Archived article: Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

The government has launched a new review of the state pension age, which may mean that it rises to the age of 68 sooner than planned.

Currently both men and women can claim the state pension from the age of 66, but this is already planned to rise to 67 and to 68 for future pensioners. However, the government has launched the third review of the state pension age to consider whether the rules around pensionable age are still appropriate based on the latest life expectancy data and other evidence.

As a result of this review, the government may be told to accelerate plans to raise the state pension age to 68, although it isn’t forced to accept recommendations. An increase to state pension age from 66 to 67 is already slated to happen between 2026 and 2028. But it’s less clear what will happen after that. There is also an increase to age 68 pencilled in for 2046, but a faster increase is definitely on the cards.

The first two reviews of the state pension age advocated for bringing this forward, but successive governments have treated the issue like a hot potato. This latest state pension age review, however, may eventually force the government’s hand.

Read more about the state pension.

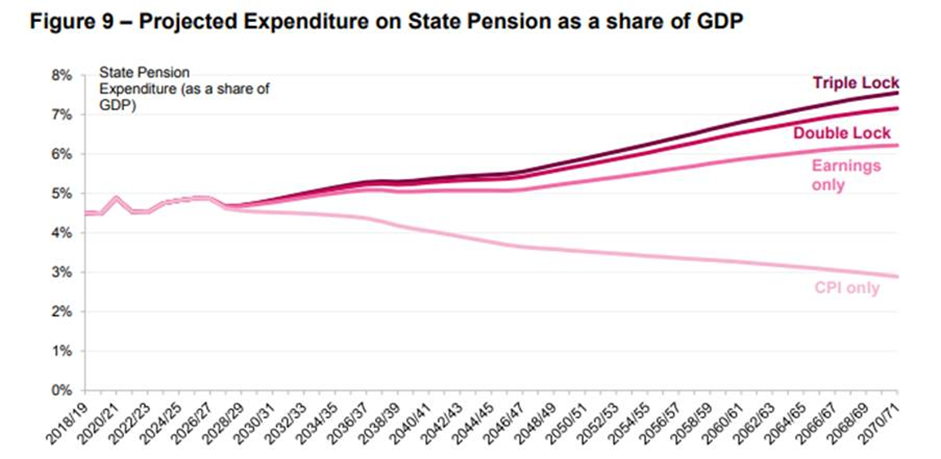

State pension benefits are one of the single biggest expenses for the Treasury and account for more than 80% of the £175 billion pensioner welfare bill. Without policy intervention, state pension costs are set to spiral to nearly 8% of GDP over the next 50 years based on the current trajectory, up from 5.2% today, according to government figures.

The second state pension age review in 2023 recommended that the increase to 68 should be introduced between 2041 and 2043 to help reduce costs, although the government under Rishi Sunak opted not to commit to that timetable. However, the new Labour government may feel it needs to consider the rise to age 68 more closely, particularly if it wants to demonstrate steps toward long-term fiscal prudence.

What will the third state pension age review look at?

The new state pension age review will look at key factors such as linking state pension age to life expectancy, fairness between generations, and its role in ensuring the state pension’s long-term sustainability.

An ageing population places an increasing burden on taxpayers, with state pension costs rising and fewer working age taxpayers to cover the cost. Future governments will hope that an improved economy and growing tax receipts will help alleviate some of the pressure. But that can’t be guaranteed, and there needs to be a credible plan for maintaining affordability.

One option is to raise the state pension age higher and faster than currently planned. Although the elephant in the room is that state pension age is just one lever government has to help manage the cost of the state pension – the other is reforming the triple lock.

Could the triple lock be under threat?

For over a decade, debate about the state pension has centred on maintaining the triple lock guarantee. Making changes to state pensions is a notoriously fraught endeavour, and Labour has already committed to keeping the triple lock during this parliament.

However, if the state pension age review calls for the state pension age timetable to be accelerated, that could provide some cover for future governments to look at reforming the triple lock in order to avert ever more dramatic rises in state pension age.

Figures included in the last state pension age review illustrate how alternatives for increasing the state pension could help manage costs.

Source: Second State Pension Age Review Independent Report team modelling. Includes basic state pension, new state pension, over 80 pension and additional state pension. Additional state pension is uprated by CPI only and unchanged between each scenario.

What to do if your state pension age changes

If the review recommends bringing forward an increase to age 68 to the mid-2030s, the government will need to step carefully. Bad memories of accelerating the increase from age 65 to age 66 linger in the UK psyche. The government will need to give Brits enough advance warning to make plans for their retirement. Bringing forward the increase to the mid-2030s will mean those born in the early 1970s will have to find from their private savings the equivalent to an additional year of state pension if they want to retire at the same time on the same income.

Past experience shows it will be essential for the government to sing – loudly and clearly – from the rooftops about any rises in state pension age. Everyone should know their state pension age, or we risk people not adequately planning for their retirement.

For those planning ahead, it is important not to panic. Any changes to state pension age will be phased in over time so this won’t change your plans if you’re retiring in the near future.

However, it does illustrate that relying on the state pension alone for your retirement income is risky. The state pension, now worth close to £12,000 a year, is extremely valuable. If you’re forced to wait a year or two to claim it, you’ll either need to work longer or find tens of thousands of pounds extra from your pension and private savings to plug the gap.

Many people will feel they don’t want to work until their late 60s, and many will feel it’s physically impossible for them to do so, especially those with labour-intensive jobs. While some people will be able to manage by leaning on other savings, downsizing their home to free up cash, or moving into another job, possibly part-time, as retirement approaches, the best way to give yourself freedom to retire on your own terms is to build up your private pension pot.

So-called ‘normal minimum pension age’ determines when you can access your private pension pot. While that will rise to 57 in the next few years, and may rise again to keep it within 10 years of state pension age, it is the best way to give yourself the financial means to retire early before your state pension kicks in.

The best way to boost your pension is to increase contributions, taking maximum advantage of any employer matching and tax relief on offer. Consolidating your private pension pots together will also help you get control of your money, potentially reduce fees to boost returns, and allow you to plan ahead.

Rachel Vahey: Head of Public Policy

Rachel is AJ Bell's Head of Public Policy. She helps financial advisers and planners understand the changing pensions and savings environment, as well as how new legislation and regulation affects them and their clients.

Rachel...