’s assume that they both return an average 5% annually. How would that difference in fees affect the growth of your money over time?

Initially, not by much. In five years, Fund A would be worth a total of £1,270, while the investment in Fund B would have grown to £1,246. But further down the line, the difference becomes more significant. After 20 years, the investment in Fund A would be worth £2,603 while Fund B would stand at £2,411. That near-£200 difference is equivalent to a fifth of the money you started with. And for larger sums of money, the differences become even more obvious.

While it may seem counterintuitive, a higher fee doesn’t mean a better fund performance. And while you can’t know how a fund will perform, you can know how high fees will eat into those returns.

Hannah Williford: Investment Writer

Hannah joined AJ Bell in 2025 as an investment writer. She was previously a journalist at Portfolio Adviser Magazine, reporting on multi-asset, fixed income and equity funds, as well as macroeconomic impacts and regulatory changes...